idan t

523 posts

They're all different parts of the supply chains. $AXTI makes the materials needed for anything to do with photonics. I still have my AXT positions.

Packaging layer players might be impacted given nuances of hyperscaler vertical integration.

But selling off any laser or upstream player doesn't make much sense and it's a good buying opportunity for some.

English

I've always maintained $POET can get designed out and likely would in a few years for $MRVL.

Especially as hyperscalers tend to vertically integrate upstream, I just didn't expect it so soon.

For me to be bullish, $POET would have needed to multi-source to multiple hyperscaler supply chains rather than just Marvell.

However, this goes this show:

There's a reason why all the Laser companies are worth tens of billions.

Laser design and fab is much more difficult than companies like $POET buying the lasers to package them.

If $MRVL were completely reliant on $POET, they wouldn't break off the engagement despite the NDA, so it does feel like an excuse. Poet was just the fastest time to market given it's already designed into Celestial, but serves more as a Gen-1 bridge.

Regardless all the hyperscalers require a light source (which is much much more difficult to vertically integrate):

And after $NVDA went and bought out allocation for $LITE, $COHR...

There's not many laser suppliers left aside from $SIVE.

There's a lot of nuances markets might miss, but packaging layers are different than laser layers.

It's highly likely now $MRVL just buys lasers directly from Sivers (which is even more bullish) given they already match Celestial specifications.

And also highly likely Marvell multi-sources with $MTSI and $LITE (if there's any capacity left).

English

$AXTI #money #stockmarket

Wow!!! 50 million dollar investment in AXTI!!!! Earning on Thursday !!

English

idan t retweetledi

This is what happens when you find a true monopoly.

Did you listen anon?

