Eric G retweetledi

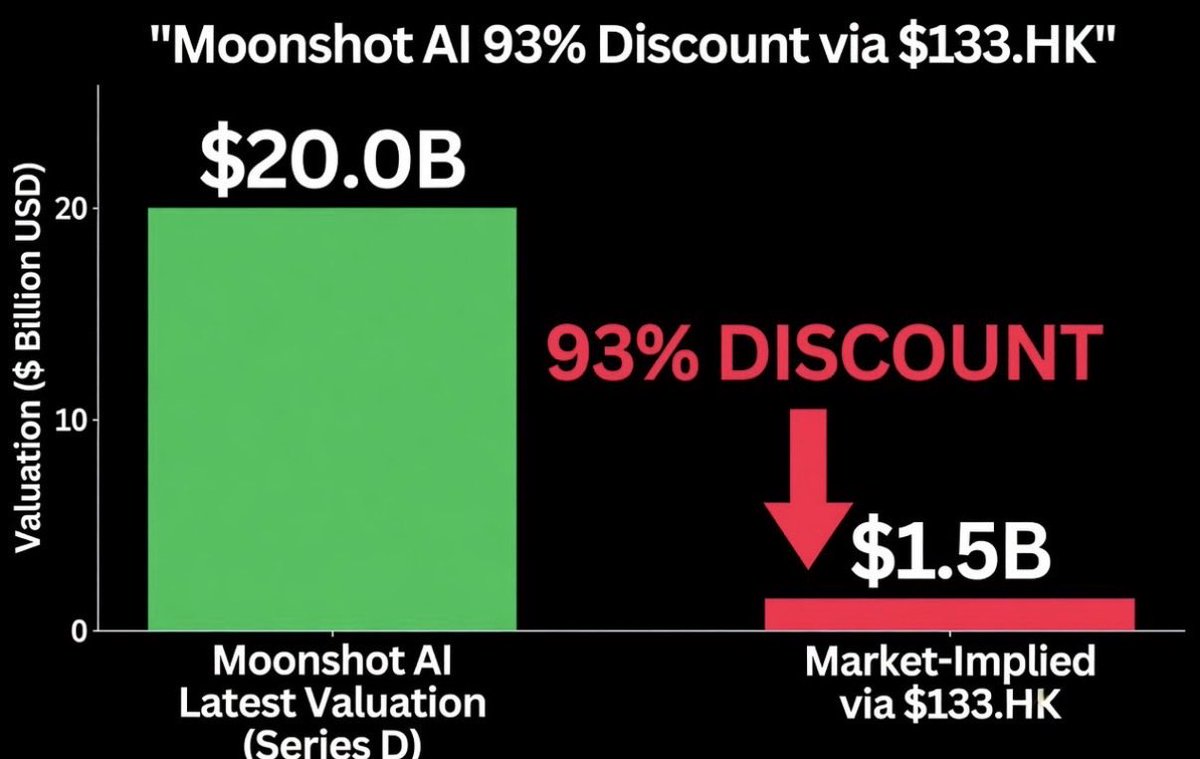

We like $133.HK, it’s a time machine that gives investors exposure to China’s leading agentic AI model associated with Cursor/SpaceX at a $1.5bn valuation. Thanks to activist involvement, you also get paid an 8% dividend yield to wait for the re-rate. Full writeup: maiuspartners.com/p/back-to-the-…

English