👻औसत छात्र 👻

1.7K posts

#SME #CosmicCRF #Cosmic #Amzen

Cosmic CRF H2 & FY26 Concall Highlights

👉 FY27 & Future Outlook

▫️Emphasis on volume-led growth expected in FY27 with existing operations targeting 1.22–1.30 lakh MT production (vs ~1.06 lakh MT achieved in FY26)

💠Implying ~30%+ topline growth even without Amzen contribution; no exact number given to avoid “unnecessary guidance”.

💠Supported by higher realisations and improved utilisation (targeting 90%+ across facilities

💠Prices of raw materials and finished goods expected to rise further in H2 FY27 (7–10%+ uplift anticipated)

▫️Amzen Legal victory:

💠Supreme Court set aside NCLAT order; company declared eligible and remains sole H1 bidder.

💠In words of Management: “God-given” transformative asset with modern German/American machinery.

💠Subsidiary integration progressing smoothly; plan to consolidate remaining 26% in NS Engineering via SEBI route.

💠Mainboard transition eligibility achieved (30 June 2026); filing expected first week of July.

▫️Amzen integration to be a game-changer:

💠LOI expected shortly (possibly June), factory ramp-up in 9–12 months (commercial production targeted March–May 2027)

💠Initial focus on repairs/maintenance + wagon manufacturing (scaling from 3,600 to 7,200 wagons p.a.).

▫️Long-term vision (by FY29):

💠~3.5 lakh MT total capacity and potential ~₹3,500 Cr revenue at ~₹1 lakh/MT average realisation.

💠Amzen alone expected to be equivalent to the entire current group (CRF + NS + Springs/Forging) at full utilisation — the single biggest growth driver over next 3–5 years.

💠Springs business margins to expand sharply post-RDSO approval (target PAT 10–18%)

💠Forging unit commercial production in next 9 months with high-value, high-margin railway components (₹1.4–1.5 lakh/MT ASP).

💠Container manufacturing (sea freight 20/40 ft) planned via Amzen — initial mathematical target 7,500–10,000 units.

👉 Current Order Book / Projects and Future Pipeline

▫️Order book of ₹760 Cr (split between railway and infrastructure items) providing excellent visibility.

💠~75% of coach/wagon body deliverables manufactured in-house across 4 units

💠Full backward integration (CRF sections, DM/non-DM items, fabrication, springs, forging, galvanizing) reduces dependency on vendors.

▫️Pipeline highlights:

💠Government’s plan to procure ~1 lakh wagons (~₹40,000 Cr opportunity) + Rail Plan 2031–33 requiring ~4 lakh additional wagons over 5–7 years (~40,000–45,000 wagons p.a. feasible industry-wide).

💠West Bengal government change expected to drive massive infra push— management already engaging with officials.

💠Amzen strengths: all types of wagons (open top, covered, etc.), bridge girders (20,000 MT capacity), wagon repairs (big addressable market from ageing fleet), DFCC/internal siding advantages.

💠Additional diversification into sea freight containers and defence/export wagons.

👉 Other Notable Points

▫️Operational scale-up:

💠Total installed capacity 1,33,600 MT (CRF standalone 55k + NS 65k + CSEL 13.6k)

💠FY26 production ~1,06,370 MT (~90% YoY volume growth)

💠NS ramped 12.5k → 65k MT; overall capacity grew ~94% YoY. Utilisation ~80% (engineering plants typically max out at 85–87%; targeting 90%+ next year).

💠Cash flow from operations turned positive (₹3.5 Cr vs negative ₹90 Cr last year) despite aggressive capex.

💠Debt remains light (term loan only ~₹36 Cr; total debt ~6–15% of assets/topline).

▫️Margin & balance sheet:

💠Some FY26 PAT dilution due to springs ramp (only ₹1.5 Cr profit on ₹67 Cr revenue pre-RDSO), Amzen-related carrying costs, and legal expenses.