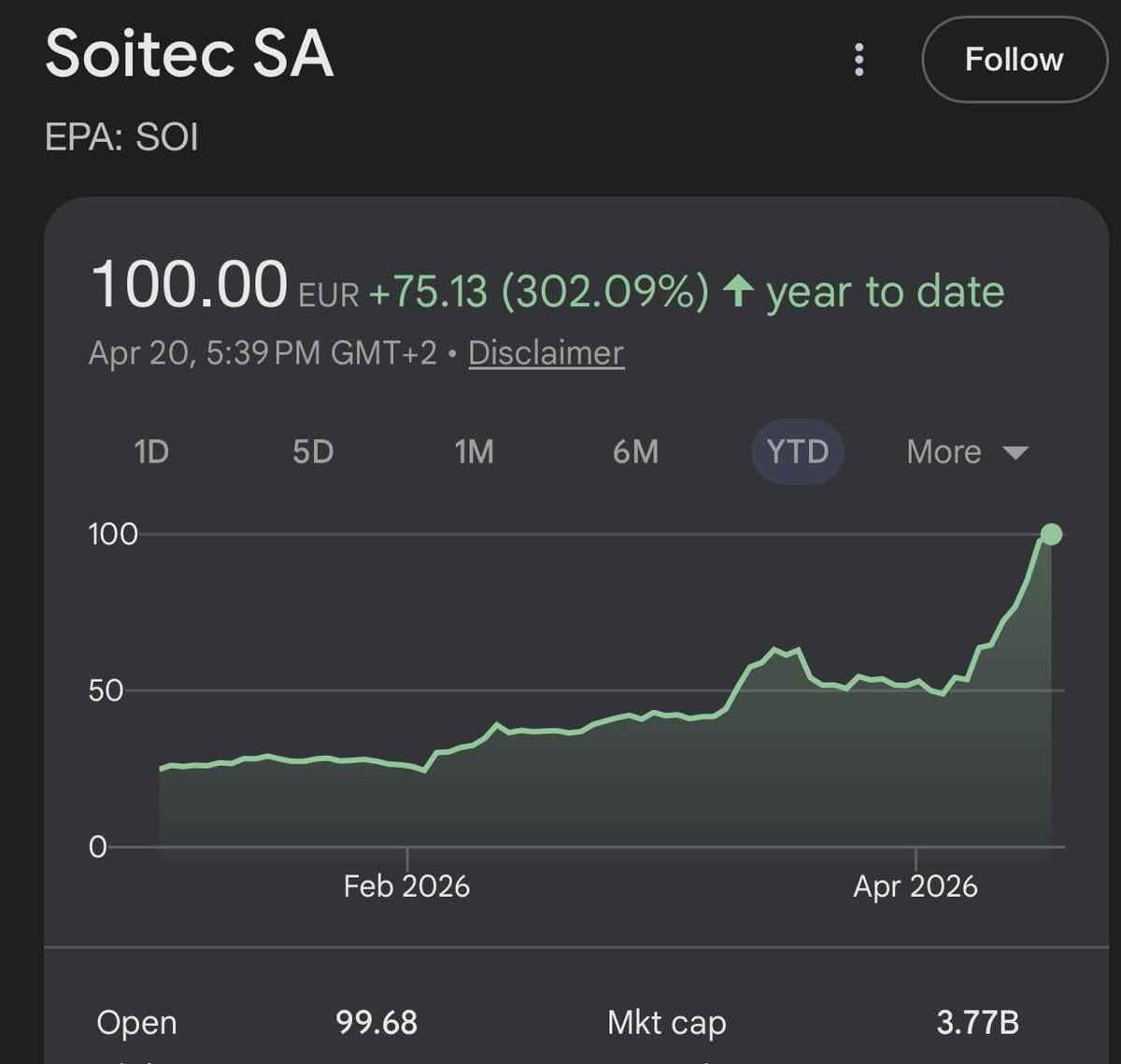

$SOI up +140% since my thesis 1M ago and +302% YTD.

Just a friendly reminder:

“Soitec’s Photonics-SOI products are deployed in 100% of next-generation AI data centers.” - EVP Soitec

Serenity@aleabitoreddit

Changed my mind about Soitec ( $SLOIF ) and took a sizable position ~43 for CPO exposure. $NVDA GTC next week biggest catalyst pushing photonics and this architecture. ~1.5B euros MC. Trading at 1x book value and ~2x P/S (very depressed valuations) Genuine monopoly over substrates side for CPO (typically very premium valuations for photonics + even extra premium for monopoly status) Algos and analysts might get confused over market share but it’s an actual monopoly over SOI substrates since they give licenses to other players like Shin Etsu for diversification sake eg. $TSM doesn’t like just 1. I don’t think institutions will wait until next year to frontrun these names like Soitec or $TSEM (and most probably haven’t even heard of these names like $AXTI yet) This timing would be buying the likely bottom of the depressed smartphone cycle, while getting full upside of CPO mid-late 2027 + $NVDA GTC catalyst next week. I personally think it’s a 3x from here so I went long.

English

קרן שמשקיעה ב-Anthropic וב-OpenAI הפכה לציבורית, והמשקיעים לא רואים בעיניים...

בחמשת הימים האחרונים אנחנו עדים לשיגעון לא רק במלחמה מול איראן, אלא גם בבורסה בניו-יורק, וספציפית עם קרן אחת, שהייתה לא מזמן די אנונימית בשם The Fundrise Innovation Fund, ונסחרת תחת הסימול $VCX. 👇

עברית

KEY FIB LEVELS FOR POPULAR GROWTH STOCKS

Space

• $RKLB -- $67

• $ASTS -- $87

• $PL -- $24

• $BKSY -- $23

Photonics

• $AAOI -- $83

• $LITE -- $504

• $COHR -- $203

• $CIEN -- $278

Drones

• $ONDS -- $10

• $UMAC -- $12

• $AVAV -- $223

• $KTOS -- $75

Nuclear

• $OKLO -- $50

• $UUUU -- $13

• $GEV -- $649

• $LEU -- $168

AI Utility

• $IREN -- $33

• $NBIS -- $94

• $CIFR -- $11

• $CRWV -- $69

AI Inference

• $NET -- $195

• $DOCN -- $63

• $FSLY -- $19

• $OSS -- $8

AI Power

• $VST -- $140

• $BE -- $118

• $CEG -- $257

• $VRT -- $192

AI Hardware

• $NVDA -- $164

• $TSM -- $292

• $ASML -- $1,177

• $AMD -- $194

AI Applications

• $PLTR -- $120

• $SNOW -- $155

• $MDB -- $238

• $ZETA -- $16

Physical AI

• $TSLA -- $323

• $AMZN -- $199

• $GOOGL -- $269

• $ISRG -- $466

AI Security

• $MSFT -- $381

• $CRWD -- $401

• $PANW -- $161

• $RBRK -- $46

English

I just realized…

Am I the most subscribed to finance account on X right now?

Kinda surreal so many funds and companies started reaching out for requests recently.

That aside; not planning on changing anything when I was 300 followers and now 100k+.

Just having fun sharing my thoughts with everyone.

