🚀🚀🚀

5.4K posts

🚀🚀🚀

@equitycaller

I buy for myself 27yrs in equities. Ex FPI emergng mkts for 8 & head of equities broking for 13yrs.Working on my own now. Simple ideas lead to best investments

🚨 GUJARAT THEMIS BIOSYN: THE ₹3,038 CRORE BET NOBODY IS MAPPING BSE: 533329 | CMP ~₹364 | Mcap ₹4,018 Cr | Promoter: 70.9% A fermentation company from Gujarat 🇮🇳 just committed 75% of its own market cap in back-to-back acquisitions within 30 days. 💰 ₹1,738 crore for 🇫🇷 Sanofi's global TB portfolio. 💰 ₹1,300 crore for an 85-year-old 🇯🇵 Japanese biotech. Zero cash deals. All debt + equity. Two continents. 55 countries. 359 🇯🇵 Japanese employees. 13 anti-TB brands. A proprietary ADC conjugation technology with a PENDING 🇺🇸 US PATENT. Plasmid DNA manufacturing. 3 🇺🇸 FDA-approved plants. The pre-acquisition GTBL had 2 customers accounting for 90-95% of total sales. One contract loss away from collapse. These acquisitions aren't optional. They're existential. Here is the complete forensic. 👨👦 THE FAMILY & THE EMPIRE Dinesh Shantilal Patel (Patriarch) & Dr. Sachin Dinesh Patel (Son/CEO). Combined: 34 directorships across manufacturing, distribution, and biotech. Mumbai-based 🇮🇳 pharma industrialists. Decades deep. Two listed entities: → Gujarat Themis Biosyn Ltd (GTBL) → fermentation biotech → Themis Medicare Ltd (TML) → injectable formulations, APIs 14+ private companies under the family, but one is the key: Vividhmargi Investments Pvt Ltd (VMIPL). It sits at the center of the preferential warrant issuance and the related-party transaction approvals. 💊 THE ABORTED MERGER On Nov 18, 2024, TML agreed to acquire the remaining 76.8% stake in GTBL. A full amalgamation. Months later, both boards abruptly withdrew it. Official reason: "strategic desire to focus on TML's core domestic formulations." The real reason? Within months of killing the merger, GTBL announced ₹3,038 Cr in debt-funded acquisitions. If the merger had gone through, TML's deteriorating balance sheet would have been merged with GTBL's new acquisition debt. They killed the merger to isolate the debt on GTBL and protect TML's listed entity. 📉 THEMIS MEDICARE: THE DISTRESS DRIVING THE LOOP To understand the cross-funding mechanics, look at TML's standalone numbers: → FY22 PAT: ₹61.56 Cr | FY25 PAT: ₹23.92 Cr (Collapsed 61%) → Debtor collection period: 159 DAYS → Q2 FY26 EBITDA: NEGATIVE ₹3.1 Cr The sister company was bleeding. TML needed cash. GTBL needed debt capacity. The family had to move money in both directions simultaneously. 🔄 THE CAPITAL MOBILIZATION LOOP Layer 1: TML issued convertible warrants to VMIPL (promoter vehicle). Total raise: ₹47.28 Cr. Layer 2: TML sold 30L GTBL shares from its treasury to Dr. Sachin Patel personally for ₹130 Cr cash. This extracted liquidity directly into TML's treasury while concentrating GTBL ownership in Sachin's hands pre-acquisition. Layer 3: TML secured postal ballot approval for material Related Party Transactions (up to ₹250 Cr with VMIPL/Themis Distributors). Three simultaneous moves to engineer a capital loop while dropping ₹3,038 Cr in acquisition announcements. 🥇 DEAL 1: SANOFI'S GLOBAL TB PORTFOLIO → Price: 💰 €158M (₹1,738 Cr) | Multiple: 2.5x revenue (discount to the 3-5x industry standard). → Target: 13 established anti-TB branded generics (Rifampicin-based). WHO Essential Medicines. → Presence: 55+ countries. Revenue: ~₹682 Cr. ⏳ The Transition Chasm: 13 brands × 55 countries = ~715 individual regulatory transfers. Sanofi continues distributing via Transition Services Agreements (TSAs). TSA fees will suppress gross margins and delay full revenue integration for 18-24 months. Anyone modeling immediate revenue accretion is wrong. 🥈 DEAL 2: MICROBIOPHARM JAPAN (MBJ) → Price: 💰 JPY 21.5B (~₹1,300 Cr) | Multiple: 2.28x revenue (PE exit price). → Target: 100% of MBJ. Seller: T Capital Partners (🇯🇵 PE). → Assets: 359 employees, 3 🇺🇸 FDA-approved plants, 85 years of institutional knowledge. 🏭 THE THREE PLANTS & ONCOLOGY CATALOG 1. Iwata: Mid-scale fermentation & R&D scale-up. 2. Yatsushiro: Large scale commercial. High-containment workshops for ADC payloads (the most toxic cancer drug components). 