Sabitlenmiş Tweet

Been holding this bad boy from whole last year and have only added on dips. Now all of sudden it became one of my biggest holding!!! $AAOI $LITE

English

Equity Climb

877 posts

@equityclimb1

| Tech Research | Tech & Semiconductor Insights | I post stocks that can 10x |Not Financial Advice | $NBIS @17 @APLD @4 $BE @17 $AAOI @15 $AEHR @20

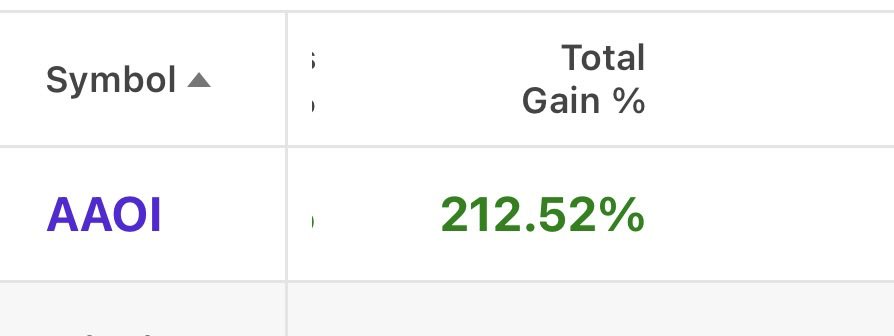

$AAOI might be undervalued relative to its strategic value. It should be at $200+ atm

主流叙事:"NeoCloud 利润已被定价" SemiAnalysis 反驳: VR NVL72 价值上限 $12.25/hr,现价 $4.90/hr 租金上行空间巨大 主要因为 NVDA 没把 capex 转嫁给 NeoCloud,NVIDIA 需要通过给 NeoCloud 留利,来支持这些“亲儿子”去挑战 Amazon、Google 等自研芯片的云巨头,NeoCloud 处于“拿低价硬件、收高价租金”的黄金窗口期。

So why did $NVDA invest in $NOK and did a partnership with $FJTSY ? And why did $NOK acquired Infinera ?

I have positions in all three but I really like $CLS thesis here and we bought alot around 267 and now its up at 350

@TheValueist Based on this, 2 stocks to watch out for $AAOI and $BE. Bloom energy hydrogen cells don’t have intermediate cost to convert to AC to DC it’s just plug and play which is huge advantage for them when next generation of GPUs arrive compare to turbine power

Samsung Electronics reported DRAM ASPs rising roughly 90-95% sequentially from Q4 to Q1, signaling a sharp tightening in memory markets tied to AI-driven demand. The reinforces how memory from companies like $MU and $SNDK alongside GPUs are becoming a key constraint in scaling next-generation data center infrastructure.