English

@aleabitoreddit How much my bank account love you from 1 til 10? 💸💴1000

English

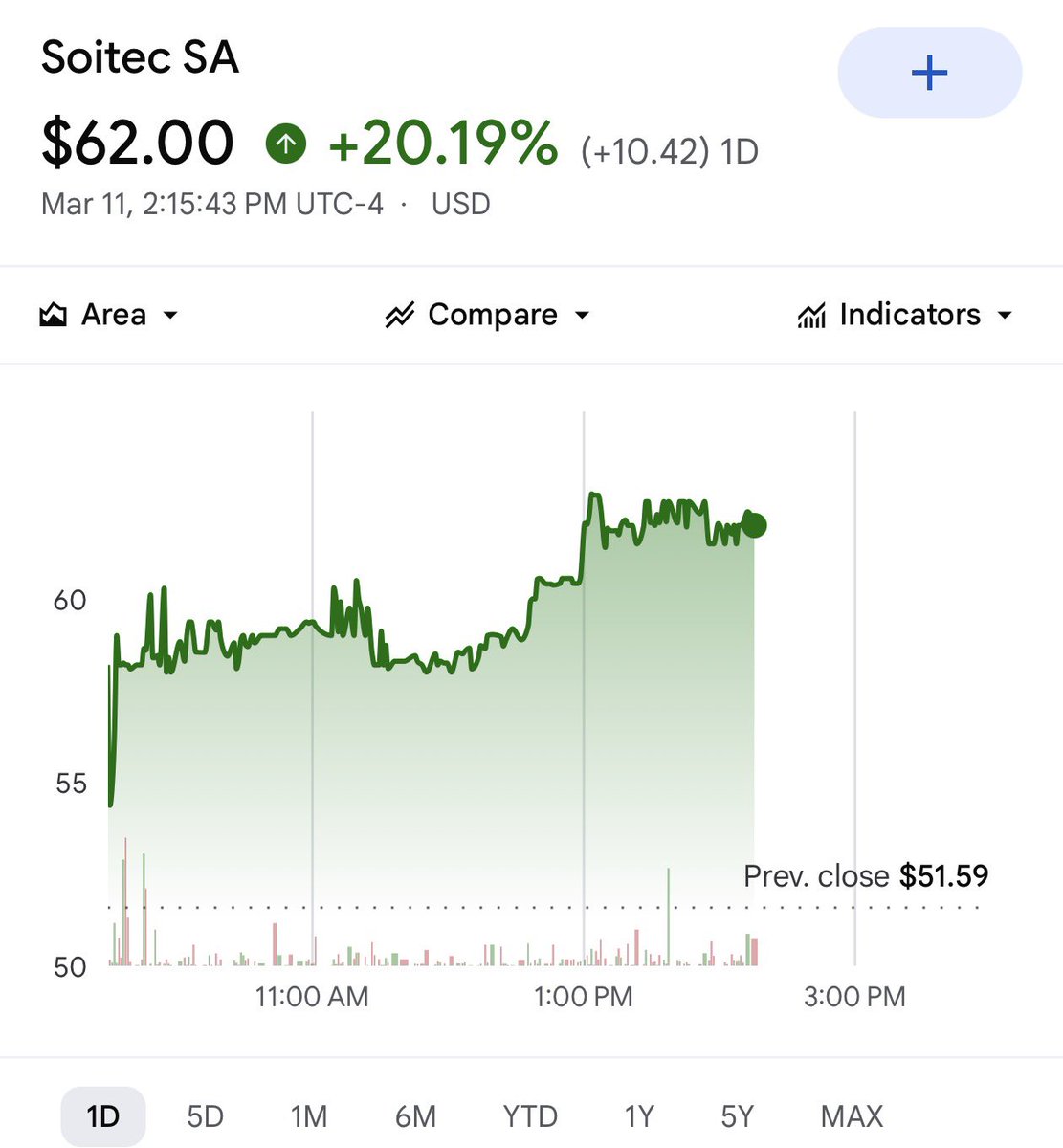

$SIVE <> $SIVEF is now up 165% this week.

Valuation? ~$300M MC.

However; either I’m dumb or Sivers is one of the best opportunities in photonics today.

You get the laser supplier for Jabil, Ayar, Poet ( $MRVL Celestial ), O-Net, and others:

That end up in $GOOGL, $MSFT, $AMZN, $META AI datacenters.

At ~$300M.

The EML laser suppliers today from $LITE to $COHR for reference are $45B+

This is one of the most undiscovered yet critical bottlenecks for future upstream photonics supply chains.

