fabiorbb 🇺🇦

328 posts

LOL. Nomura initiates $SOI coverage and gives it a EUR 250 PT.

Back when I went long at ~€43, after the first +25% institutions were saying not to buy and that there’s nothing new.

Now 2 months later they’re giving price targets ~6X+ my thesis post.

Serenity@aleabitoreddit

Changed my mind about Soitec ( $SLOIF ) and took a sizable position ~43 for CPO exposure. $NVDA GTC next week biggest catalyst pushing photonics and this architecture. ~1.5B euros MC. Trading at 1x book value and ~2x P/S (very depressed valuations) Genuine monopoly over substrates side for CPO (typically very premium valuations for photonics + even extra premium for monopoly status) Algos and analysts might get confused over market share but it’s an actual monopoly over SOI substrates since they give licenses to other players like Shin Etsu for diversification sake eg. $TSM doesn’t like just 1. I don’t think institutions will wait until next year to frontrun these names like Soitec or $TSEM (and most probably haven’t even heard of these names like $AXTI yet) This timing would be buying the likely bottom of the depressed smartphone cycle, while getting full upside of CPO mid-late 2027 + $NVDA GTC catalyst next week. I personally think it’s a 3x from here so I went long.

English

@aleabitoreddit You are a legend, bro. Sad to have sold AXTI too soon 😪

English

Did you listen anon?

The fact that $SIVE is up 600%+.

But still can 10x from here in a year... once ~ $AAPL, $JBL, and $MRVL require mass production of their lasers in 2027.

Is incredible.

Probably my most legendary thesis post since $AXTI.

Serenity@aleabitoreddit

The more I look into Sivers < $SIVE / $SIVEF > the more I wonder: How is the laser company for the hyperscaler photonic supply chains… Valued at ~$200M USD MC? All the companies that buy and repackage their lasers are now worth $1-4B+? Pre-product SV AI companies are worth billions? Pre revenue Photonic companies in development phase line $LWLG are worth $1B+? Yet the company that makes the silicon photonics/CPO scale up & scale out work. And has actual revenue. ~$200M… Reminds me of early $AXTI when I had zero clue how a company worth $500M MC controlled the InP substrate/feedstock supply chain for photonics. Either I’m completely wrong… or this is the most undervalued and unknown photonics company on the market.

English

@slabecry @Albert_TheVoid @OmerCheeema What’s your sources or thesis behind your statement that MEMS components are inside LITE ones?

English

Wow. A microcap optics company that's profitable. I like it.

English

Wow $SOI is now the 16th name...

I've done a mininthesis post on that returned over 100%

Year to Date.

The most recent two were $ALRIB and $RPI.

Why does everything around me keep doubling?

Serenity@aleabitoreddit

Changed my mind about Soitec ( $SLOIF ) and took a sizable position ~43 for CPO exposure. $NVDA GTC next week biggest catalyst pushing photonics and this architecture. ~1.5B euros MC. Trading at 1x book value and ~2x P/S (very depressed valuations) Genuine monopoly over substrates side for CPO (typically very premium valuations for photonics + even extra premium for monopoly status) Algos and analysts might get confused over market share but it’s an actual monopoly over SOI substrates since they give licenses to other players like Shin Etsu for diversification sake eg. $TSM doesn’t like just 1. I don’t think institutions will wait until next year to frontrun these names like Soitec or $TSEM (and most probably haven’t even heard of these names like $AXTI yet) This timing would be buying the likely bottom of the depressed smartphone cycle, while getting full upside of CPO mid-late 2027 + $NVDA GTC catalyst next week. I personally think it’s a 3x from here so I went long.

English

@aleabitoreddit People bringing this kind of criticism just show their ignorance in the field, so they can’t really face your thesis and counter argue; just ignore them

English

No. This type of BS mindset needs to stop.

What I do is point them out to retail first before the 100-500%+ returns.

US institutions like Point72 or Apollo would have bought them out eventually.

1. $IQE went up because they're sitting on the most latent merchant capacity in the world for InP reactors back at a 100M euro marketcap. While companies like Landmark were trading at $3.8B.

They were also the supplier to $LITE, and photonics/epiwafer demand took off this year.

2. $SIVE went up because they had new deals with $JBL and O-Net.

