J ENZ

83 posts

Chill out

Norveçli@norveclifinance

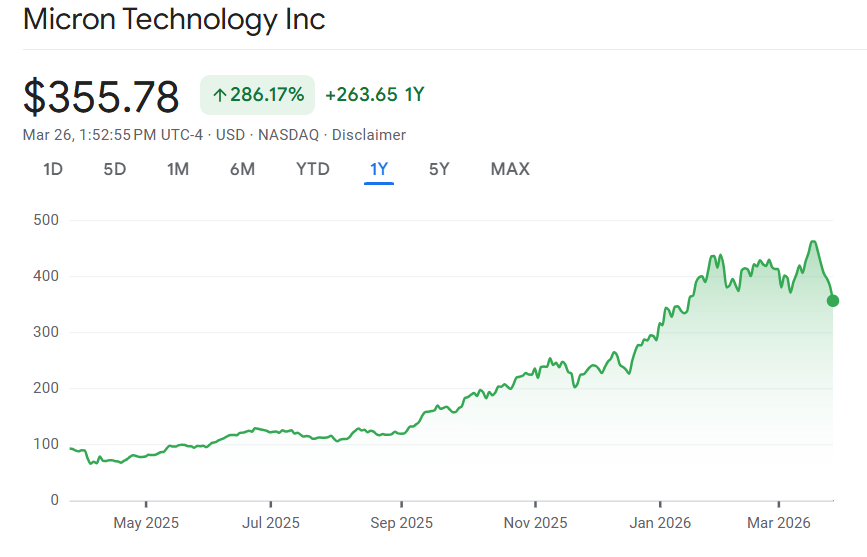

Dear Micron Management, Enough is enough. Micron’s stock is being openly pressured by short sellers who are spreading FUD and using aggressive short selling to distort the price. False, ridiculous, and misleading narratives are being pushed into the market while management remains too quiet. This is hurting shareholder confidence and damaging the company’s market value. Micron is not a weak company. Micron is a critical pillar of the AI, data center, and memory ecosystem. The fundamentals are strong. The long-term outlook is strong. The company’s strategic importance is obvious. Yet the market is being flooded with noise, and that noise is being used to pressure the stock unfairly. Now is the time to act. Micron management should immediately: 1.Publicly reject and correct false narratives. 2.Defend the company’s real business strength with stronger and more direct communication. 3.Accelerate share repurchases at these unjustifiably depressed levels. 4.Show the market that management will not sit back while short sellers and fear-driven misinformation attack shareholder value. Shareholders should not be left to fight this battle alone. The silence is no longer helping. It is encouraging the wrong actors. Please respond clearly, forcefully, and without delay. @MicronTech @MicronCEO $mu

English

@wealthmatica Just a reminder that institutions are forced buyers/algorithmic and are not explicit signs of conviction. Love seeing the CEO as a top shareholder however.