💠Margins expected to improve meaningfully with scale, backward integration, and higher-value products.

💠Promoter-led execution + team efforts repeatedly highlighted; multiple capacity additions (new sheds, galvanizing bath expansion, R&D) funded largely through accruals + preferential warrants.

👉Questions & Answers:

💠 Amzen timeline & contribution: 9–12 months to commercial production; FY27 impact minimal; major ramp from FY28 onwards

💠Debt & funding: Peak term debt post-Amzen ~₹200–300 Cr range; well within manageable levels given asset size and cash position; no immediate dilution expected.

💠 Springs/Forging: Current low margins due to pending RDSO; improvement expected post-approval. Forging to add high-margin railway safety components.

💠Margins & RM volatility: Hedging + long-term contracts + PVC clauses + future liquid metal initiative planned for larger scale.

STR@sachprat07

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform. 👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional. ——— 👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform : 💠 OBSC Perfection 💠 Aimtron Electronics 💠 Yash Highvoltage 💠 CFF Fluid Control 💠 DSM Fresh Foods 💠 L.T. Elevator 💠 Monolithisch India 💠 GSM Foils 👉Across Different Sectors. One common place. 🔗 smeresearch.github.io/SMEGems 👉Stay tuned for more insights ——— ⚠️ For educational purposes only. Not investment advice. Please DYODD. #SMEGems #SMEPlatform #HiddenChampions #SME

English

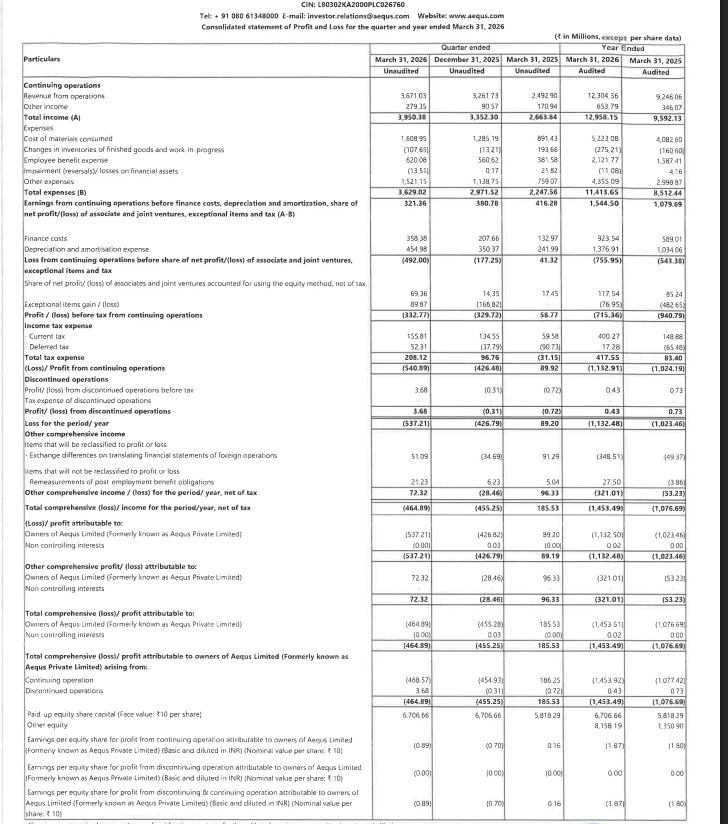

Aequs Ltd Q4FY26 Results:-

#Q4Results #Q4FY26 #Stockmarket #Nifty #Aequs

Revenue 367.10 Cr vs 249.29 Cr

(+47.26% YoY┃+12.55% QoQ)

EBITDA 4.20 Cr vs 24.53 Cr

(-82.88% YoY ┃-85.52% QoQ)