But they were already unknown as the laser supplier to $MRVL's CPO program when I first went long.

American institutions like $AVGO would have likely just bought the company directly like what Qualcomm did with Alphawave over in the openlight side of things if I didn't bring attention to it.

Then Swedish retail investors wouldn't get any of the upside.

3. $ALRIB went up because their earnings sent their P/E down to fwd 26, despite holding a duopoly in the MBE category with $VECO.

This combined with new SiPH equipment, as well as $IQE + QD Laser (for quantum dot) being their customers.

This was combined from raw information discovery of the decade that $MSFT Quantum was their buyer.

You don't see direct hyperscaler frontier programs in quantum computing dependant on some <$1B MC company.

4. $SOI is up 208% because it has an unknown monopoly over SOI substrates for silicon photonics and CPO.

This was more information synthesis combined with timing the bottom of their legacy cycle.

5. $RPI went up because of earnings and AI hardware usage.

I was just the very first person to point it out.

I projected 55% revenue growth compared to 14% from analysts. They did 58%.

I just gave retail the chance to buy it before institutions.

The stock would have gone up off of pure fundamentals without me posting my thesis because you don't do $511m in revenue off a $500m MC as a fabless company.

I'm just giving retail the all the information discovery before institutions have a chance to find it and price it in.

This is a completely different model than the same institutions telling you to buy index funds or stocks that already went up 1500% so you're exit liquidity.

Deo Non Fortuna@filiusveritatis

@aleabitoreddit They only went up those percentages because of your and other X accounts attention to those stocks combined with them being undervalued

English

If you want to trade hyperscaler qualification cycles…

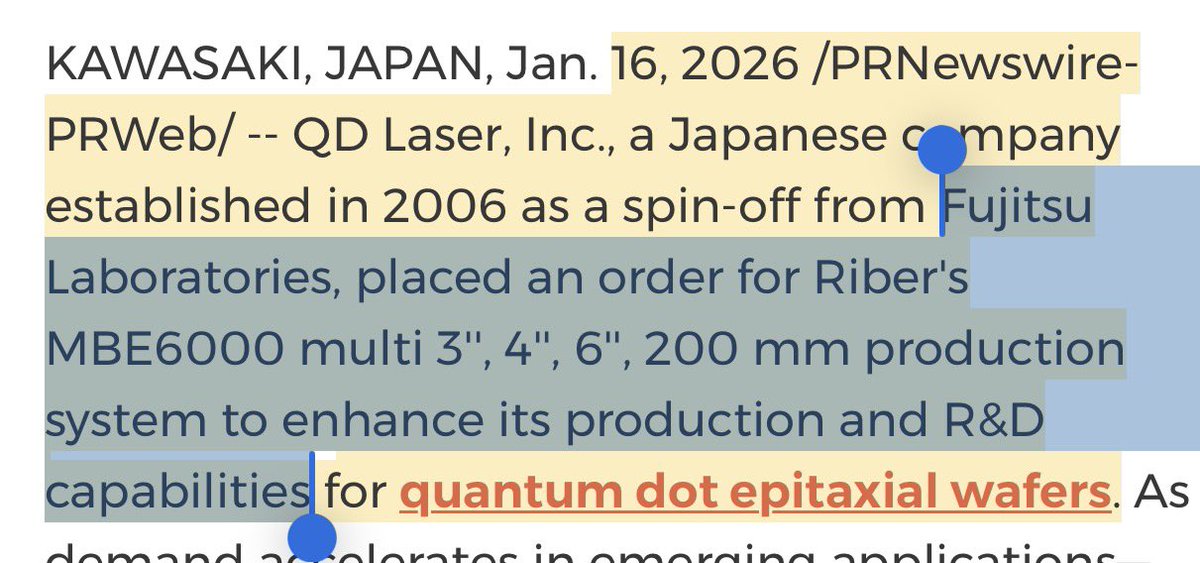

And quantum dot like QD Laser (TYO: 6613) up 226% YTD:

IMO safest way to do it are their unknown MBE machine suppliers like $ALRIB early on.

Then pivot to pure play lasers later when they move from qualification -> volume orders.

I mentioned earlier $MSFT quantum was Riber’s undisclosed hyperscaler customer.

