HBrsn retweetledi

The photonics thesis is predicated on a multi-year cycle.

My play? Focus on two concentrated trades that account for both short and long term technology shifts so I can gobble up the asymmetry today and tommorow.

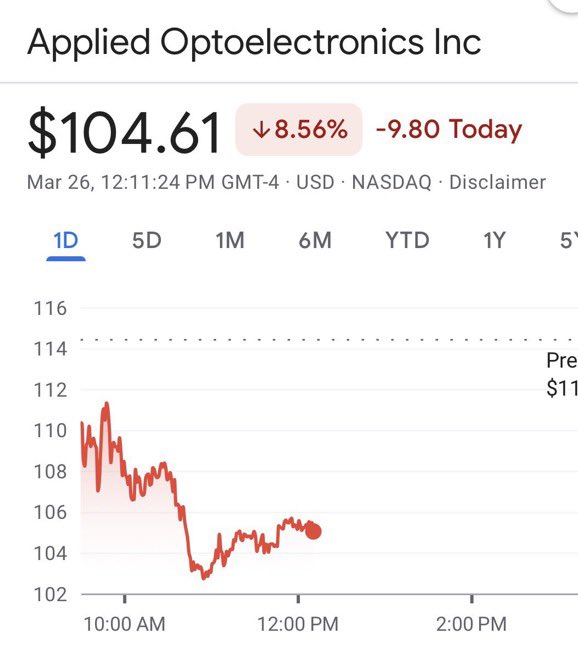

The first, $AAOI, is my near-term explosive set up based on extreme hyperscaler demand for LPO transceivers to solve the copper wall now.

Management is guiding to a $5B run rate as soon as early 2027, up from ~$500M in 2025. MC ~8B pales compared to the outlook. Vertical integration with their own domestic laser fabs makes it unique.

I know the demand is there. This is not a sleep at the wheel trade. It means watching management like a hawk to see if they can meet the moment.

The second, $SOI / $SLOIF, is a trade on the back half of the cycle, when CPO takes over because transceivers are imperfect solution. A pluggable transceiver or LPO uses approximately 50 square millimeters of Photonics-SOI per chip. A CPO switch package uses approximately 200 square millimeters.

This business is cheap at 3.6x EV/revenue because it will take time to bounce off the mobile chip trough and let photonics point the way once CPO production ramps in 2027.

Morgan Stanley sees this doubling their PT yesterday to 70 euros, considerable upside on 54 euros currently.

"The mobile market remains weak, but growing confidence in Photonics SOI is shifting the medium-term outlook".

Soiboy and AA-O-my-god.

English