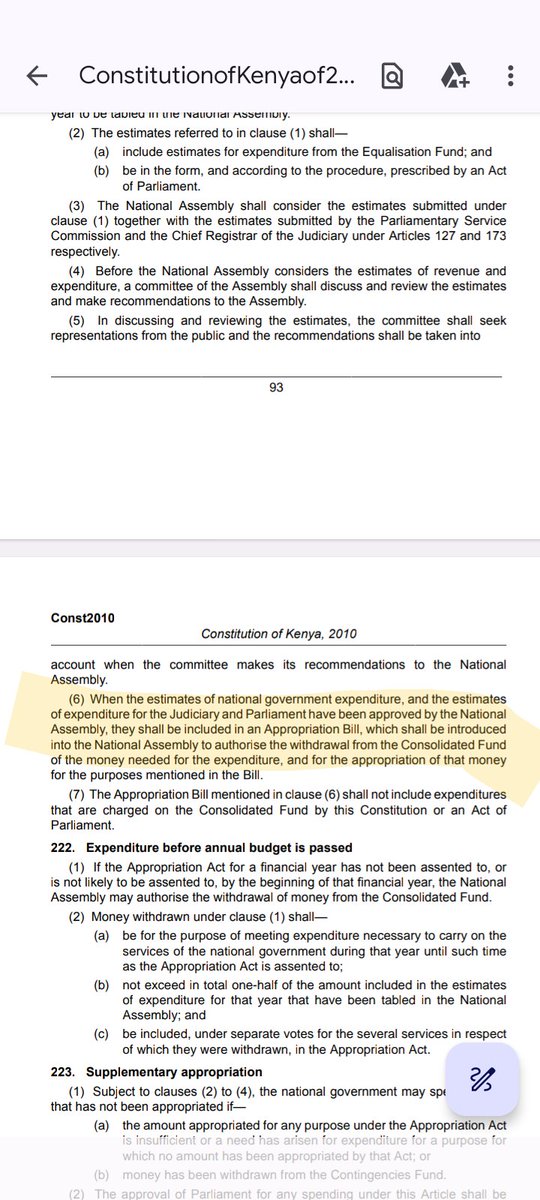

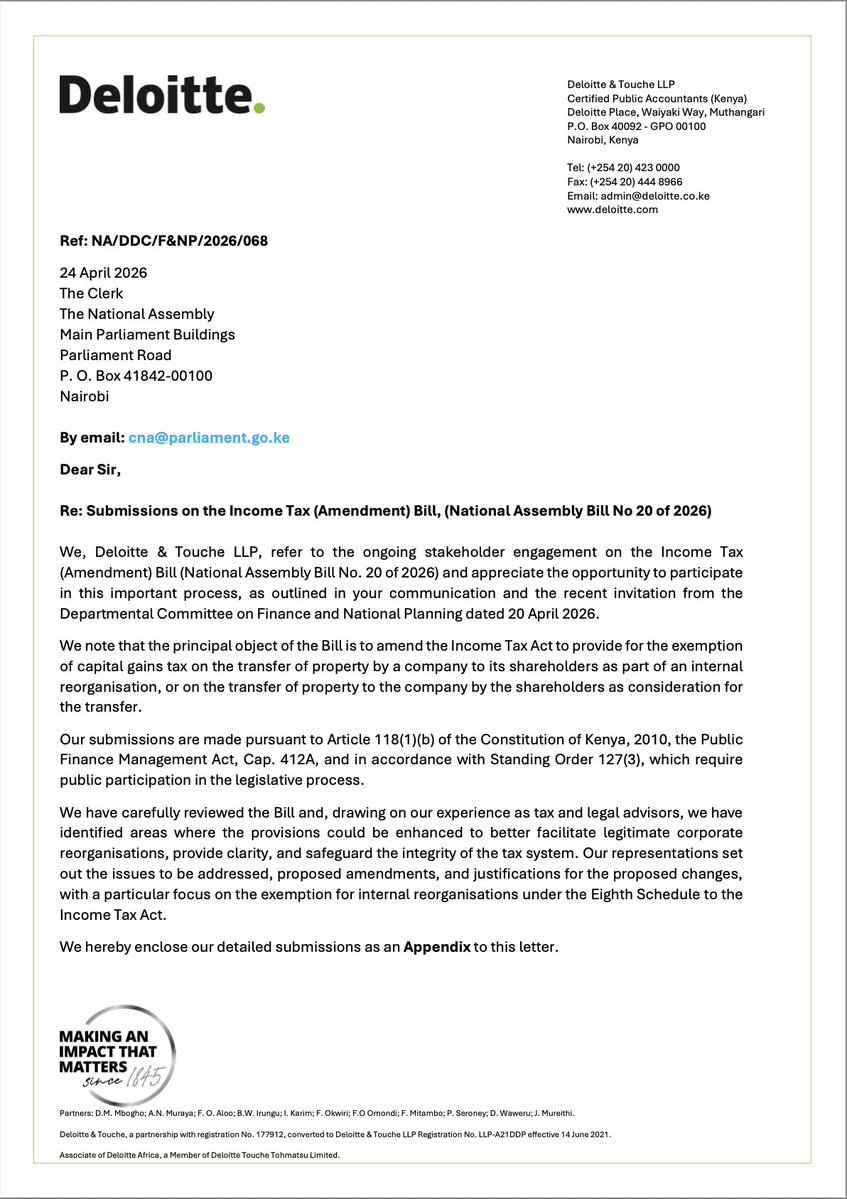

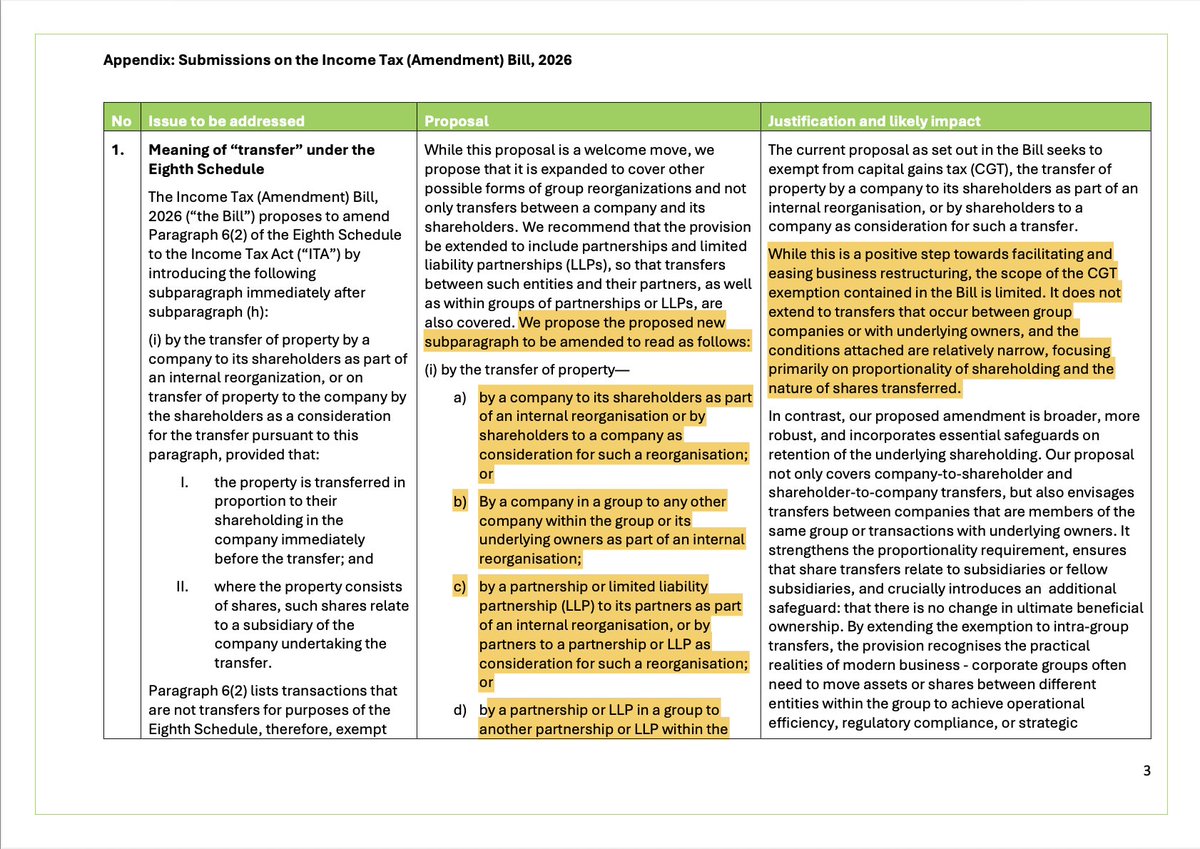

The Income Tax Act (Amendment) Bill 2026 is also out! The change is on Capital Gains Tax with regard to exemption of transfer of property in the case of internal reorganisation. I am struggling with this from an optics standpoint: 1. Remember Finance Act 2025 started this process by defining a "company". Now the Income Tax (Amendment) Bill 2026 effectively furthers this process. The clean up is warranted, it's the timing that doesn't make sense 2. Why couldn't this just wait for Finance Bill 2026? Finance Bill 2026 is just two weeks out anyway? What's the urgency? 3. Shouldn't this Bill have granted the PAYE relief for Kes 50k & below earners? Weren't we just told last week that there was no point in having an Income Tax Amendment Bill just before Finance Bill? Why is that provision missing in this Bill