But QD laser (getting popular) is heavily reliant on Riber too for their quantum dot program.

I’m not a fan when it comes time to volume production (eg. $AIXA vs the actual volume producers) since machines don’t capture downstream revenue.

But if you want to benefit from capex R&D cycles… eg. QD Laser absorbing capex costs (paying Riber) to build capacity

$ALRIB, $ASML, $AIXA type companies usually hits the balance sheet much earlier so you don’t need to wait 2-3 years for production orders.

Mooni Insight 💫@Semicon_player

@PhotonCap 일본 투자계 친구들이 QD LASER 에 엄청난 관심이 있더라고 이것도 한번 집중 탐구 분석 해보면 글로벌리 아주 넓게 좋을듯 쏘니

English

@aleabitoreddit You are the best, let’s keep riding man! Look, have you checked the products of ams-OSRAM? 👀

English

Yeah… I’m cooking super hard.

$AAOI +10.65%

People aren’t bullish enough after the new $LITE backlog report.

The demand visibility lasts past 2029 for optical companies…

Serenity@aleabitoreddit

I'm not sure people understand yet: $LITE backlog order fill into 2028 signals extreme demand. And a lack of capacity. Then by second order effect of hyperscaler demand spillover: Guess who is projected to have the largest 800G/1.6T capacity in America? $AAOI. They fab their own inp lasers, design their own transceivers, and assemble it. If $AAOI can execute on capacity ramp, that likely all translates into revenue due to everything being sold out. My $40B MC price target from $5B is starting to look more and more likely?

English

@aleabitoreddit What should we do at this point, hold it and hope for the better, or get out of the markets in light of the rationality?

English

The market are missing the implications from $NVDA investing:

$2B into $COHR for optical.

$2B into $LITE for optical.

and $2B into $MRVL for optical today.

Nvidia did this exact same playbook last year.

They realized the push to 800G/1.6T pluggables would exhaust the global supply of EML.

So they approached $LITE, $COHR, Sumitomo, and preallocated majority of production.

And we've seen this reflected in their share price with $LITE rising 955% since the major supply squeeze.

We're seeing the beginning of the same playbook happen now over the last month.

Just for a new architecture, this time.

As these deals included multibillion-dollar purchase commitments and future capacity rights.

So... what's next? CW/EML and CPO bottlenecks.

Nvidia just prefers to invest in downstream players. But the supply crunch happens upstream.

Laser suppliers from $MTSI, $SIVE, $LITE, $COHR, Furukawa, and Sumitomo are on overdrive.

Foundries from Win Semi, $TSEM, $GFS are likely on overdrive.

The entire supply chain benefits (eg. testing from $AEHR, substrates with $SOI).

But these two segments from foundries to ELS/CW laser chokepoints are likely to be the biggest beneficiaries.

Nvidia is the biggest signal of what's coming next; it's just a waiting period for the inflection point to hit.

English

This is why you need to have conviction before entering a trade.

If you knew $SIVE positioning in the CW laser space to Jabil, $MRVL Celestial, and others for CPO.

$250M MC as the light source chokepoint would be a joke.

High confidence we’ll see this end up like $AXTI in a years time since it this will be the architectural paradigm for cpo scale up.

Don’t care about volatility in the way up because I have conviction in how this plays out with photonics.

English

The Photonics Supercycle is here.

$NVDA is spearheading the next leap into CPO & Silicon Photonics.

And we’re only near the inflection point with chokepoints in the supply chains like Soitec ( $SOI ) or Sivers ( $SIVE ).