EBITDA Margin 1.14% vs 9.84% YoY & 8.90% QoQ

PBT Ex-Exceptional Items

-42.26 Cr vs +5.88 Cr YoY & -16.29 Cr QoQ

PAT -53.72 Cr vs +8.92 Cr YoY & -42.68 Cr QoQ

Other Income 27.94 Cr vs 17.09 Cr YoY & 9.06 Cr QoQ

Last Q3 Exceptional loss of 16.68 Cr

This Q4 Exceptional Gain of 8.98 Cr

English

@Atulsingh_asan Offline store mein toh mujhe iska koi product hi nahi dikhta UP mein

Indonesia

7 Good Defence stocks to track🔥

Solar Industries

Data Pattern

Astra Microwave

Unimech

Azad

Aequs

Axiscades

Which one is your favourite❓

TheAlpha10X@TheAlpha10X

Very Positive news for Private Defence Sector stocks 🟢🔥 ✅Bookmark it Solar Industries Data Pattern Astra Microwave Idea Forge MTAR Nibe Paras Defence Zen Tech Unimech Cyient DLM DCX Systems Azad Aequs Structurally very positive for Indian private defence players. It reinforces a multi-year trend: more outsourcing, indigenisation, ammo/missile/drone/private manufacturing push Which of the above stocks do you like the most❓ Follow @TheAlpha10X for more such interesting stock ideas RETWEET & SHARE if useful For Early Entry & Exit, check the Comment Section 👇👇👇👇👇

English

Attended Bihar AI Summit 2026.

Good initiative by Bihar Govt but speakers of events may be upgraded.

Inviting Miss Universe Bihar is in such event is meaningless 😁

English

Tell me one Defence stock you are holding silently thinking it can become a serious wealth creator in the next 3 to 4 years.

English

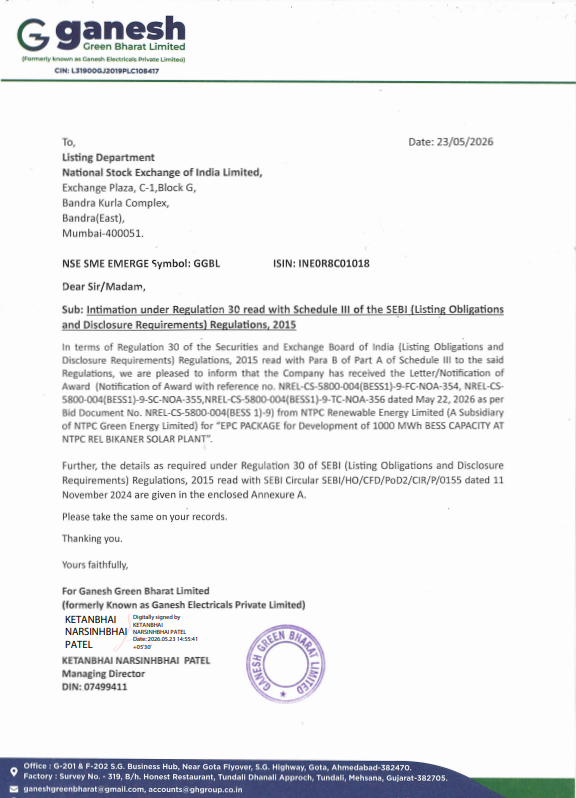

Ganesh Green Bharat has received the Letter of Award(LOA) from NTPC Renewable Energy for EPC PACKAGE for Development of 1000 MWh BESS CAPACITY AT NTPC REL BIKANER SOLAR PLANT.

Total order book for ongoing projects has increased from Rs. 700 Cr0, as intimated on 22nd May 2026, to Rs. 2210 Cr.

