Hasquet retweetledi

Red Robin is a case study in how to kill a restaurant chain from the inside out.

In 2015, the stock hit $92.90 per share. Revenue peaked in 2017 at $1.4 billion across 573 locations. Families loved the place. Bottomless fries. Birthday parties. “Gourmet” burgers when that word still meant something in casual dining. The brand had real equity.

Then management panicked about rising minimum wages and made the single worst decision in the company’s history: they fired all the bussers.

January 2018. CEO Steve Carley cut bussers across every location, eliminated expeditors, and replaced kitchen managers with generic “back-of-house” roles. The logic was pure spreadsheet thinking. Labor costs were rising, so remove labor. The savings looked great in quarterly earnings. The second and third order effects were catastrophic.

Tables stopped getting cleared. Wait times ballooned. Walkaways increased 85% year over year. 75% of the dine-in traffic loss came during peak hours, the exact window when the restaurant makes money. Ticket times out of the kitchen jumped a full minute on average. Customers who waited 20 minutes for a table and another 20 for a burger stopped coming back. Red Robin’s own CEO at the time, Denny Marie Post, admitted the damage was self-inflicted.

And here’s the compounding problem. While Red Robin was gutting its own service model, it simultaneously launched a “Tavern Double” value menu at $6.99 to drive traffic. Orders of the cheap burgers jumped from 9% to 15% of all orders, which cratered the average check. So Red Robin was now serving worse food, slower, in a dirtier restaurant, at a lower price point. That combination is how you enter a death spiral.

Meanwhile, 16% of locations were in malls. Mall traffic was already declining. Those locations saw 5.5% sales drops versus 3% at standalone stores, dragging the whole system down. Management acknowledged the problem quarter after quarter and did nothing about it for years.

Five CEOs in 10 years. Think about that. The one leader who provided stability, Michael Snyder, was with the chain from 1979 to 2005. After that, it was a revolving door. Every new CEO launched a new turnaround plan. Every plan was abandoned by the next CEO. The North Star plan. The First Choice plan. New menu rollouts. Loyalty program reboots. None of it addressed the core issue: they’d trained an entire generation of customers to think of Red Robin as the place where the service is terrible.

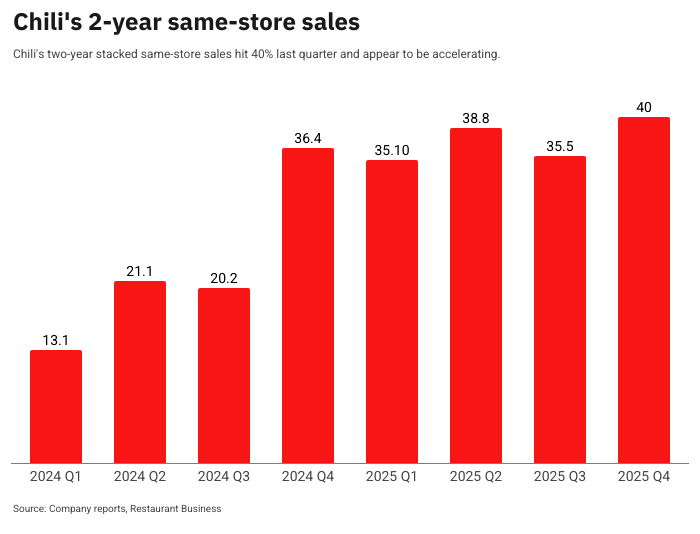

The contrast with Chili’s makes the failure even clearer. Kevin Hochman took over Chili’s in 2022 and did the opposite of what Red Robin did. He simplified the menu, invested in operations, launched a $10.99 “3 for Me” deal that went viral on TikTok, and let the food speak for itself. Chili’s just posted 31% same-store sales growth. Red Robin’s comparable revenue was down 1.2% for all of 2024.

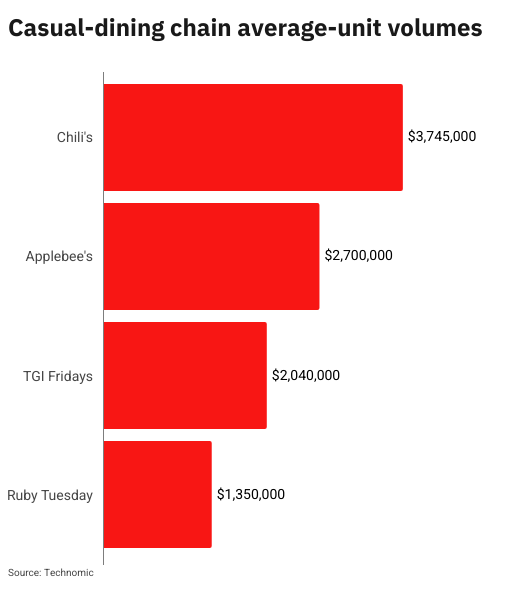

Both chains were in roughly the same position three years ago. One chain invested in the customer experience. The other spent a decade cutting it. Red Robin’s $65M market cap and Chili’s $3.3B market cap tell you which approach works.

The stock went from $92 to $3.61. That’s what happens when you optimize for the quarterly earnings call instead of the customer walking through the door.

Triple Net Investor@TripleNetInvest

Red Robin has lost ~90% of its value over the last 5 years You can now buy the ENTIRE company for just ~$60 million They used to be one of the most beloved spots for kids, teens, and families... Where did it go wrong for them and can they turn it around?

English