Dylan

1.7K posts

Dylan

@dylan_teeter

Value-oriented investor with a very long term perspective $IREN

Katılım Haziran 2015

1.1K Takip Edilen870 Takipçiler

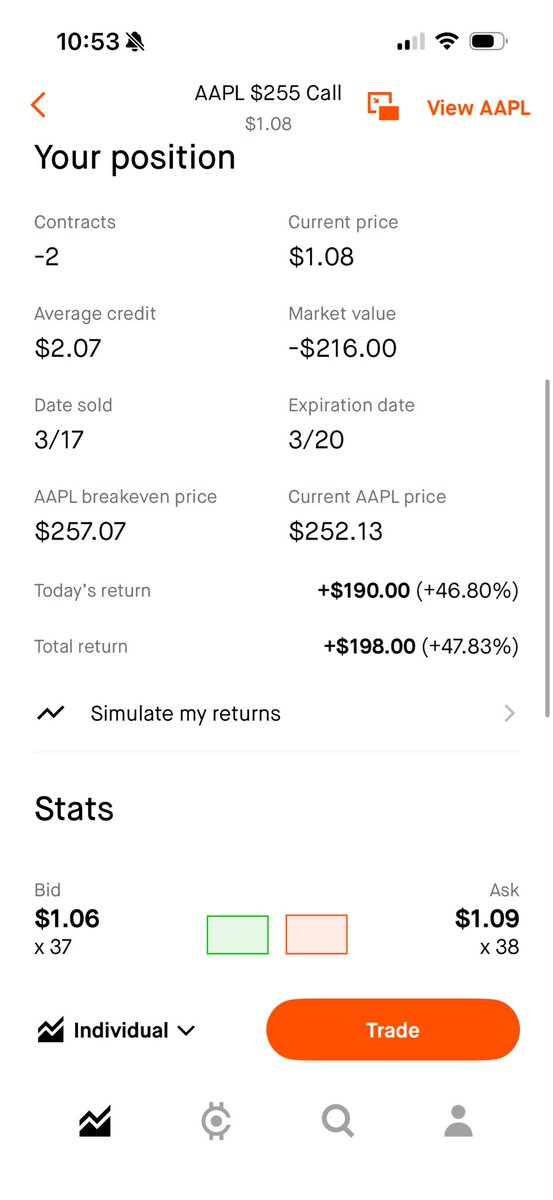

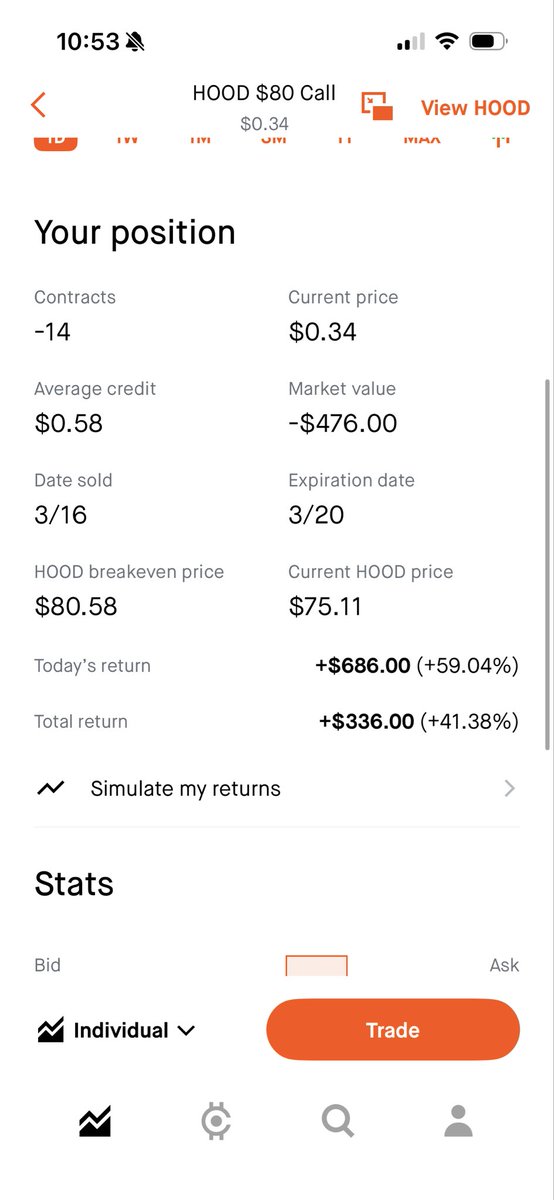

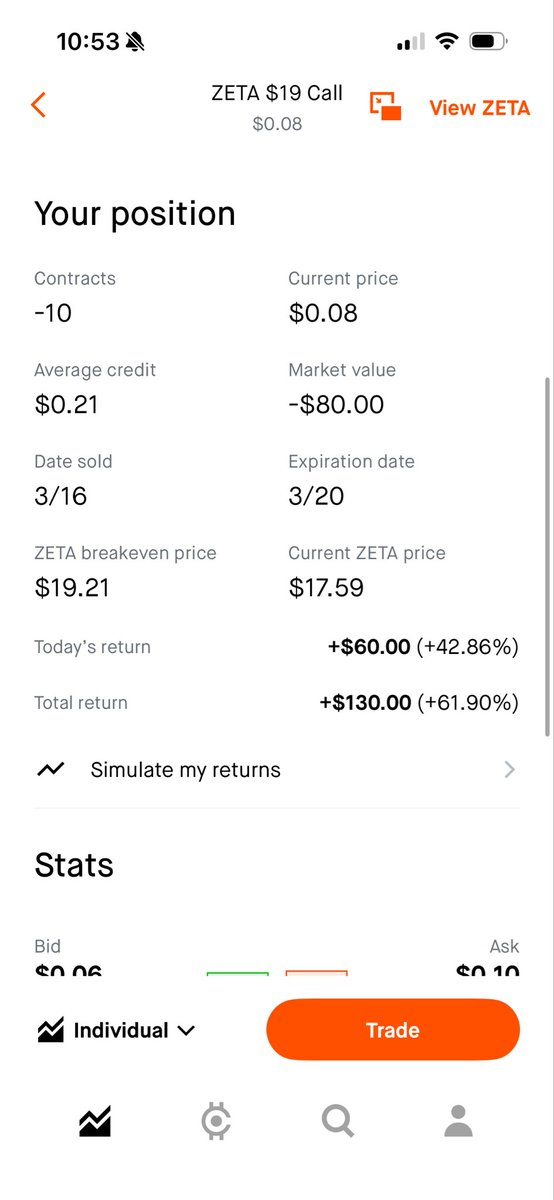

I think I’m hitting my flow state when it comes to selling option.

$AAPL $HOOD $ZETA

English

English

English

im not trolling when I ask this… can someone really find me a $nbis shareholder that actually dives deep into the business the way $iren holders do?

I can’t find a single $nbis shareholder that holds up to @Agrippa_Inv @bitcoinbutcher1 @FransBakker9812 @jiahanjimliu

I actually see no critical thinking from them (or so who I follow)

English

@LandoInvests They will probably upload to YouTube page but might take a few days

English

@Agrippa_Inv @IREN_Ltd Jealous! I have no IREN gear, i think I qualify based off my share count lol

English

@dylan_teeter @IREN_Ltd Good marketing is memorable.

Straight out of a Dale Carnegie talk. Let people talk about themselves

GIF

English

Pod will be a banger. All Jensen all the time - from GTC!

Up soon…

English

@dylan_teeter @Agrippa_Inv Oh gotcha, thought IREN was red. I’m outperforming yall this year.

English

@JustusFult99485 @Agrippa_Inv IREN up YTD. He’s up massively last year. Same here

English

@Agrippa_Inv I’m out performing you with these IQ points little buddy.

