Filippo Garbarino

560 posts

Filippo Garbarino

@filippogarba

Chief Investment Officer, Investor, Lifelong Learner ---- I use Twitter as a journal for my thoughts on investing ---- not investment advice

Switzerland Katılım Aralık 2017

697 Takip Edilen296 Takipçiler

@robin_j_brooks This a testament to how much sentiment and positioning matter. Being contrarian at extremes is difficult but pays off very well

English

It's worth pausing to recall just how negative Dollar sentiment was a year ago. But here we are. The Dollar has been a much better safe haven than gold recently. Reserve managers are watching. They'll be cutting allocations to gold and going back into USD.

robinjbrooks.substack.com/p/why-has-gold…

English

@zerohedge Being a capex receiver $MU is better than being a capex spender $MSFT . However, the price decoupling has a ceiling as if ROIC disappoints, the spender will stop spending. Something's gotta give here

English

From Goldman's Delta-1 Desk:

Hyperscalers: This is poised to become one of the defining debates of the next few months. Markets have rarely rewarded companies allocating exceptionally large proportions of free cash flow toward capex during the build phase. This does not necessarily mean management is making poor long-term decisions; it simply means equity investors generally prefer immediate, tangible returns to distant, uncertain cash flows. Multiple expansion typically occurs during the harvesting phase, not the construction phase. The theory of reflexivity remains highly relevant in this environment. If hyperscalers continue to underperform while suppliers rally, boardrooms may increasingly question whether incremental AI investment is maximizing shareholder value. At some point, capital expenditure may slow and if one peer blinks, the market will immediately question whether others should follow.

English

@TSOH_Investing Stunning chart but the market is forward looking and is telling us that the future for $MSFT will not be like the past. Hope market is wrong as I am long $MSFT and $AMZN

English

@Proctooor I think the hyperscalers will have to blink on capex slowdown. The market will force this

English

@filippogarba my thinking too. This is getting to a cliff where something has to give. What's your take? Hyperscalers cutting or Micron at 2000$ and Msft at 250?

English

Being a capex receiver $MU is better than being a capex spender $MSFT . However, the price decoupling has a ceiling as if ROIC disappoints, the spender will stop spending. Something's gotta give here

English

@CapexAndChill Not alone. I sold $AMAT August last year, probably worse

English

Assuming its rage bait but still need to do it. This man woke up this morning to sell $META and $AMZN because they are down.

Options selling with Christian@optionscjp

I made a huge mistake the last year I’ve had over 50% of my acct in $META & $AMZN I’ve refused to buy the narrative that the capex spenders won’t be rewarded Well here we are today, day after day they are getting beaten down to a pulp.. I’ve been trimming them the last month or so And today I sold 500 more $Amzn @$229 and 100 more $META @$560 to free some capital for my other high conviction names Please note: I’m not at all bearish on these names and I will be covering those shares with some leaps or calls. Just exiting some for now. Still heavy in both names.

English

@ThierryBorgeat I agree 100%. Have been long $TDG since 2013, $HEI since 2020 and more recently $GE. This industry has created and will continue to create generational wealth for decades

English

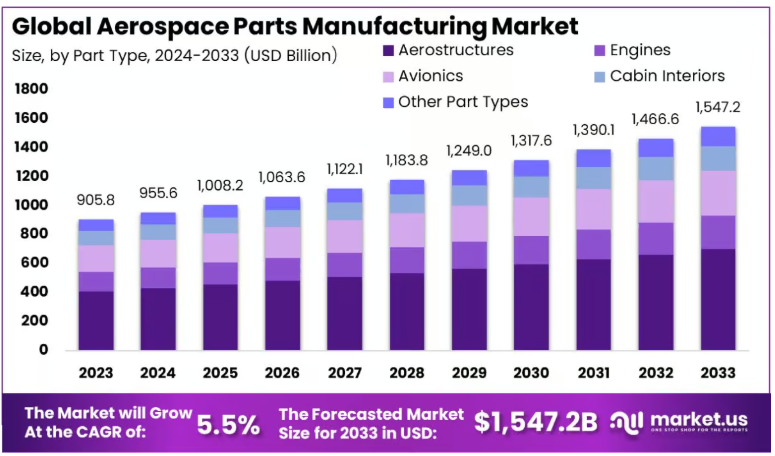

Why aerospace might be the most beautiful industry on earth. Not the romance of flight. The economics.