English

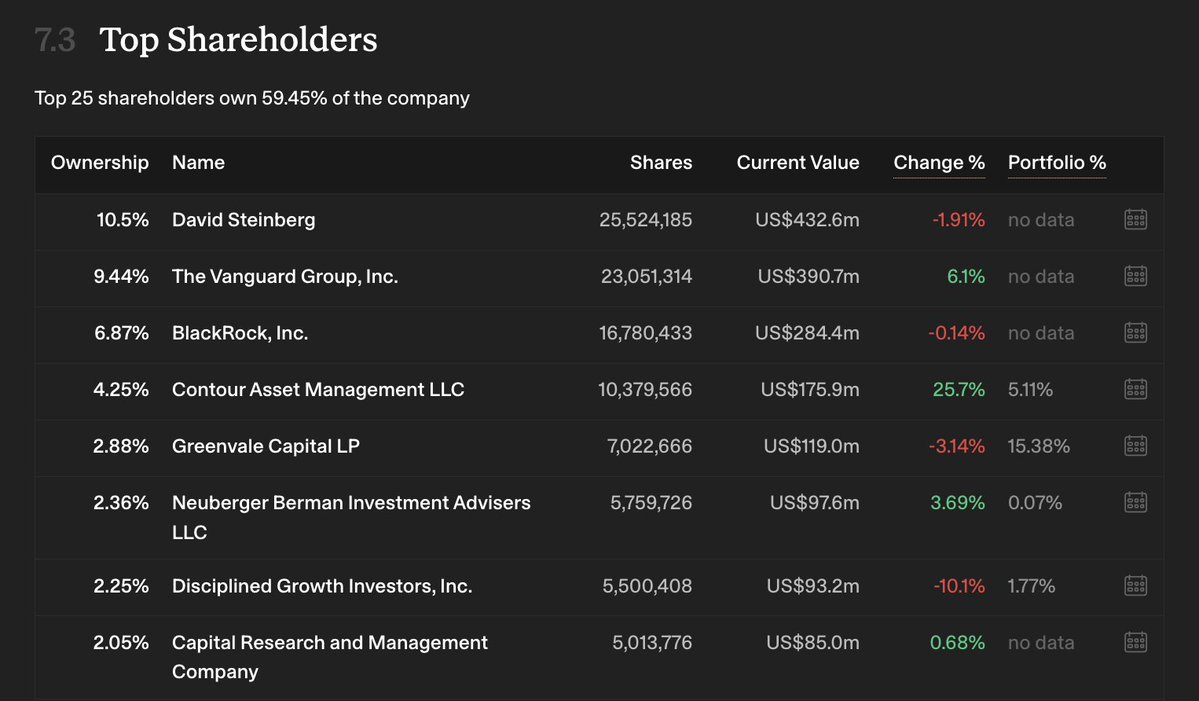

These are the top 8 shareholders of $ZETA Global.

1. David Steinberg, CEO/Founder

2. Vangard

3. BlackRock

4. Contour Asset Management

5. Greenvale Capital

6. Neuberger Berman Investments

7. Disciplined Growth Investors

8. Capital Research & Management Company

English

@FIREDUpWealth This is unironically how a lot of retail investors think. A true prolonged bear market is going to be glorious.

English

@nanalyzetweets @WOLF_Financial The sad reality is that most want to a) be told what to do because doing the work is difficult

b) be in an echo chamber

c) think action = performance

I think X makes you fall into these buckets. Carefully vetting/curating followings helps to get effective analysis.

English

@WOLF_Financial The quality of which is dubious at best in most cases because people on X aren't motivated to help others become better investors.

English

Tom Lee on why he loves X

“Outside of TV, X is one of the only places where you can get real financial news and conversation in real time.”

Tom Lee Tracker (Not actually Tom)@TomLeeTracker

We got to sit down and interview Tom Lee @fundstrat at FutureProof this past week Here is what we discussed: Q: What's happening in society as adoption moves toward blockchain and Ethereum $ETH? A: Wall Street is now viewing blockchain as a productivity driver. AI agents need instant settlement, finality, and security. Smart contract blockchains already offer that. Blockchain is the natural financial rail for AI agents with their own wallets. Q: Is crypto bottoming? A: Crypto winters in the past have seen 90% drawdowns. This one is severe but not that severe. Bitcoin and Ethereum could be bottoming soon. Crypto tends to bottom on bad news (i.e., war and oil). Q: How do you think about Granny Shots in small and mid-cap $GRNJ? A: You don't need a monopoly. You need a company that dominates an important, growing industry, even if it's a smaller space. That's how the best investments get started. Facebook and Netflix weren't large-caps when they began. Q: Why do you love X so much? A: Outside of TV, X is one of the only places where you can get real financial news and conversation in real time.

English

@wallstengine Trash company. I remember when they waited exactly a couple of hours before deadline to file audits for their accounting last year. How is this company run so damn bad?

English

$SMCI disclosed that federal prosecutors in the Southern District of New York have charged three people tied to the company in an alleged export-control conspiracy. Supermicro was not named as a defendant.

The company placed two employees on administrative leave, cut ties with a contractor, and is cooperating with the investigation.

English

@WillBiddy_ My concerns are growth. They've tried expanding internationally but some markers just aren't mature enough for insurance. How do you think they can re-accelerate growth?