English

@Agrippa_Inv Well said. Nebius Group started in 2024. Dan and Will was running around the world 5-6 years prior locking up power and land. Laying the foundation to the IREN platform. I also agree they are very different companies. People love to compare the two but I think IREN is one of one.

English

Why I’m Not Invested in $NBIS

First of all, let me make one thing clear: contrary to what you might think, I’m not an $NBIS bear. But then again, I’m not invested either… and for good reason.

Nebius positions itself as a holistic cloud platform with superior software technology that caters to AI-native start-ups and enterprise clients.

That in and of itself isn’t a problem, but it means they're directly competing against the largest hyperscalers in the world, who are also targeting that exact cohort with their own set of software solutions (Google Cloud, Microsoft, etc.).

Nonetheless, if $NBIS can successfully differentiate itself with its core offerings, it could gain some pricing power, which is the company’s best shot at one day becoming profitable.

The problem is, $NBIS is VERY far away from that…

Looking at the last quarterly filing, the company’s gross expenses + depreciation equaled ~110% of its revenues. In other words, these two cost categories exceeded the value of the underlying revenues ($249.2m vs. revenue of $227.7m).

To be fair, last quarter Nebius still used a 4 year depreciation schedule on GPUs, which is rather short and overstates depreciation.

Adjusting for a 5 year depreciation schedule (industry standard) leads us to $144.6m of depreciation. Then, adding gross expenses of $68.5m on top gets you to $213.1m, which equals 93.5% of revenues.

And keep in mind, this figure does NOT include the hundreds of millions in costs spent on SG&A, R&D, and financing (interest).

So what’s my point with this?

The problem is, these are STRUCTURAL costs, the kind that scale with revenue, meaning you can’t easily grow out of them through sheer scale.

My point is that $NBIS' pricing power is nowhere to be seen, at least not relative to its costs.

Now, most $NBIS investors would probably argue that we are still "early" and that pricing power will show up eventually.

My problem with that argument is that the company seems to be allocating a very large chunk of its pipeline towards servicing hyperscalers through bare metal offerings, the kind of “bulk” service that does NOT command significant pricing power.

That means, fundamentally speaking, $NBIS is likely very far away from actually becoming profitable.

And while right now everyone is focused on headline figures like ARR, the market’s patience will run out eventually... it ALWAYS does for every company.

One day, the market will demand to see real profits flow down to the bottom line, and I’m not sure if $NBIS is structurally positioned to deliver on that any time soon.

To make matters worse, investors can’t even model out the economics of these large hyperscaler deals, because management provides absolutely 0 information on anything except headline figures.

We don’t even know the CapEx associated with these deals, or at the very least, the number of GPUs they have to purchase to fulfill their end of the bargain.

Contrast that with a company like $IREN, which gives you all the necessary information to build an entire P&L and cash flow model over the full course of the contract length, which is exactly what I’ve done extensively for our subscribers on Substack.

I have a VERY good idea of how much actual post-tax net income $IREN is making in every year of their hyperscaler contract.

There are other reasons that further point in the same direction, but I won’t get into them right now.

If they fix their cost structure one day, I’m happy to reconsider my stance.

But as of today, their “black box” approach to publishing details on their largest deals makes them uninvestable for me.

English

@StockSavvyShay Is this on top of the NVDA 2 billion worth of shares?

English

$NBIS prices an upsized $4B convertible note at very low rates (1.25% due 2031, 2.625% due 2033) with conversion premiums of ~57% above current price.

Dilution is contained (~9%) while investors fund billions of AI infrastructure buildout with a clear bet on upside.

English

Dylan retweetledi

As a follow up to my @Agrippa_Inv post.

Childress can hold ~154k B300. Current guidance reflects 17k at Childress.

154k-17k=137k incremental B300 GPUs that require lower cap ex retrofits and come quicker to market.

Current guidance is ~$3.7B

The 137k GPUs will result in ARR of $3.425B to $4.11B if they generate $25k to $30k ARR.

So people can make fun of "legacy" chips but the reality is ARR will double with Childress alone. We have plenty of time to install Rubin.