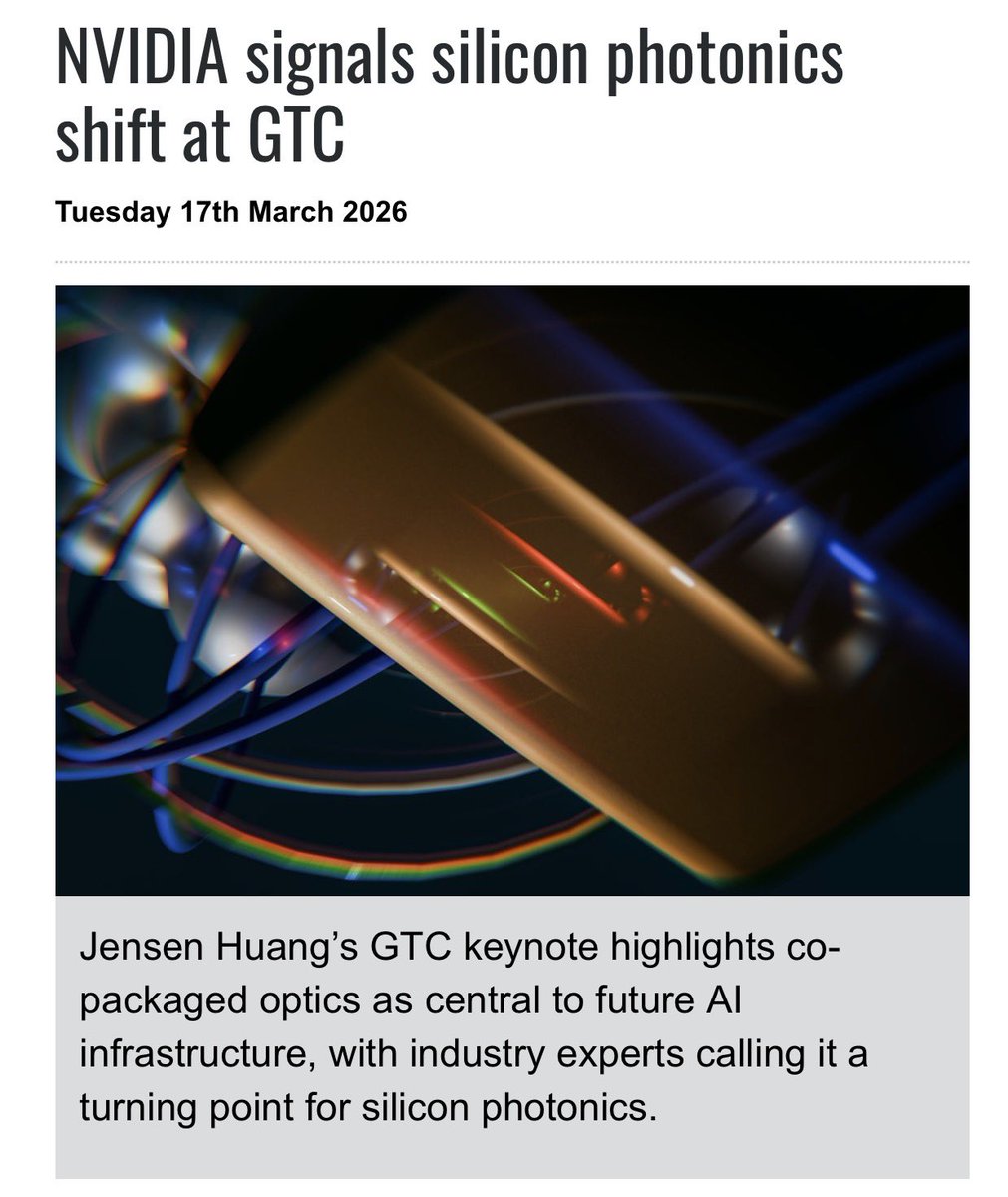

“NVIDIA’s update on the Spectrum-X switch with co-packaged optics is an important moment, confirming that silicon photonics is central to next-generation AI infrastructure.”

Despite a long-standing reliance on copper-based interconnects for scale-up systems, the company is now placing photonics at the core of its future platforms, including Vera Rubin Ultra.

This transition is expected to support increasingly complex configurations, such as NVL576 and future architectures like Kyber NVL1152.”

“Nvidia is already in production with Spectrum-X Photonics, which is co-packaged optics (CPO) Ethernet switch.

The company also announced the Quantum-X Photonics InfiniBand switch, which delivers up to 800 Tb per second of scale-out throughput using its proprietary scale-out interconnect”

Although copper is important, it can no longer alone can no longer handle AI-scale demands.

