dre1012

3.6K posts

People who call SpaceX overvalued on current multiples are looking at today’s $16B revenue… so let me ask, what’s the TAM of the Milky Way galaxy?

English

$LMN.V @ 12x

Revenues on track. Margins to be optimized.

$CSU style reporting with a complete disregard to short-term focused shareholders

Other companies would definitely present you all the adjusted figures wrapped in a bow, but not this one.

Just wait for the numbers in the coming quarters.

English

dre1012 retweetledi

Lumine Group Q1’26 deep dive 👇

$LMN $LMN.V

1) Growth: headline organic looked weak, but the core recurring line was fine.

Revenue grew +17% YoY to $208.3m. Headline organic was 0% (or -2% FX-adjusted), but that gets distorted by the noisier buckets (licenses/hardware).

Cleaner read: maintenance & other recurring (highest-quality bucket) posted +6% organic (~+3% FX-adjusted) and was +27% reported on acquisition contribution. Recurring base is still growing; weakness was more in the lumpy lines/timing.

Of the +$29.6m YoY revenue uplift in Q1, ~$22m came from Synchronoss post-close. The remaining ~$7–8m uplift is mostly carryover from FY25 acquisitions (Vidispine + Datafusion) rather than true organic — my estimate is ~$8–9m combined.

2) M&A:

Synchronoss closed Feb 13, 2026.

Cash consideration paid: $309.3m

Cash acquired: $34.3m → net cash paid ≈ $275m

Synchronoss contributed $22.0m of revenue in Q1 and would have contributed ~$20m more if owned from Jan 1.

Implied pro-forma Q1 revenue ≈ $42.4m, annualized ~$170m (lines up with Synchronoss’ last run-rate/guidance range $169–$172m).

So the cash multiple ≈ 1.62× sales. Versus Lumine trading around ~5× P/S, you’re seeing the platform buy at ~1.6× and trade at ~5× — that “arb gap” is the point.

Synchronoss was funded via cash on hand + a $160m draw on the Lumine Facility; bank debt rose to ~$372m while cash fell to ~$248m, putting LMN at ~$124m net debt (ex leases) vs ~$140m net cash at Q4’25. Even post-deal, that’s still low net leverage (~0.5× net debt / EBITDA), leaving meaningful balance sheet capacity for further acquisitions.

3) Operating income = EBITA; margin compressed

Lumine’s “Operating income” is effectively EBITA (net income before tax, amort, bargain items, and finance/other).

EBITA was $57.9m vs $59.5m (-3%), but costs rose faster than sales: expenses +26% vs revenue +17% → expense ratio 67% → 72%.

Staff was the big line: staff +37% YoY. They disclosed $2.755m of Synchronoss transaction costs in staff/pro fees — but even adding that back, staff growth still looks too fast, suggesting other integration/roll-in costs not separately itemized (or a true step-up in the cost base).

4) Cash optics: CFO / FCFA2S collapsed (mostly WC + taxes)

CFO: $19.8m vs $40.1m

FCFA2S: $15.3m vs $35.0m

CFO drop was mainly to (i) worse working capital (~$14.5m) and (ii) higher cash taxes paid (~$4.4m).

Working capital drag was largely payables + receivables timing. A reasonable explanation (not explicitly stated) is post-acquisition cleanup — settling vendor/professional fee accruals and other payables around Synchronoss, plus normal billing/collection timing — which would show up as payables down / receivables up and hit CFO in Q1. Q2 will be the check on whether this mean-reverts.

English

dre1012 retweetledi

What does the post-acquisition journey at Lumine actually look like?

To answer that, we're starting a new series, ‘After Acquisition,’ tracing a company’s experience at 1, 5, and 10 years. First up: a look at Incognito Software Systems, acquired over a decade ago.

In this video, Lumine Group Founder & CEO David Nyland and key figures from Incognito's journey reflect on the acquisition and what a decade of growth has looked like in practice.

Watch the first in our ‘After Acquisition’ series: luminegroup.com/grow/incognito…

English

dre1012 retweetledi

Warren Buffett on Tim Cook, after the Apple CEO announced his upcoming retirement: “What he has done with Apple could not be done by anybody I’ve known.”

English

dre1012 retweetledi

The US is doing poorly, but Canada is in another league

The Food Professor@FoodProfessor

This one graph explains why more than 2 million Canadians rely on food banks every month: no wealth, no food. Simple as that.