#ggbl

English

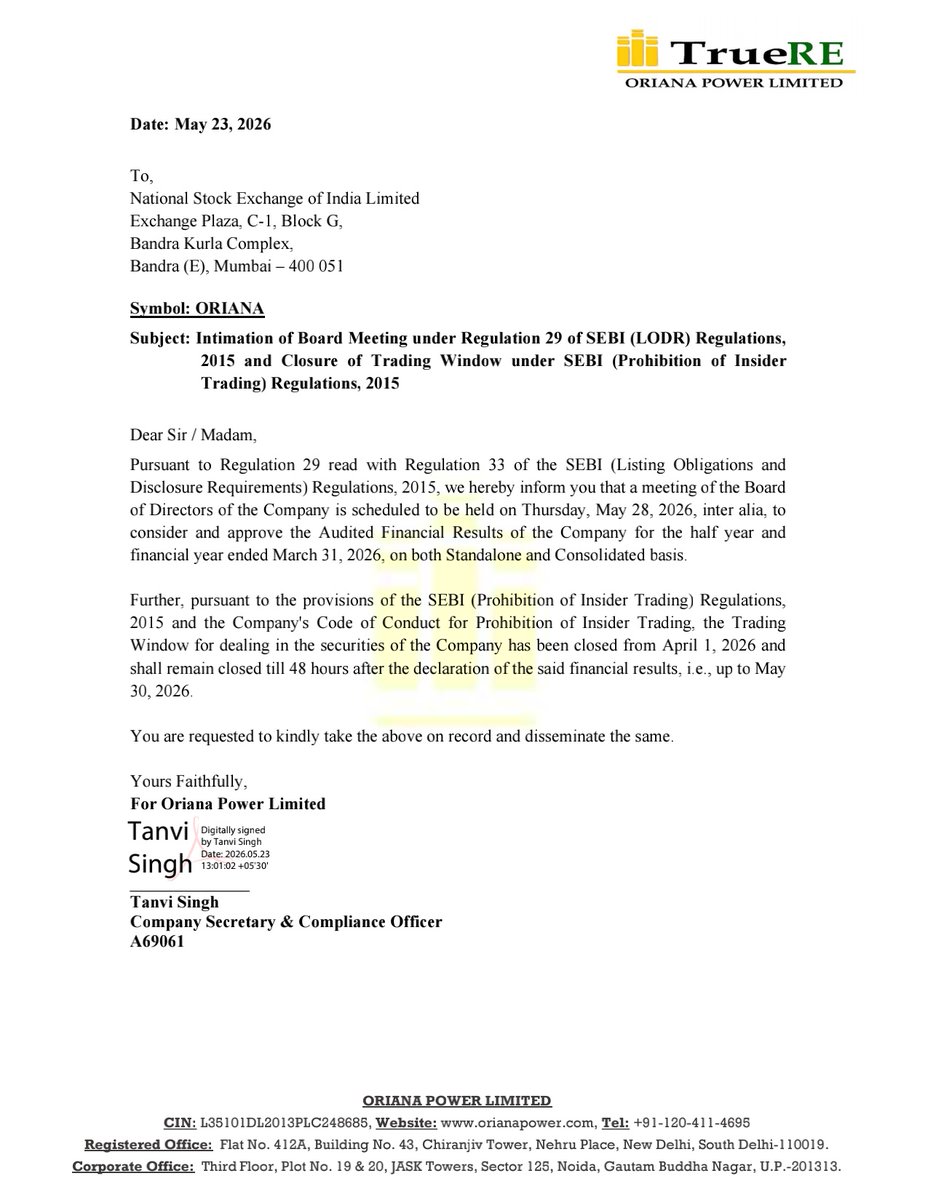

📌 Oriana Power Limited informed the exchange that a meeting of the Board of Directors of the Company is scheduled to be held on Thursday, May 28, 2026, (1) to consider and approve the Audited Financial Results of the Company for the half year and financial year ended March 31, 2026, on both Standalone and Consolidated basis. #SME #ORIANA 📅📊

English

Most people know TruAlt Bioenergy as India’s largest ethanol producer. More recently, people started tracking the company because of its Sustainable Aviation Fuel (SAF) ambitions after signing a technology licensing agreement with Honeywell UOP.

But I think the most interesting business inside TruAlt today is neither ethanol nor SAF.

It is CBG.

And the timing here is becoming extremely interesting.