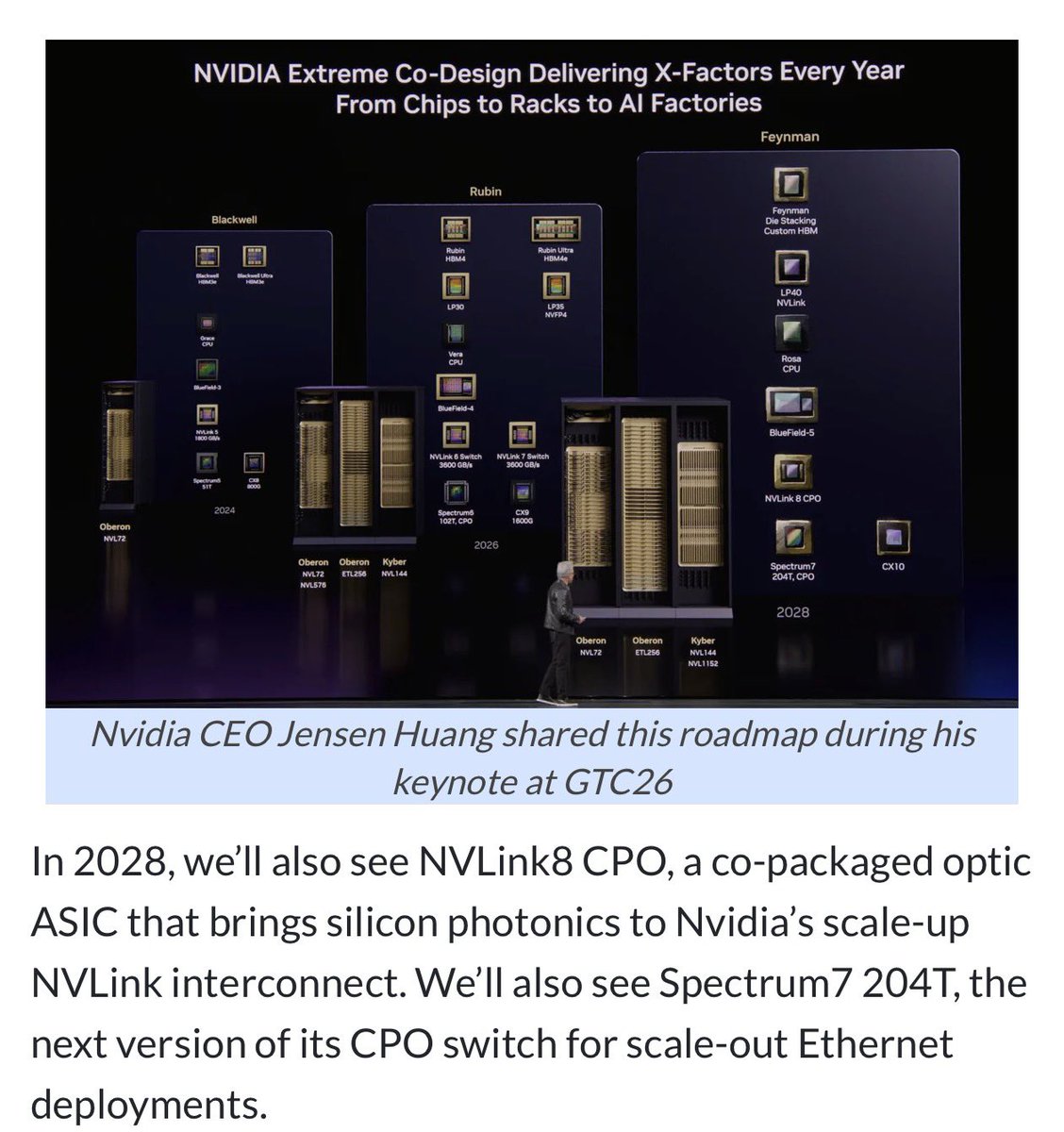

NVLink8 CPO is probably the biggest signal with $NVDA also bringing silicon photonics into its scale-up NVLink interconnect, not just scale-out networking.

CPO for scale-out is shipping now/2026, CPO for NVLink scale-up arrives soon.

The paradigm has shifted, and the bottleneck of AI infrastructure is now officially being solved by light.

It’s only a matter of time before markets find these chokepoints in the supply chains.

Then price them in.

