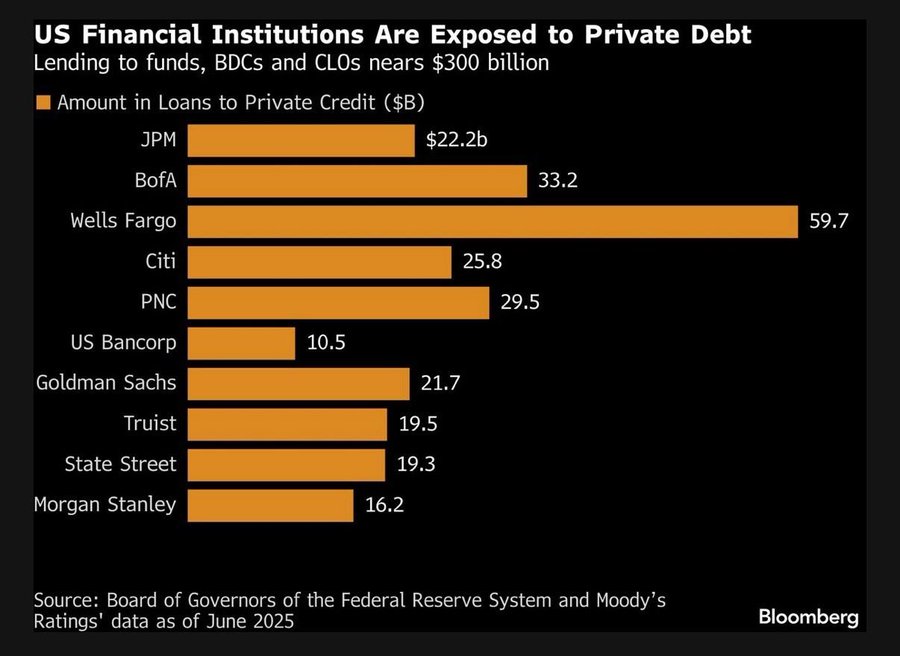

@OilHeadlineNews @tomkeene Also explain that their exposure is nearly all investment grade structures with massive subordination. They are not exposed directly to first dollar loss of the loans.

English

gregkero

3.6K posts

@gregkero

Father. Husband. Coach. Founder of A Street Investments. Private credit. Venture capital. Safety first. Tweets are not advice.

Araghchi reminds everyone that without Iranian oil exports the world is locked into high oil prices. Millions of barrels of oil also need a stable electric power supply to move. This is Trumps prisoner dilemma…he can’t blow #Iran up entirely w/out the global economy suffering. #OOTT

I feel their pain. 40% redemptions is beyond breaking point for a private credit firm. But gating your investors? In the long run, probably even worse. Private credit funds lend to middle-market companies (in Blue Owl's case, mostly software and SaaS). These are illiquid, multi-year term loans. They can't be sold overnight on an exchange. There is no bid. Now imagine 40% of your investors want out. You have two options: A) Honor the redemptions. To raise cash, you have to sell loans at a steep discount, or worse, call them in early. But your borrowers don't have the cash sitting around either. They took term debt because they needed time. Force-selling a multi-billion loan book at 70-80c on the $ doesn't just hurt your returning investors - it destroys value for everyone who stays. B) Gate redemptions. Which is exactly what Blue Owl did. Cap withdrawals at 5% per quarter. Protect the remaining LPs. Protect the borrowers. But now you've confirmed every investor's worst fear: your money is locked and you can't get it back when you need it. This is the fundamental tension in private credit: you're offering quarterly liquidity on assets that have none. It works beautifully in calm markets. In stress, the math breaks. And here's the part nobody talks about - the borrowers. If a fund were forced to liquidate, those SaaS companies with 3-5 year term loans would face early repayment demands, covenant pressure, or their debt getting transferred to a distressed buyer at punitive terms. The very companies the fund was supposed to support become collateral damage. Blue Owl is in survival mode, so they chose the second option. Which doesn't mean they won't have to go with option A as well, and very soon. But the real question for the industry: should interval fund structures be used for assets this illiquid in the first place?

FT exclusive: US treasury secretary Scott Bessent discussed tightening the US Treasury’s oversight of the Federal Reserve by adopting elements of the Bank of England’s model ft.trib.al/6dgGvkh