India is aggressively expanding PNG infrastructure, CGD networks, and CBG blending initiatives. The direction is very clear. India wants a larger share of its energy ecosystem to come from domestically produced gas alternatives over the next decade.

The problem is that supply is nowhere close to demand.

India’s SATAT programme envisioned thousands of CBG plants, but actual operational capacity today remains a fraction of what was originally planned. That creates a massive supply gap just as the ecosystem is getting built out.

This is where TruAlt quietly enters the picture.

Through its subsidiary, Leafiniti Bioenergy, the company has already been operating a 10 TPD CBG plant. And the numbers are surprisingly strong.

FY26 revenue from this single plant was nearly ₹42 crore with EBITDA margins exceeding 50%.

That detail matters a lot because while TruAlt’s core ethanol business is currently facing underutilisation and margin pressure, this relatively small CBG operation is already demonstrating significantly superior economics.

And now they are scaling aggressively.

• JV with Sumitomo Corporation

→ 4 CBG plants

→ 20 TPD each

→ 80 TPD planned capacity across Karnataka & Maharashtra

• JV with GAIL

→ 49% stake in Leafiniti

→ 72 TPD additional planned capacity

But the more important detail here is that GAIL could potentially offtake the entire production.

That changes the nature of the business completely.

Once India’s largest gas infrastructure player becomes your potential buyer, the business starts moving away from cyclical commodity-style economics toward something far more stable with better demand visibility and stronger revenue predictability.

And then there is the SAF optionality sitting quietly in the background.

TruAlt already has the Honeywell UOP Ethanol-to-Jet technology agreement and plans to develop 80,000 TPA SAF capacity in Andhra Pradesh.

Which means the company’s underutilised ethanol capacity today could potentially become SAF feedstock tomorrow.

Same ecosystem.

Same feedstock chain.

Potentially far better economics.

This is why I think the market may eventually start viewing TruAlt very differently.

What people currently see:

“An ethanol company facing margin pressure.”

What it could gradually become:

• A high-margin CBG platform

• A SAF player linked to aviation decarbonisation

• A stable ethanol blending business

• A carbon-credit-generating bioenergy ecosystem

Interesting times ahead for TruAlt Bioenergy.

This is not investment advice. :)

English

India’s healthcare opportunity is massive 📈

Top listed hospital chains in India 👇

✅ Apollo Hospitals Enterprise

74 hospitals | 10,400+ beds

✅ Manipal Hospitals

49 hospitals | 12,600+ beds

✅ Fortis Healthcare

36 hospitals | 6,000+ beds

✅ Narayana Health

21 hospitals | 5,859+ beds

✅ Max Healthcare Institute

20 hospitals | 5,200+ beds

India still needs ~2.4 million more hospital beds to meet global standards.

Rising insurance penetration + ageing population + lifestyle diseases + medical tourism = Huge long-term opportunity for hospital sector.

Healthcare may become one of India’s biggest structural growth stories over next decade.

#Hospitals #India #HealthCare

English

If you have to select 4 stocks to invest till 2030

Which 4 Stocks Will You Select?

English

@vandit_jain1994 Sir आप भी टेलीग्राम ग्रुप चलाते हो देख कर सेबी वाले लेंस लेकर खोज रहे हैं😆🤣

हिन्दी

You would find many people boasting about Trident Techlabs when it was doing well.

However, most never accepted their mistakes, never posted whether they exited or are still holding and have just vanished.

I accepted my mistake, shared about my exit publicly.

Making a mistake is not wrong, when people publicly boast about their great calls..they should also accept their wrong calls.