English

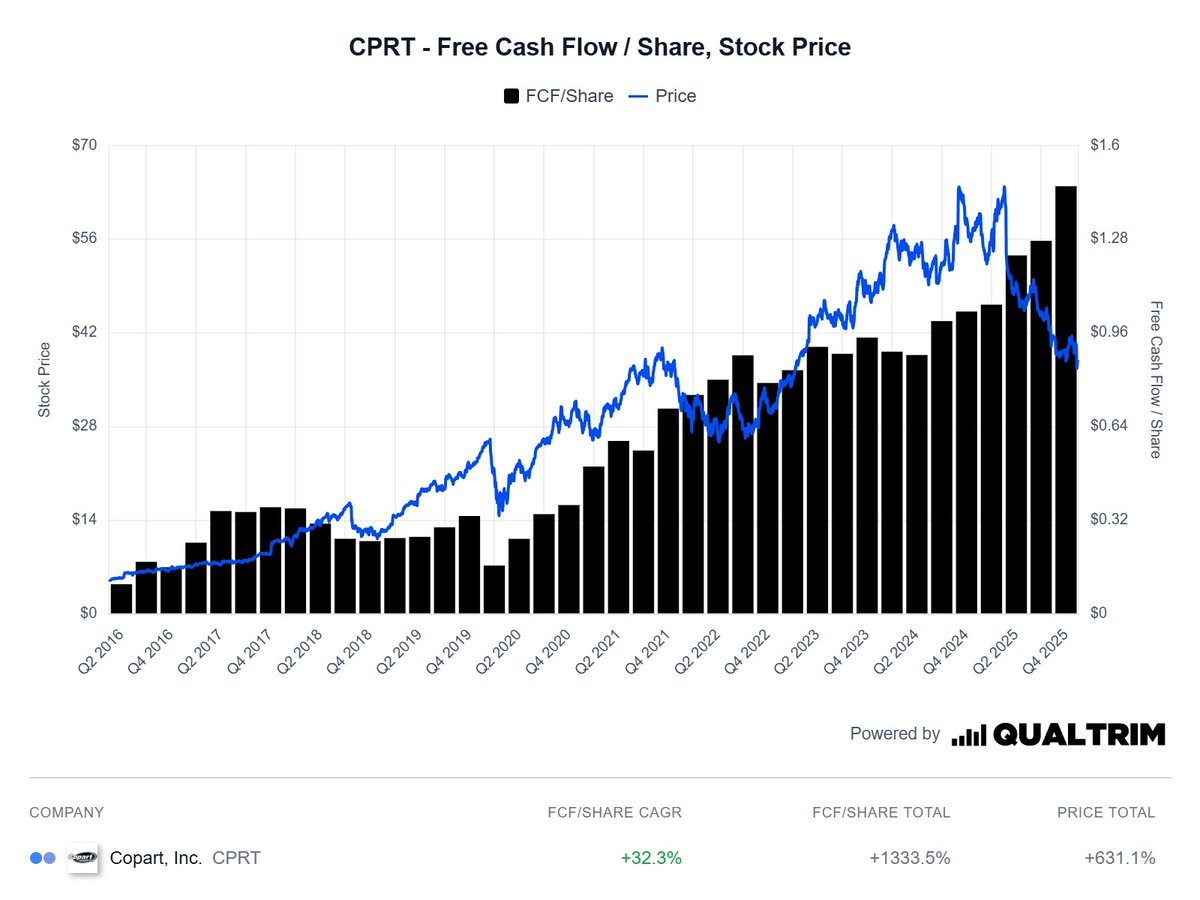

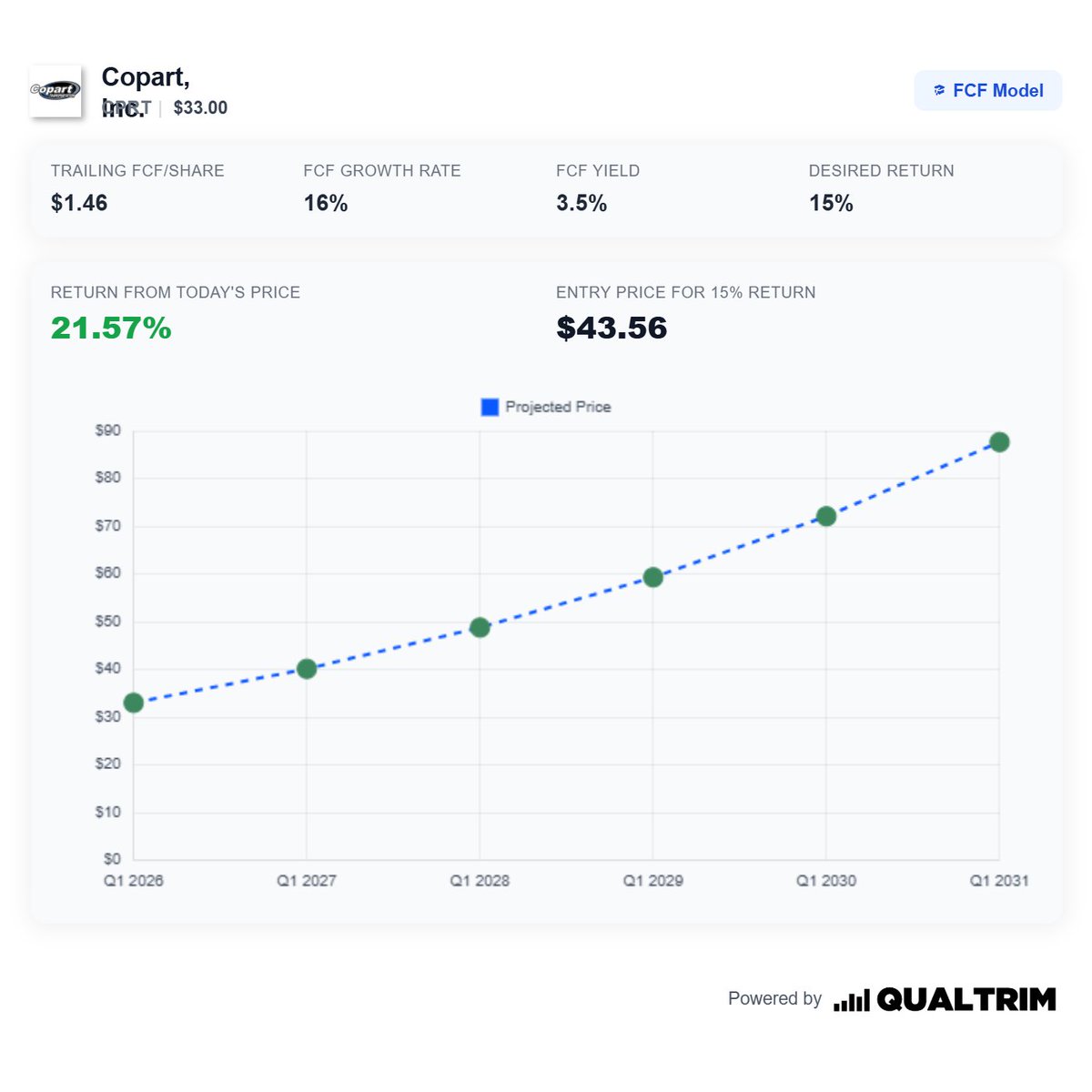

$CPRT is arguably the most disrespected compounding machine in the entire market currently.

-Incredibly wide moat

-Owns ~90% of their land

-AI beneficiary long-term

-Duopoly with largest market share

I think its about time for me to pull the trigger on this one...

English

@jwtarheel @CapexAndChill @PronkDaniel Sorry, not either of these two but I imagine a focus back into profitability/margin expansion in the financials. Wall Street is notoriously short term focused but expanding the customer base is way more important given the untapped TAM than margins at the mo

English

@CapexAndChill @CapexAndChill and @PronkDaniel - thanks for all the great intel. Serious question - what catalyst(s) will change price action (neg to pos) for $MELI (excluding overall market stability)?

English

This is another important for $MELI. They have a data flywheel moat allows them to appropriately price risk like no other.

A 20%+ NIMAL means that after MercadoLibre has completely written off the ~25% of loans that went bad, and after they have paid the costs to fund those loans, the credit portfolio is still generating a 20%+ pure yield.

The revenue is not fake, and the losses are not being hidden. The bad debt is fully expensed out of the Fintech division's profits, and the massive interest spreads in Latin America ensure that the segment remains highly lucrative even with a quarter of the portfolio running past due.

