@CryptoPicsou À quel prix du Hype tu met ton plus beau Hypurr en PP

Français

Greg.hl

31.4K posts

Hypurrs getting swept as we speak

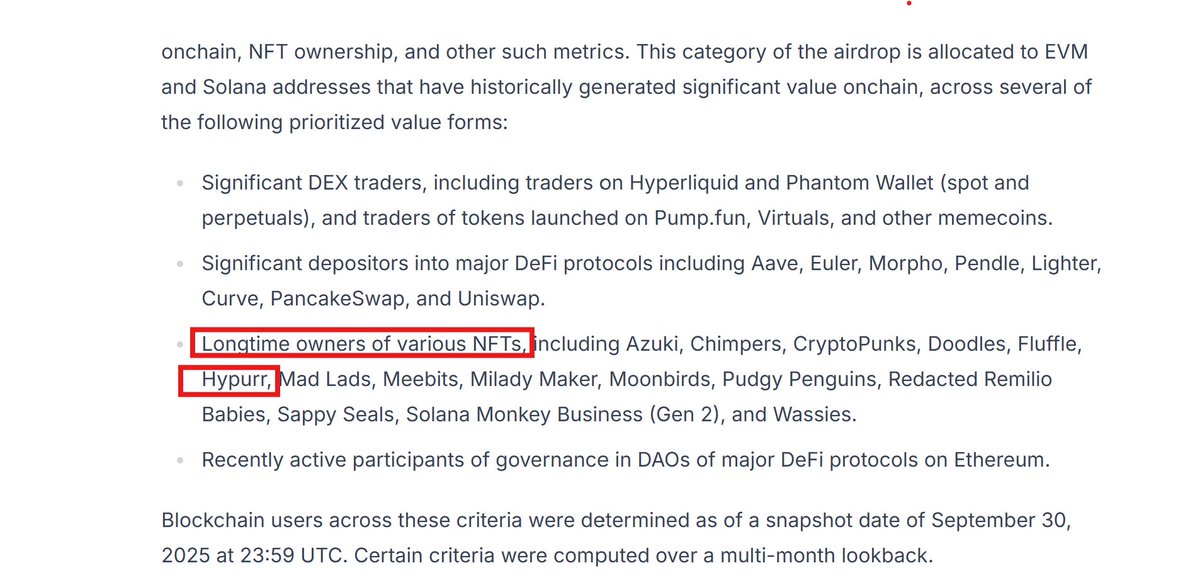

How I think about valuing @kinetiq_xyz $KNTQ relative to Lido and Jito Kinetiq is a dual-layer liquid staking protocol built on Hyperliquid. It has two main products: • kHYPE, the base liquid staking token (LST), currently yielding around 2.2% APY, with a 0.1% exit fee on unstaking and no fee on yield, meaning users keep 100% of rewards. • vkHYPE, a yield vault built on top of kHYPE, where users can earn 4–6% APY. The protocol takes a 20% performance fee on vault profits, which is the main revenue source for now. Benchmarking against Lido and Jito To find a fair range for KNTQ, I looked at the two leaders in liquid staking. Lido (LDO) • TVL: ~$31.85B (DeFiLlama) • APY: ~2.6–3% (Dune Analytics) • Annualized Fees (user yield): ~$1.08B (DeFiLlama) • Annualized Revenue (protocol): ~$108M (DeFiLlama) • Fee model: takes ~10% of validator rewards Its Market Cap sits around $775M, with a Fully Diluted Valuation (FDV) of $865M (CoinGecko). Jito (JITO) • TVL: ~$2.55B (DeFiLlama) • APY: ~6–8% (Jito Network) • Annualized Fees (user yield): ~$178M (DeFiLlama) • Annualized Revenue (protocol): ~$10-20M • Fee model: 4% fee on total yield (staking + MEV) Its Market Cap is approximately $410M, and its FDV around $1.05B (CoinGecko).Comparative valuation Here’s how the three protocols compare on a revenue and valuation basis: • Lido generates around $108M in annualized revenue and trades at a FDV of about $865M, implying roughly an 8× revenue multiple. • Jito earns between $10M and $20M per year, with a FDV of about $1.05B, which corresponds to a 50–100× revenue multiple given Solana’s growth dynamics and Jito’s MEV exposure. • Kinetiq, with an estimated $3–4M in annualized revenue, would trade between 15× and 35× at a $50–120M FDV range. This places Kinetiq squarely between Lido’s stable, mature profile and Jito’s high-growth positioning. The current range feels fair for a protocol that is still early but already has meaningful traction, clear differentiation in fee structure, and growing visibility within Hyperliquid. Kinetiq doesn’t yet monetize its full TVL like Lido or Jito, but its model is highly scalable. As more kHYPE holders move into vkHYPE or other yield layers, its revenues could expand faster than its TVL, improving operating leverage over time. Both Lido and Jito monetize their entire TVL base, while Kinetiq currently earns most of its revenue from its vault layer. Kinetiq’s current revenue profile • Total TVL: ~$1.65B (DeFiLlama) • Revenue-generating portion: ~$330M (vkHYPE vault, Kinetiq Docs) • Fee structure: – kHYPE: 0.1% exit fee only, no yield fee – vkHYPE: 20% performance fee on vault profits Assuming an average 5% yield on the vkHYPE vault, users earn roughly $16.5M annually, of which around $3.3M accrues to the protocol. That gives Kinetiq an estimated annualized revenue of $3–4M, which represents a strong take rate on the "active portion" of TVL. Comparative valuation Here’s how the three protocols compare on a revenue and valuation basis: • Lido generates around $108M in annualized revenue and trades