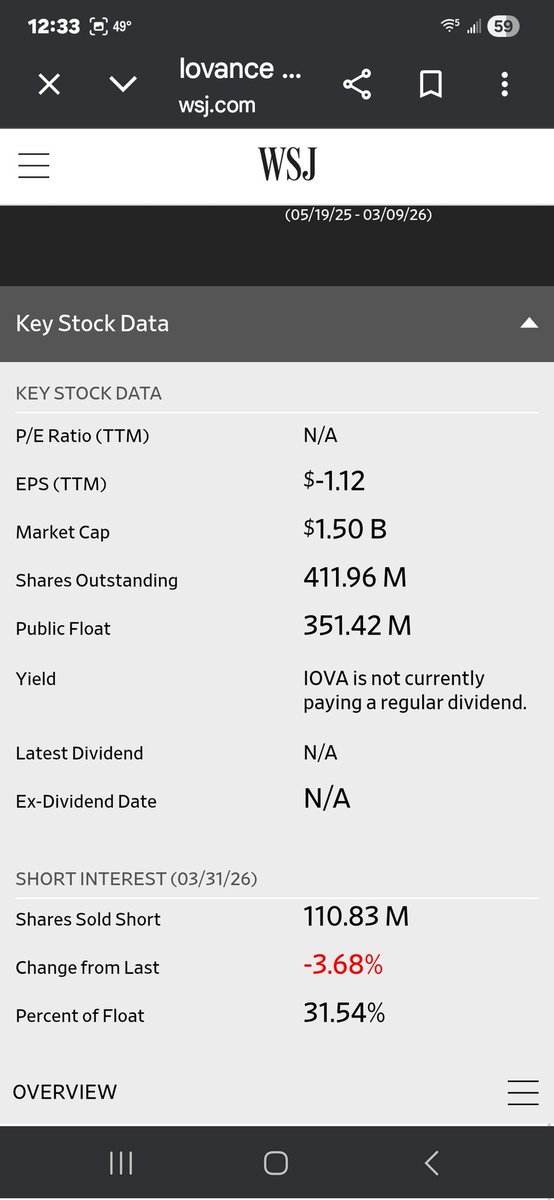

@Dancingtapas Right now the market cap is only sitting at roughly 5x last year's full year revenue That's ridiculous with Amtagvi ramping and 60%+ revenue growth last year New guidance in early May could easily deliver that 20-30% you mentioned especially if they give color on margin expansion

English