English

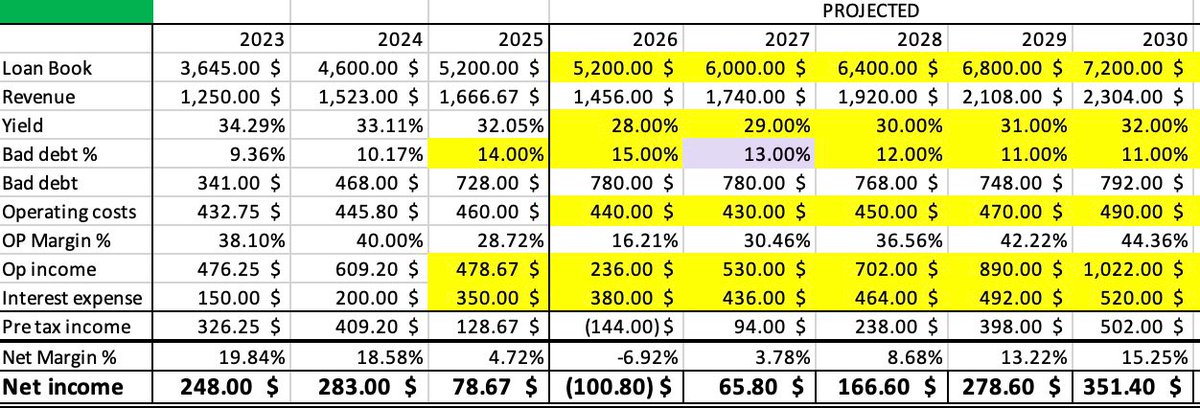

$GSY $GSY.TO ugly results but largely expected

The one big positive here supporting the turnaround thesis:

Net charge offs

Q1 guidance: 17.5% to 18.5%

Expected to decrease from 23.8% in the fourth quarter of 2025 to the mid-teens for full year 2026; improvement is expected as the year progresses.

..this means NCO’s are projected to end 2026 on a sub-14% run rate

= profits in 2027

English

@TraderNorway Only the 1B$ in debt is in negotiation (credit facility).

The 3.7B$ in bonds is in compliance.

English

Ask yourself why a creditor would put them in a recievership when they would get peanuts back for their $4B debt when goeasy can continue meeting their obligations and customer portifolio are booming. Meaning yields for creditors are good.

J

English

Is there another example where CSU steps in to restructure the debt part as a minority shareholder ?

I agree with your analysis btw, also for adj ebitda.

I was thinking csu can pay down that debt and refinance from the mother company at low rates, and then assess the value csu would pay for the whole biz.

English

@WSB_redditor @andrew1corpora1 @JustinvestToday Either you use EV, and net operating income, or market cap and net income.

Considering debt is pretty much permanent and used to generate revenues, I prefer to use net figures.

English

$LMN.V is alive

GIF

Investor Lens@InvestorLensCA

$LMN.V — Lumine Group Inc. | FY & Q4 2025 Results 📡 Constellation Software's comms & media spinoff posts a breakout year — net income flips from -$258.9M loss to +$118.8M profit 📊 FY 2025 Highlights: • Revenue: $765.7M (+15% YoY) • Net Income: $118.8M ($0.46/sh) — vs. $(258.9M) loss in 2024 • OCF: $236.5M (+106% YoY) — record • FCFA2S: $217.0M (+153% YoY) — record • IFRS Operating Income: $167.3M • Cash: $352.4M (up from $211.0M — strongest liquidity ever) 📦 Q4 2025: • Revenue: $216.3M (+16% YoY) • Net Income: $49.6M ($0.19/sh, +69% YoY) • OCF: $71.4M (+34% YoY) • FCFA2S: $67.1M (+48% YoY) 🏗️ Capital Allocation: • Acquisitions: $20.5M deployed in 2025 (vs. $145M in 2024 — selective year) • Bank debt reduced: $125.7M repaid, net debt position = net cash • 1% organic growth (FX-adjusted) — recurring revenue base = 70%+ of total 💡 The thesis: this is a Constellation Software clone in comms & media software. Near-$1B revenue, triple-digit OCF growth, and a balance sheet ready to acquire. Full analysis: investorlens.io/stocks/LMN.V #TSXV #LMN #CanadianStocks #VMS #SoftwareStocks #SmallCap #Acquisitions #InvestorLens