Daniel Pronk@PronkDaniel

The answer is provisions. Provisions for credit losses go directly against net income as a loss today. $MELI has 100%+ of all NPLs already provisioned (written off against earnings, and cash set aside to absorb all of them). This basically means that if the NPL goes truly bad, it's already written off, doesn't effect earnings, and is absorbed by the cash already set aside. So no, revenue and earnings are not inflated. If anything, you could argue they're under-reported, as they assume 100%+ of provisions will go bad.

English

TerraVest $TVK.TO share price has been flat for about a year now. That shouldn't come as a surprise, as the valuation ran up a lot from '23-'25.

That said, I've been feeling pretty good about the underlying business lately. There are a lot of drivers pushing in the right direction right now:

* LNG production in Canada continues to ramp. This was already positive, but now even more so d/t the Hormuz situation resulting in an LNG supply crunch. This is good for BC nat gas production -> good for TVK's PE segment.

* Crude oil is up and might stay there for a while. Good for PE, and especially Services. (Although there is a slightly counter-cyclical effect here for propane, as higher crude oil prices result in higher propane prices, which reduces demand.)

* Propane is now in a stronger position domestically as the 'electrify everything' trend has died off. In addition, a harsh winter plus an already existing desire for fleet renewal should provide a positive backdrop for compressed gas.

* US trucking rates are increasing -> positive for trailer demand.

* C-store buildout, data center buildout -> positive for HT/composites.

* The NA chemical sector appears to be inflecting a little bit. This is now being supercharged by the war in Iran, as global competitors are having a rough time sourcing cheap feedstock from the Middle East. Not saying 'the cycle has turned', but at the moment it seems like a hopeful time to be selling chemical containment equipment in North America, where feedstock is cheap and plentiful.

TerraVest has operated in a hostile environment for most of its 'modern' history, usually due to low oil/gas prices or political hostility toward fossil fuels. (E.g. cancelled oil pipelines, drilling permit freezes, heat pumps being subsidized to replace propane heating, increasingly stringent gas/oil boiler efficiency requirements, etc etc etc.) Yet even then TVK thrived. And now it appears that many of those factors are inflecting.

Execution was wonderful when conditions were poor -- what will it be like when the demand backdrop flips?

English

@WillBiddy_ Didn't even get our bounce despite okay results! Thesis remains unchanged.

English

@WillBiddy_ Still a lot of hangerover from the saaspocalyse. A good result will probably given them a bounce but very quickly will sell off. I expect the stock to remain flat. Long Adobe so will probably average down a bit.