3. Kiyosu: Acquired from Astellas. Recombinant proteins, peptides, and Plasmid DNA manufacturing (the upstream backbone for gene therapy + mRNA vaccines). MBJ produces Anthracycline Analogues (Doxorubicin, Daunorubicin) - the most widely used chemo drugs on earth. But they are also developing Ansamitocin P-3, an ADC payload precursor used to make the warheads that kill cancer cells in antibody-drug conjugates. 🧬 THE CROWN JEWEL: ez-ADiCon™ & THE US PATENT Most ADCs rely on chemical conjugation, generating a heterogeneous mixture with unpredictable toxicity. MBJ’s ez-ADiCon™ is a fully enzymatic, site-specific process yielding a Homogeneous DAR4 conversion rate of 93%. It requires NO antibody mutagenesis. 📜 The US Patent (US20240191272A1): Filed in 2022 under T Capital's ownership. It covers this exact enzymatic mutant process. 🇺🇸 Regeneron Pharmaceuticals has actively cited this patent family in their own therapeutic filings. If granted, GTBL owns a US patent on a superior conjugation platform in a market where ADC licensing deals routinely hit $1B+. 💼 THE LICENSING PLAY GTBL isn't just buying a manufacturer; they are buying a licensable tech platform. MBJ offers Track 1 (Contract Synthesis) and Track 2 (Technology Licensing). Every pharma company developing ADCs is a potential licensing customer. (Note: MBJ also hides a 5th business line: a proprietary P450 enzyme library that replaces multi-step chemical synthesis with single-step hydroxylation, offered as a contract service to global pharma). 🤝 THE GEDEON RICHTER BRIDGE The Patel family operates a JV with Gedeon Richter (€4.2B 🇭🇺 pharma giant). When GTBL needs to commercialize MBJ's oncology APIs or Sanofi's TB brands in Europe, this JV is the regulatory and commercial bridge. 📊 THE BASE BUSINESS (Q3 FY26) → Revenue: ₹434 Cr (+9.7% YoY) | EBITDA Margin: 49.13% → Pre-acquisition D/E ratio: 0.12. They are printing cash from their base business, which recently completed a facility expansion explicitly tied to "forward integration into API production" (which we now know meant MBJ). 🗺️ THE POST-ACQUISITION GTBL If both deals close, GTBL transforms from a domestic fermentation player into a global biotech platform: → Revenue: ~₹2,850 Cr run-rate by FY28. → Capabilities: Indian commodity fermentation + Japanese Oncology APIs + Plasmid DNA + Proprietary ADC Conjugation IP. → Geography: Manufacturing in India/Japan, commercial footprint across 55+ countries, EU bridge via Richter, and US IP jurisdiction. 🎯 THE RISK STACK → Leverage: Committing ₹3,038 Cr on a ₹4,018 Cr Mcap. Projected debt >₹2,000 Cr against FY25 borrowings of just ₹29.64 Cr. Can 49% base margins support this debt servicing if a top-2 client walks away? → Regulatory/Cultural: ⚖️ Japan's FEFT Act approval uncertainty. Plus, integrating an 85-year consensus-driven Japanese workforce with Indian management. → Key Person Risk: 10 named MBJ scientists hold the institutional knowledge for the US Patent. Post-acquisition attrition destroys the strategic value. → Sanofi Drag: 18-24 months of TSA fees suppressing margins while 715 global regulatory transfers clear. → The TML Shadow: The aborted merger proves the promoters are deliberately isolating risk. If GTBL stumbles under the debt, TML will not be there to bail it out. 👁️ WHAT TO WATCH: → June 4 postal ballot result (borrowing limits). → Q2 FY27: MBJ closing & FEFT Act notification. → US Patent grant timeline. → Key person retention (are the 10 inventors staying?). → Kiyosu plant utilization (is Plasmid DNA at 20% or 80% capacity?). The Patel family is betting the entire company. 70.9% promoter holding means they're betting on themselves. 🔍 Speedy never satisfies its curiosity enough. ⚠️Speedy Proprietary Database, MicroBiopharm Japan corporate website, T Capital Partners press releases (July 2, 2021), Kirin Holdings IR, Toray Industries disclosures, USPTO (US20240191272A1), 🇺🇸 Regeneron patent citations, 🇯🇵 Japan MOF FEFTA records, 🇭🇺 Gedeon Richter Plc annual reports,Speedy director search, 🇫🇷 Sanofi Press Release. Not investment advice. DYOR.

