DEUS X

680 posts

Investing narratives now the war is over:

1. the obvious space narrative still running

2. health sector ~ looking at UNH lead

3. defence sector is a fade for me ( will go up, but lesser )

My calls for narratives are usually quite spot on for those that follow me all these years. The problem is the vehicle I choose to ride the narrative. So don't fade my calls on narratives, but do your own diligence on what you'll use to ride it.

English

NVIDIA just dropped benchmarks showing 4-bit inference loses less than 1 point vs BF16 on most tasks.

It's not accuracy per request that you should be measuring. It's tasks completed per dollar. And at that metric, 4-bit wins by a landslide.

Read the full blog 👇

Fleek@fleek

English

@howardlindzon @Polymarket seems like I am not the only guy not knowing how to fix my bike

English

Lost a finger last night. the good emergency room at SDSU worked hard to save it.

I guess all that’s left is a @polymarket to

bet on if the finger can be saved

English

DEUS X retweetledi

DEUS X retweetledi

ATTENTION: NEAR20, an Agentic Yield-Bearing Token has just launched via @margfinance

"The launch of NEAR20 represents a significant milestone in bringing institutional-quality yield products to the NEAR ecosystem" - Philipp Suarez, Head of Finance at NEAR Foundation

Margarita Finance@margfinance

Most crypto treasuries are basically sitting on "dead" capital. Billions in ecosystem tokens stay static because the tools to put them to work safely—without crashing the price—just didn't exist. Until today. We just launched NEAR20 on @rhea_finance . 🧵 By leveraging Margarita Finance’s autonomous protocol, $NEAR holders can now earn permissionless yield via institutional-grade option strategies. The fact? We went from concept to live deployment in weeks, not months. No new infra. Just plug-and-play utility. 🍸 Working with the @NEARFoundation team to turn "static" tokens into "active" capital is exactly why we built this. The era of passive DeFi is over. The Agentic era is live. Check it out: rhea.finance

English

Morning thoughts on 2026 just posted for X subs.

I think this is going to be the story for the next year.

#WhatTheDataIsSaying

English

DEUS X retweetledi

Recording with @RaoulGMI on Thursday, should be a good chat

English

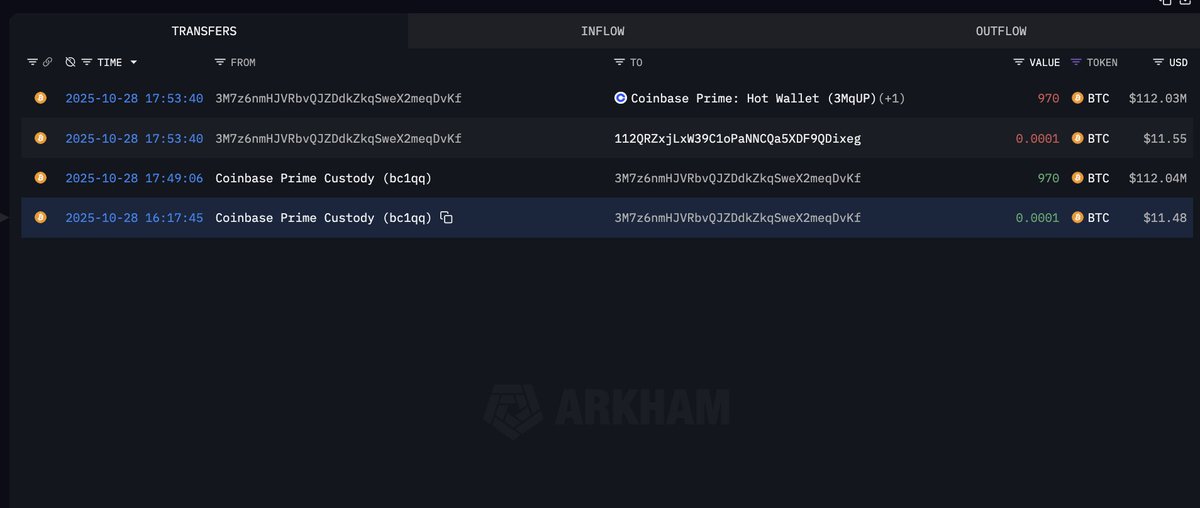

Update: They sent the 970 $BTC ($110M) to Coinbase Prime.

This is Sequan's first sale since they acquired the Bitcoin Treasury Strategy

Emmett Gallic@emmettgallic

Sequans, a Bitcoin Treasury Company, with over 3200 Bitcoins moved 970 BTC. The address they sent to then tested an unused address that looks like it will be a Coinbase Deposit. I'll update as it plays out, but this would be their first sale of Bitcoin since they launched.

English

Crypto majors trade at the following levels

BTC 113,840 (down 1.6% in 24 hours)

ETH 4,090 (down 3.4%)

XRP 2.618 (down 1%)

SOL 119.20 (down 2.6%)

Have a great day!

English