That markets have only starting to price in today.

Serenity@aleabitoreddit

I’m long $SIVE at $140M. I believe this is the next $LITE that markets and institutions missed. $SIVE makes InP CW DFB lasers. Closest comparison is $LITE in the current EML laser bottleneck. But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles. They supply the lasers to $POET Starlight, Ayar SuperNova. And others for the future CPO/silicon photonics architectures spearheaded by $NVDA. Current valuations make 0 sense to me personally. $POET is advanced packaging for $SIVE type lasers… But $POET commands worth 11x+ more than the company making the laser itself? It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B. So now at $130m: - - You have a likely mini $LITE like laser supplier to Marvell Celestial + hyperscalers through $POET. - Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI. And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential. On top, for revenue, they expected $453M "pipeline next few years”. And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers." Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come. I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt. It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week. Best of all, this is their pure play inp laser segment for silicon/photonics + cpo. Their Lidar segment is ramping up and they have $53-138M projected revenue coming in. Downside risk: - execution (as always) - dilution to scale up capacity to compete with $LITE and others. - $LITE, $COHR competition on scale after $NVDA just gave them $4B - CPO ramp gets delayed. I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B+ MC. Or how $POET, is worth ~9-10x more than its laser supplier. When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M. I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck). But I do think it will get a lot of institutional attention as Celestial and Ayar scale up. Especially if $POET and $SIVE gets qualified with other customers. If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures. Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated. Just as how $LITE did today going from $16 -> $622. This is just my personal thesis I'm sharing, DYOR/NFI. TLDR: InP Lasers are the current bottleneck in photonics as seen with $LITE valuations. $SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp. I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst). The upside here just way too compelling for me personally as the next possible $LITE.

English

@aleabitoreddit I love youuuuu haha!!!

With you on every stock $AXTI $AAOI !!! And of course $CRCL ❤️❤️🥷🏿🥊

English

$CRCL is now up 148.15% in 1 month.

If people are wondering why my YTD is ~500%?

It’s because I look at fundamentals, not scribbles on a chart.

The comment section back here aged like 2021 monkey JPEG prices.

Serenity@aleabitoreddit

I really, really like $CRCL at $54. Valuation has been completely reset back to $12B MC. Everyone was rushing to buy it back at $150-200 but at $54, it's a ghost town. USDC supply still $70B+ and I expect stablecoins to continue growing in usage.

English

@aleabitoreddit I’m with you my man! I will hold it for the rest of the year…!!

English

@aleabitoreddit Wondering if to take some money out and put it on SOI….i love those stocks ..

English

How does a random person posting their thoughts on a multi billion dollar company $SOI …

Send it up 20%

Am I that powerful now?

Serenity@aleabitoreddit

Changed my mind about Soitec ( $SLOIF ) and took a sizable position ~43 for CPO exposure. $NVDA GTC next week biggest catalyst pushing photonics and this architecture. ~1.5B euros MC. Trading at 1x book value and ~2x P/S (very depressed valuations) Genuine monopoly over substrates side for CPO (typically very premium valuations for photonics + even extra premium for monopoly status) Algos and analysts might get confused over market share but it’s an actual monopoly over SOI substrates since they give licenses to other players like Shin Etsu for diversification sake eg. $TSM doesn’t like just 1. I don’t think institutions will wait until next year to frontrun these names like Soitec or $TSEM (and most probably haven’t even heard of these names like $AXTI yet) This timing would be buying the likely bottom of the depressed smartphone cycle, while getting full upside of CPO mid-late 2027 + $NVDA GTC catalyst next week. I personally think it’s a 3x from here so I went long.

English

אני עובר ומתקן נתונים 😂

ישראל לא מבעירה בארות נפט. עדיין לא.

היא פוגעת במאגרי דלק.

למאגרי דלק (זוכרים חומר מזוקק מאתמול?) אין כל השפעה על השוק הגלובלי, רק המקומי.

יש לאיראן סדר גודל של 4000 בארות נפט.

ברגע שהורמוז סגור, לא משנה מה נעשה מכאן- הנזק הגלובלי כבר נעשה (ע״י האיראנים)

אילן שילוח@IlanShiloah

״להבות הנפט״. ישראל מבעירה בארות הנפט של איראן ותסומן זו שהבעירה בארות הנפט, מחירי הנפט, נגד סין, הצרכנים האמריקאים . למה לא לתת לאיראנים להבעיר בעצמם? טסטוסטרון עודף. היבריס.

עברית