at a FDV of about $865M, implying roughly an 8× revenue multiple. • Jito earns between $10M and $20M per year, with a FDV of about $1.05B, which corresponds to a 50–100× revenue multiple. • Kinetiq, with an estimated $3–4M in annualized revenue, would trade between 20× and 50× at a $70–175M FDV range. This places Kinetiq squarely between Lido’s stable, mature profile and Jito’s high-growth positioning. The current range feels fair for a protocol that is still early but already has meaningful traction, clear differentiation in fee structure, and growing visibility within Hyperliquid. Kinetiq doesn’t yet monetize its full TVL like Lido or Jito, but its model is highly scalable. As more kHYPE holders move into vkHYPE or other yield layers, its revenues could expand faster than its TVL, improving operating leverage over time. Why there could be upside The current valuation does not yet reflect Kinetiq Launch, an upcoming product designed to connect staked HYPE holders with entities deploying HIP-3s. Launch will enable those entities to borrow staked liquidity and share a portion of their revenue with Kinetiq users, creating an additional revenue stream and expanding the percentage of TVL that produces fees. Beyond Launch, the team plans to introduce more yield-generating and staking-related products, which will diversify and strengthen the protocol’s overall monetization base. Given the growing momentum around the Hyperliquid ecosystem, these factors could justify a valuation premium once they go live. Another key variable is the price of HYPE itself. Since Kinetiq’s revenue is directly linked to the notional value of staked HYPE, any price appreciation over the next 6–12 months would automatically increase both the protocol’s fee income and its nominal earnings base. Markets tend to anticipate that type of linkage, so $KNTQ ’s valuation could start reflecting higher expected revenues ahead of time if sentiment around Hyperliquid and HYPE strengthens. For that reason, I think $KNTQ could reasonably trade at launch within a $100–250M FDV range. That would imply a token price between $0.10 and $0.25 ( maximum supply of 1,000,000,000 KNTQ). KNTQ Airdrop for Users (Based on $100–250M FDV Range) • Genesis (25.0%) → valued between $25M and $62.5M • Hypurr Holders (1.0%) → valued between $1M and $2.5M Hypurr allocation is directed to holders of the 4,600 Hypurr NFTs, representing the earliest supporters of the Hyperliquid ecosystem. Given that 1.0% of the supply equals 10,000,000 KNTQ tokens, the estimated value per Hypurr NFT would be: At $100M FDV ($0.10/token): ~$217 per NFT At $250M FDV ($0.25/token): ~$543 per NFT Final Thoughts Some of the recent predictions I’ve seen feel a bit stretched when compared to the actual metrics of leading liquid staking protocols like Lido and Jito. This doesn’t make me bearish on Kinetiq; the fundamentals and timing still look strong. It just seems more prudent to keep expectations grounded in realistic comparables and proven revenue models rather than market hype. Valuations that reflect fundamentals tend to hold up better once the initial excitement fades. Wdyt? Hyperliquid.

I guess I’m neither a Hypurr holder nor a Hyperliquid trader. Hyperliquid.