English

dre1012 retweetledi

$LMN.V — Lumine Group Inc. | FY & Q4 2025 Results

📡 Constellation Software's comms & media spinoff posts a breakout year — net income flips from -$258.9M loss to +$118.8M profit

📊 FY 2025 Highlights:

• Revenue: $765.7M (+15% YoY)

• Net Income: $118.8M ($0.46/sh) — vs. $(258.9M) loss in 2024

• OCF: $236.5M (+106% YoY) — record

• FCFA2S: $217.0M (+153% YoY) — record

• IFRS Operating Income: $167.3M

• Cash: $352.4M (up from $211.0M — strongest liquidity ever)

📦 Q4 2025:

• Revenue: $216.3M (+16% YoY)

• Net Income: $49.6M ($0.19/sh, +69% YoY)

• OCF: $71.4M (+34% YoY)

• FCFA2S: $67.1M (+48% YoY)

🏗️ Capital Allocation:

• Acquisitions: $20.5M deployed in 2025 (vs. $145M in 2024 — selective year)

• Bank debt reduced: $125.7M repaid, net debt position = net cash

• 1% organic growth (FX-adjusted) — recurring revenue base = 70%+ of total

💡 The thesis: this is a Constellation Software clone in comms & media software.

Near-$1B revenue, triple-digit OCF growth, and a balance sheet ready to acquire.

Full analysis:

investorlens.io/stocks/LMN.V

#TSXV #LMN #CanadianStocks #VMS #SoftwareStocks #SmallCap #Acquisitions #InvestorLens

English

@WideMoatCzar @goeasyltd It’s almost impossible that it stays within the range. Stock is pricing in some challenges. If not this goes +100%.

English

@dre1012 @goeasyltd As long as net charge-offs remain within their target range (8–10%) and management can successfully prove that it is legitimate (no accounting delayed losses) then this dip is a gift.

English

$GSY.to @AndreyOmelchak states that the GoEasy management has made a number of mistakes :

1. The Diversification “Mistake” (Auto Lending): Andrey contends that GoEasy overextended into the automotive loan market, a sector where they lacked deep historical expertise. He suggests the "mistake" was chasing growth for growth's sake when their core unsecured lending market was already large enough.

2. The collection failures: He said, “Maybe Collection wasn’t great, it was difficult to collect the cars for non paying and the technical matters around it” His argument is that GoEasy struggled to physically collect or repossess vehicles from non-paying borrowers.

inthemoneypod@inthemoneypod

Propel is plunging 10% after profit and sales missed expectations Small cap investor Andrey Omelchak would buy the dip, but is staying clear of Goeasy $PRL.to $GSY "We just discussed Propel...and the management team is A+. As it relates to Goeasy, management has made mistakes." WATCH THE FULL EPISODE NOW: youtu.be/vXnu04GqR5w?si…

English

@WideMoatCzar @goeasyltd I’d add to that by saying GSY is just starting its auto business, and they will grow it a lot over the next few years… So what matters more is how that future loan book does, which they now have much more experience in.

English

For the first argument, @goeasyltd management is shifting from unsecured to secured lending via physical assets. I think secured loans now make up around 42% of the total loan book, which in the long term lowers the company’s overall risk profile.

For the second argument, that is where short seller @JehoshaphatRsch alleged that GoEasy’s auto loan book was hiding serious delinquencies, which $GSY.TO management has denied. If GoEasy can prove through the first half of 2026 that its 180-day charge-off policy is legitimate and recovery values on cars are holding up, then it is not a mistake in my opinion.

English

English

@WideMoatCzar @inthemoneypod Having a short report written on you is now a mistake on management it seems. Idk either

English

Propel is plunging 10% after profit and sales missed expectations

Small cap investor Andrey Omelchak would buy the dip, but is staying clear of Goeasy $PRL.to $GSY

"We just discussed Propel...and the management team is A+. As it relates to Goeasy, management has made mistakes."

WATCH THE FULL EPISODE NOW: youtu.be/vXnu04GqR5w?si…

YouTube

English

@WSB_redditor As long as the ROE is anywhere in the positive, this is a buy

English