𝗩𝗲𝗿𝘀𝗮𝘁𝗶𝗹𝗲 𝗦𝘁𝗼𝗰𝗸 𝗜𝗻𝘃𝗲𝘀𝘁𝗶𝗻𝗴@vandit_jain1994

Once a fraud always a fraud.. Management guided 250 cr sales and 40 cr PAT in FY25 and failed to deliver even close to it even on FY26. Trident Techlabs Limited Blunder Results H2FY26 vs H2FY25 (YoY) 👉🏼 Revenue: ₹33.74 Cr | ▼ 39.2% YoY (vs ₹55.50 Cr) 👉🏼 OPM: -9.3% vs 23.4% in H2FY25 👉🏼 Net Profit: ₹ -5.31 Cr | vs ₹8.04 Cr in H2FY25 - turned negative FY26 vs FY25 (YoY) 👉🏼 Revenue: ₹97.24 Cr | ▲ 27.0% YoY (vs ₹76.57 Cr) 👉🏼 OPM: 14.3% vs 21.8% in FY25 👉🏼 Net Profit: ₹6.07 Cr | ▼ 47.3% YoY (vs ₹11.50 Cr) I was invested in it when plans were good, trusting the management. Realised that I betted on a wrong management and exited when FY25 results were distster. Learned many important lessons. Check all comments.

English

@BasantBaheti3 यहां तो x पर हर एक स्टॉक का नाम लिखता है और लास्ट में DYDD लिख देता है😂

हिन्दी

मेरा तो हर दूसरा ट्वीट निवेशकों को इन फ़र्ज़ियों से बचाने का ही होता है , पिछले पाँच साल से ट्विटर पर यही कर रहा हूँ , सोशल मीडिया पर जो भी विशेषज्ञ शेयर का नाम लेकर सलाह दे , उसे तुरंत ब्लॉक करें , ये बात मैं कई बार लिख चुका हूँ !

केवल उन्हीं विशेषज्ञों को सुनकर अपना ज्ञान बढ़ाएँ जो शेयर का नाम लेकर टिप नहीं देते क्यूँकि शेयर का नाम बताने वालों में 95% चिपकाने वाले विशेषज्ञ ही होते है इसीलिए 95% ट्रेडर लूजर रहते है

Vikas Khemani@vikaskhemani

Don’t know much about this case. But a wake up call and suggestion to fellow investors not to fall in trap of tips and people who recommend stocks and create FOMO. Social media has made it easy. Either build your knowledge or invest through professionals. No other way! Pl respect and treat your hard earned money with utmost care and love, not to be squandered like this. @carnelian_asset @NDTVProfitIndia @CNBCTV18Live @ETNOWlive @ETNowSwadesh @CNBC_Awaaz

हिन्दी

Sterlite tech received order of 10,000 cr rupees, bookmark it.

This order either will be canceled or will remain unexucted in future !!

English

Which one of these 3 has the potential to become a 10x in the next 3 years? 🤔

1. ABS Marine (PE-9)

2. Desco Infratech (PE-11)

3. Jay Bee Laminations (PE-12)

English

👻औसत छात्र 👻 retweetledi

#WATCH | Nibe Group says - Nibe Group has successfully completed the no-cost, no-commitment demonstration of its loitering munition named Vayu Astra with 100 KM Range at Pokhran on 18-19 April 2026 & Joshimath (Malari), Uttarakhand on 26-27 April 2026.

Nibe Limited’s Vayu Astra-1 Loitering Munition Anti-Personal carried out first NCNC demo successfully at Pokhran Range, Rajasthan, with 10 kg warhead in single attempt, successfully hitting the target at 100 km with CEP less than 1 m with abort attack and reattack capability of the LM. The LM is based on an Israeli loitering munition.

The team carried out Anti Armour (Anti-Tank) night strike using- IR camera and LM successfully hit the target within the 2 m CEP in a single attempt with capability of handing over the control from GCS to Forward Control Segment 70 km away was successfully demonstrated.

At Joshimath (Malari) Uttarakhand Vayu Astra-1 LM had been successfully demonstrated endurance flying more than 90 minutes high altitude loitering and endurance completed at more than 14000 Ft height and LM is recovery for next flight after completion of mission.

(Videos: Nibe Group)

English

👻औसत छात्र 👻 retweetledi