I urge every youngster to rent an apartment over going for a home loan. My suggestion is mostly applicable for middle class people who are looking to build a career and make more money. I recently rented an Apartment in Bangalore. I am starting the Annual Membership Program and I got a sexy apartment because I want to work in the best possible environment. I am going to be paying an annual rent of Rs 18 lacs for this apartment. The current market value of the apartment is Rs 5 CR+ so I am paying an yield of around 3.5% to the owner. I would have had to pay a bank around 8-10% for the same apartment that shall be mine after 12-15 years. Why would I borrow money at 10% to avoid paying money at 3.5%? I can work better with peace of mind knowing that I am not tied to a bank loan or any legal obligations. I can stay in luxury properties today and make more money instead of paying money to the bank and live in poorer environment. I am urging you guys to chase a sexy lifestyle and a lot of flexibility or you would not be able to work at your full potential. Stay in rented properties and get rich first. Then buy properties in cash later in life. NEVER INVOLVE THE BANK to get a house.

GUJARAT THEMIS BIOSYN #GUJARATTHEMISBIOSYN TO ACQUIRE 100% OF MICROBIOPHARM JAPAN VIA WHOLLY OWNED JAPAN SUBSIDIARY FOR JPY21.5BN (~₹1,300 CR); DEAL CLOSING EXPECTED IN Q2 FY2027, SUBJECT TO REGULATORY APPROVALS. In all the brands bought from Sanofi and the newly acquired Japanese oncology drug API. What is the missing link between API to final branding and sales???? Clue - it's already inherent in the group.

#nestleindia nestle India is in a structural bull run. The current market conditions and the forecast for increasing disparities in income are the exact recipe for better turnover for a fmcg with high roe like nestle. Step out of consumer Discretionary. Step into consumer staples. The increased capacity in Maggi noodles will bode very well going forward

#adffoods adf foods.. Great nos. Infact the contribution of the new Surat facility was literally only in the last 3 days of March. Because the plant was only active for the final few days of the quarter, the strong 35% YoY revenue growth was primarily driven by the core existing business and strong demand in the US nd UK Q1 FY27 will see a full 3 Mos of the new capacity (30% of it ie. ) probably an additional 30-40 crore per quarter initially till it moves to full capacity. This facility is the cornerstone of ADF’s plan to hit a ₹1,000 crore revenue mark by FY27. Essentially, the plant needs to contribute about ₹20–₹25 crore per month once it hits a steady state, and Q1 will be the first real test of that ramp-up phase. The SBI AMC buy of 2.2m shares has made a base for the stock @ 260 It's ready to 🌋

This entire premise that SIPs are primarily responsible for the FPI outflows and inr depreciation is absolutely humbug. FPIs wd sell if they had to sell and the inr wd depreciate anyways. The mkts may be under performing relative to other regions but they're hugely outperforming our past when even a fraction of such sell offs would have annihilated the stock markets and destroyed the inr too. Atleast we taxed the FPIs on the way out however some lax taxation changes are needed. It's stupid to abuse the retail power. Our markets have never had more depth and it's not like FPIs never return. They have an annual reallocation of funds which might give India a better weight due to relative underperformance. #keepthefaith

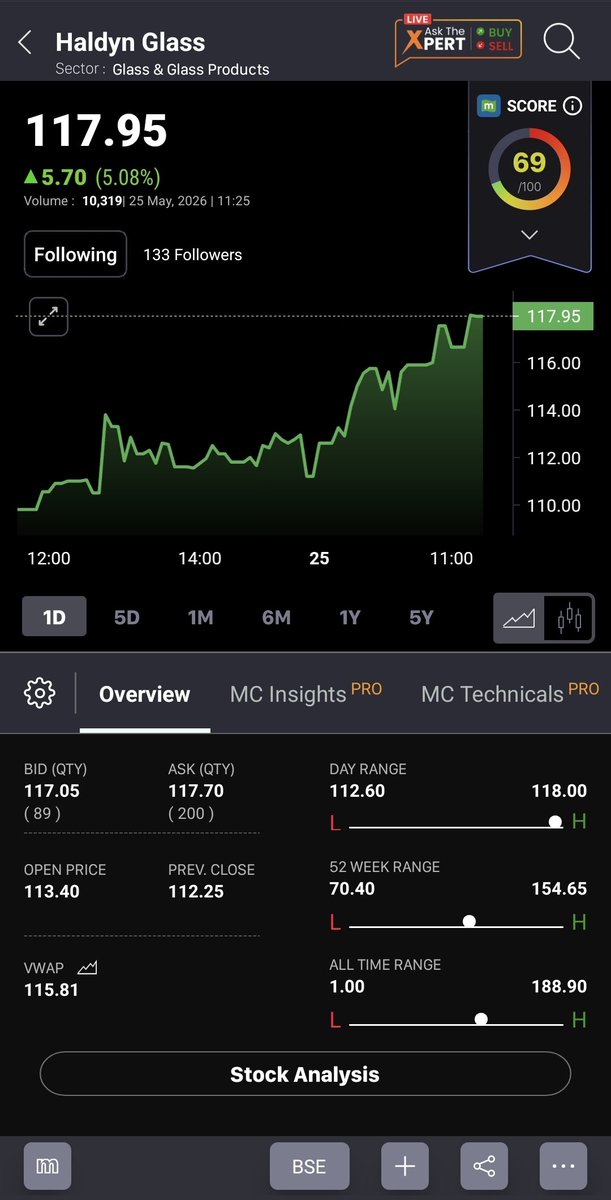

Wow haldyn glass

@NeerajCNBC Capital’s Adani buys show active stock-picking by FIIs. Meanwhile DIIs are adding Reliance — that split reflects different risk horizons and information sets. Remember: foreign funds chase returns, not loyalty; they rotate when fundamentals or risk perception shift.

#THEMISMEDICARE not bad for a horrible mkt day themis medicare