Serenity@aleabitoreddit

The upcoming CPO / Silicon Photonics Bottleneck Cheat Sheet: $SIVE, Sumitomo, $LITE, $COHR, $AVGO, $MTSI, $AAOI - Light Source (CW DFB Lasers) $TSEM, $GFS, $UMC, $TSM, $INTC - SiPh foundry $NOK, $CIEN, $CSCO, $COHR - DCO $HIMX, FOCI (3363.TWO) - Micro-lens + Fiber Arrays $POET - Optical Interposers $SOI, $AXTI, Shin-Etsu - Substrates $FN, $ASX, Innolight, Eoptolink - Optical Packaging and Assembly $MTSI, $SMTC, $MRVL, $MXL - Analog/Mixed-Signal ICs $LWLG - Speculative Modulator Materials. $GLW, $APH, $TEL, $FIT, Fujikura - Connectors and Fibers $FORM, $KEYS, $VIAV, $AEHR- Test & Measurement $BESI, $SMHN, $ONTO, $CAMT - Advanced Packaging & Hybrid Bonding Many are private companies from Lightmatter, Ayar, Ranovus and others. Now... Everyone is asking... How do you profit? If you look at the forecast for CPO TAM, it's a straight line up, and next year is inflection point for CPO mass deployment. The alpha is capturing the rotation: From the current EML bottlenecks ( $LITE, $COHR type) to SiPh / CW DFB architectural winners for CPO. Highest upside potential are the ones that aren't included in current cycles. But that are in the next. Companies like $SOI, $SIVE, or $AEHR are perfect examples. Ride the current pluggable bottleneck like $AAOI. But the alpha is frontrunning institutions with the next CPO bottleneck. The capital rotation is inevitable.

English

@aleabitoreddit @aleabitoreddit what do you think about JX metals?

English

Was the first to talk about $AXTI in relation to photonics BOM/supply chains:

$IQE is very interesting too as one of the only Western suppliers.

Basically if you look at photonics flow on $GOOGL TPU/hyperscaler ASICs kinda looks like this (very likely, but undisclosed):

Optical Transceivers (highest BOM):

Lumentum/Cloud Light:

~ Vital / $AXTI-> $AXTI/Sumitomo/JX -> $IQE (Epi-Wafers) -> $LITE / Cloud Light -> $FN (Contract Manufacturing) -> $GOOGL TPU

Merhcant optical supply chain:

~ Vital / $AXTI -> $AXTI / Sumitomo / JX -> → $LITE / $AVGO / $COHR (EML) + $MRVL / $MTSI / Semtech -> Innolight/Eoptolink -> $GOOGL

So if you want moonshot-type photonics BOM / price-hikes stocks deeper upstream in the photonics BOM: $AXTI, $IQE and your way to go.

$AXTI had terrible fundamentals before but the recent Northland fundraising round cemented its run.

$IQE has terrible fundamentals now (Net debt £23.5 million) but is probably one of the most critical parts of the supply chain. If they manage to sell their Taiwan operations, wouldn't be surprised if it went up quite a bit just from their inp business.

There's £18m convertible notes (which is basically nothing), then there's 120 to 154m new shares (~12% to 15%), which is also kinda nothing relative to current size.

On the other hand, others $LITE and Innolight are probably more established.

TLDR:

$IQE -> seems critical to Western supply chains, $130MC. Net debt, if they sell Taiwan business -> strong re-rating or they might just dilute you anyway.

But if the Taiwan business fails to be sold, probably expect to be diluted to oblivion like Wolfspeed. So huge, huge, risk ad do you own research into risks.

But $AXTI and $IQE might are personally interesting to me (I do own $IQE).

English

fabiorbb 🇺🇦 retweetledi

fabiorbb 🇺🇦 retweetledi

Verissimo. Una strage che dura da un secolo almeno.

Ed anche in questo secolare scempio la logica e' quella secondo cui all'alleato "strategico" tutto e' concesso.

North Tustin, CA 🇺🇸 Italiano

fabiorbb 🇺🇦 retweetledi

you don’t actually have to respect all cultures

Visegrád 24@visegrad24

BREAKING: Iraq’s Parliament takes the first step to lower the legal age of marriage for girls from 15 to 9. The new personal status law being discussed is based on Sharia Law.

English