$7B-$8B guidance is coming soon.

Sweetwater, OK, and all the unannounced pipeline is the cherry on top.

$iren remains misunderstood. More for the few.

English

@bitcoinbutcher1 @Agrippa_Inv Agrippa is a legend, the level of detail is amazing! I don't see any wall street analyst doing this level or DD. Retail> wall street. Air cooled data centers will be a cash cow for IREN.

English

@Agrippa_Inv with another banger in the link below.

Lot's of potential for the 450 MW of remaining air-cooled Childress to supercharge the $iren flywheel versus the 160 MW British Colombia ops.

One thing I wanted to press on from his post; guidance recently released.

Management updated guidance from $3.4 to $3.7B which @Agrippa_Inv detailed.

Previously Canal Flats and Mackenzie represented $1.0B ARR with 40k GPUs for $25k ARR

Contrast that with the new guidance estimating $1.3B ARR for 50k GPUs for $26k ARR with Canal Flats removed and Childress added

At first glance, that's a 4% increase to pricing. Cool, right? You also need to consider that the recent GPUs cost $70k versus $60k in the fall; 16.6% higher.

@_Sgr_A_Star has multiple posts showing the hourly rates of H100 (an older generation GPU) being up in excess of the 16.6% GPU cost increase.

My gut feeling tells me @danroberts0101 continues to sand bag guidance. Time to compute remains too valuable and rare for customers. They will tolerate pass throughs until the supply shortages resolve themselves.

open.substack.com/pub/agrippainv…

English

@TheTechInvest @Agrippa_Inv I’m still working my through it. His level of detail is next level and I love it! @Agrippa_Inv

English

🚨 In a new deep dive, @Agrippa_Inv states that:

" $IREN is going to make BILLIONS of actual net income over the coming years… not just meaningless EBITDA or top-line figures, but real profits flowing to the bottom line.

If anyone is the next hyperscaler, it’s $IREN."

Worth a follow!

𝐀𝐠𝐫𝐢𝐩𝐩𝐚 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭𝐬@Agrippa_Inv

New $IREN Deep Dive: Childress Unlocked I’ve spent the last couple of weeks writing the most important $IREN deep dive I’ve published to date. Air-cooling at Childress is a MUCH bigger deal than the vast majority of investors and analysts realize. Honestly, $IREN price targets across the board should be well above $100 at this point. But Wall Street missing the forest for the trees is nothing new. I’ve extensively modelled out the company’s near-term pipeline using conservative assumptions (below management’s guidance), and it’s clear as day that the market isn’t properly pricing in $IREN's industry-leading earnings power. $IREN is going to make BILLIONS of actual net income over the coming years… not just meaningless EBITDA or top-line figures, but real profits flowing to the bottom line. If anyone is the next hyperscaler, it’s $IREN. Remember, real hyperscalers are actually profitable… At the same time, every investor should be aware of looming industry risks that affect all neo-clouds in the sector and evaluate how they could impact the investment thesis. That’s exactly what I’ve done for all our readers. These are the topics this new report covers: ➞ Breaking down the new GPU orders + new guidance ➞ Implications of air-cooling ➞ Extensive pipeline modelling ➞ Comprehensive analysis of the new $6b ATM ➞ Risks to the investment thesis ➞ + Plenty of bonus topics This 40+ page mega deep dive covers everything $IREN investors should be aware of today. It’s written in a very reader-friendly way, with many graphics & embedded video clips throughout. I chuckle when I read so-called “analysts” on X give their takes on $IREN after doing nothing more than surface-level analysis (at best). Most investors have no idea where this is heading… If you’ve read the new deep dive, I’d love to hear your feedback in the comments. Appreciate all of you, cheers! ✌️ agrippa.investments/p/iren-childre…

English

I don't see anyone calling for 300k BTC this year which makes me believe it is going to happen. BTC has a way of doing what the least amount of people expect. Don't fade @AlemzadehC $BTC

“Coosh” Alemzadeh@AlemzadehC

Updated Cycle Count

English