Sabitlenmiş Tweet

don’t let romance get in the way of achievement and don’t let achievement get in the way of romance

English

heisdreamingnow 🔮

2.6K posts

@heisdreamingnow

hmm… something went wrong, try again

81% of recruiters said their employer posts ‘ghost jobs,’ per Fortune.

Dad what were you like in the 90’s? Nevermind

Here it comes… Ro Khanna + Bernie Sanders are proposing a *national* wealth tax on billionaires. Going even further than California, they want this 5% unrealized wealth tax to be annual.

Epstein philosopher: "The banana sitting on your counter top is it alive or dead? It's alive"

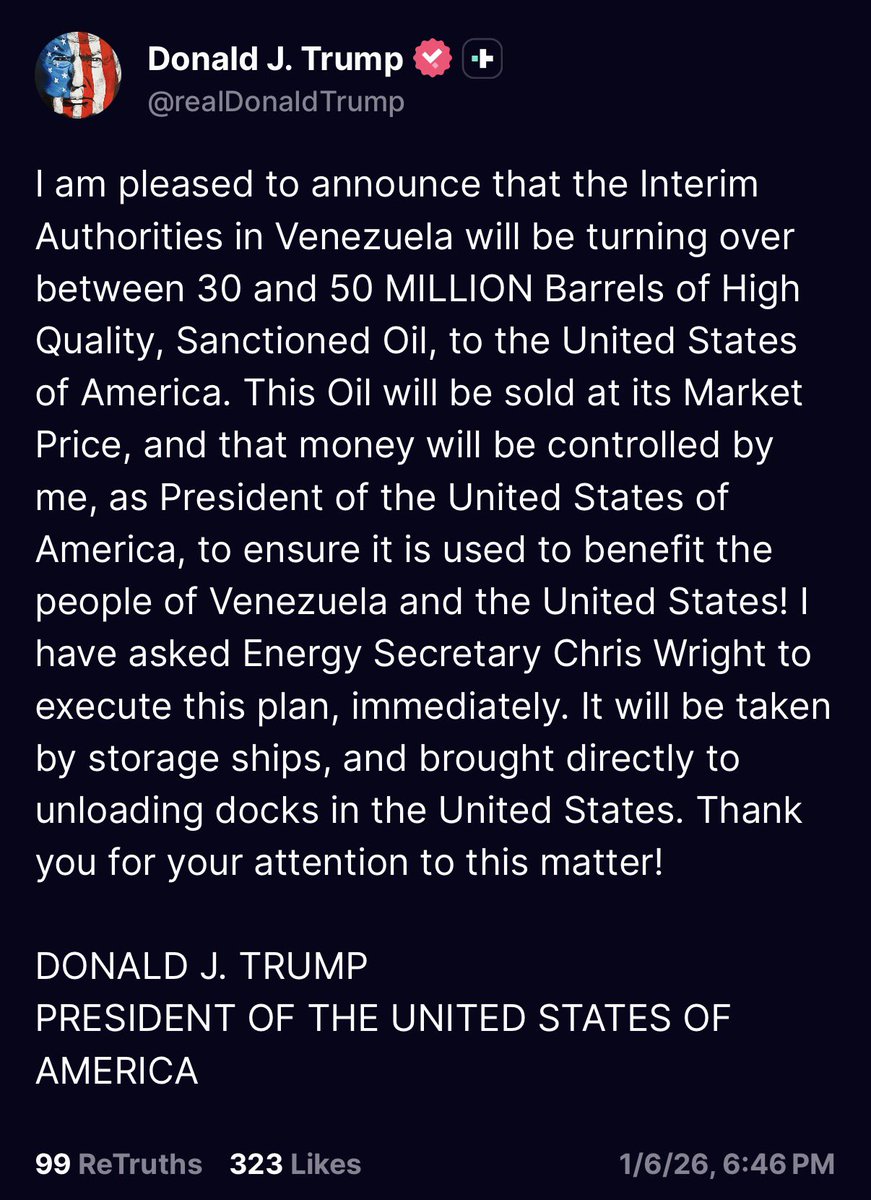

🚨 BREAKING