To sell one part for a jet engine you need decades of engineering heritage, regulatory certification, and a design-win onto a platform that flies for 30 years. Once you're specified in, you're almost impossible to remove. Re-certifying a rival costs more than it could ever save.

A part might cost a million dollars. The plane costs $100 million. Too cheap to switch. Too critical to risk.

That's not a free market. It's a fortress. And the whole market nearly doubles by 2033.

The fortress, the moat, and the rising tide. Tomorrow.

Thierry from arvy 🇨🇭@ThierryBorgeat

Roughly 90% of the world's aircraft carry a piece of it. You've never been able to own it directly. On Monday, that changes. Article coming tomorrw.

English

@sidecarcap Great. Think $TDG, $HEI and Henry Singleton should be studied as well

English

The Brian Jellison / Roper case study is the greatest I’ve ever read.

English

@RodriGo_ethe Market is trying to force $MSFT and $AMZN to pivot on data center capex

English

The market is screaming to the hyperscalers that their capex (at these levels) is lower ROI than their cost of capital.

You may trust the CEOs but I trust the market much much more.

English

@RihardJarc I respect the price action but I think a lot of bad news are priced in here

English

$MSFT, excluding its OpenAI stake, is trading at 17x forward P/E.

Investors are betting heavily that the CEOs of hyperscalers don't know what they are doing.

English

@F_Compounders With the right attitude, its easier than most people think. Permanent dollar cost averaging in equities with low (or no) leverage and let compounding magic kick in

English

@NicolaiTang1 @TheEconomist Best podcast. Sharp questions, great guests and right length

English

15 million views and listens!!! Who would have thought when we started this as a pilot four years ago. Recently @TheEconomist thought it was one of the best podcasts in the world. Here is to more great conversations ahead!

English

@moats_multiples @SouthernValue95 I believe that $MSFT's incumbency will hold, even in the AI era. Also, over the years $MSFT has shown more financial discipline than $GOOGL (and $META). It will pay dividends eventually

English

@filippogarba @SouthernValue95 His view was that Microsoft's core business franchises are more prone to AI disruption vs. Google which is likely to reinforce its competitive advantages because of it. Personally, I'm not convinced that Office gets it lunch eaten by the LLMs.

English

TCI's Chris Hohn on $GOOG and financial infrastructure ($V $MA $MCO $SPGI $DB1

"Within the technology sphere, TCI maintains positions in Google and SAP. Whilst they didn’t really discuss SAP, they seemed quite bullish on Google and its prospects in AI. Notably, they pointed out that unlike its peers, Google has a strong presence across every layer of the AI stack and that AI was a self-reinforcing competitive advantage in its other businesses e.g., AI has made the search business even better for users and customers. TCI project Google Cloud to grow at a 45% p.a. rate to 2030 and see it as one of the big winners in AI."

"There was quite a bit of discussion around businesses in what TCI labels financial markets infrastructure – Visa, S&P Global, Moody’s, Deutsche Borse. The common seam through these discussions was the standards/protocol nature of these businesses which makes them near impossible to disrupt. All the while, most of these companies seem to be trading at decades low valuations on the fear of AI disruption from the market. TCI’s conviction here was evidenced by the increased allocation of capital to these businesses which the firm hopes will generate a high-teens net IRR over the next five years."

moatsandmultiples.substack.com/p/inside-tcis-…

English

After observing capital deployment strategies for 15 yrs I have concluded that the best risk/reward is buying great businesses cannibalising their share count $HLT $ORLY. Second best: great businesses with bolt on M&A $TDG $HEI. Avoid transformational M&A at all cost $SPGI $BRO

English

@qualtrim The problem is when there is a disconnect between current price action (forward looking) and current earnings (lagging indicator). If earnings have risen but price has lagged, that could be indication of future earnings erosion. Hope its not the case with $MSFT as I am long

English

Lawrence uses $TDG to illustrate a broader framework for assessing which businesses are safe from AI and which are doomed.

His primary heuristic for AI disruption is: "Is the business selling something denominated in human time, while its cost of goods sold is denominated in compute tokens?"

TransDigm sells highly engineered, physical, proprietary aerospace components with extreme regulatory and safety moats. It does not sell "human time" or "information," so its core product and competitive advantage cannot be automated away. This makes it a highly durable asset in an AI-driven economy.

English