English

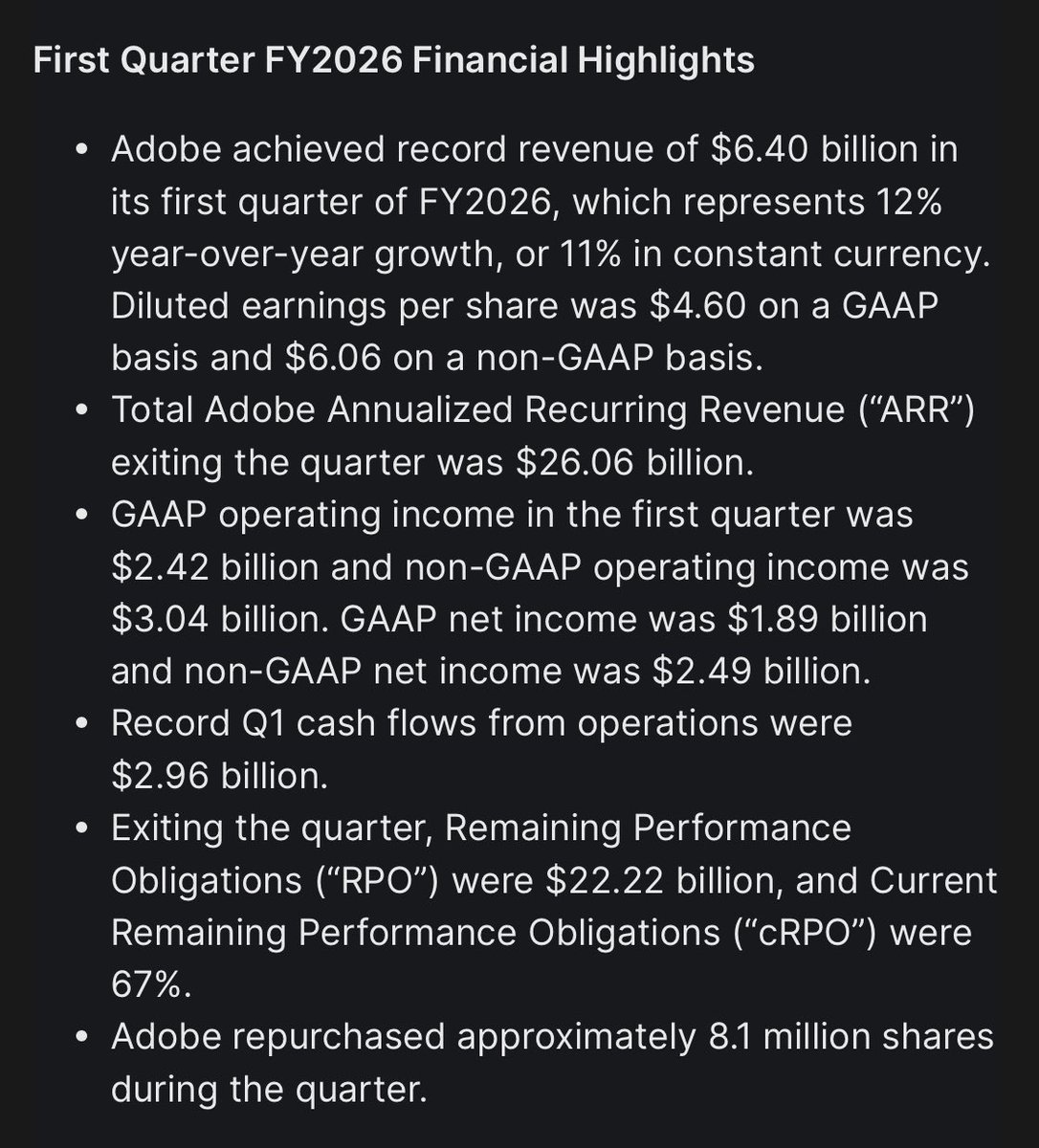

$ADBE earnings today after the bell.

If we see or hear one singular hiccup from the company I’m expecting it to near $200/share.

I think it’s a great buy under $450 so any discount is greatly appreciated beyond current price.

Excited for the results though I’ll be covering them!

English

$ADBE with another quarter of showing that there is nothing fundamentally wrong with the business but also failing to show material improvement in the business as well.

But to be truly honest the succession plans may add even more uncertainty in the mix.

English

@Nietschecapital Missiles made to bomb children's schools: I sleep

Left wing sjw social media: real shit

English

$rddt bear case: left wing shitco app

$rddt bull case: left wing shitco app

name me another company like this 😂😂

English

@QualityInvest5 I've started a position but will slowly DCA into it (if I buy a ton it will crash any 50% istg)

English

@QualityInvest5 Buying back shares at $1700 is crazy work. Either an insane vote of confidence and bullish or arrogance and capital incineration (depending on who you ask)

English

Can anyone give me a valid $FICO bear argument other than the government will regulate them to the ground (whatever that even means)

English

@ReneSellmann It's extremely rare to get one that can do both. Modest returns over a very long time period is what creates true wealth. Return chasers fail to understand that.

English

Instead of asking: "How can I earn the highest return possible?"

Investors should ask: "What are the highest returns I can sustain for the LONGEST period of time without going bust."

This changes entirely how you invest.

English

@varunv_malhotra A lot of people got burned during their lost decade but I completely agree that they've turned a corner. The prospects of Fairfax india alone make me bullish (minus the whole management fee stuff)

English

@j_enz Haha it really has a high floor. Hard to lose real capital here

English

Prem Watsa called Henry Singleton “the Michael Jordan of buybacks.”

Then he bought back over 1M of his own shares in 2025. $1.6 billion worth.

5 things making it hard for me to not buy $FFH:

(1) The float is bigger than the company. 39B of insurance float on a Market cap: of 35B. Customers pay Fairfax to hold their money.

(2) The earnings floor nobody talks about. 50B in bonds, mostly government, earning 5%. That’s 2.5B a year that shows up no matter what.

(3) The buyback is accelerating. Over 1M shares retired in 2025. 131K more in the first six weeks of 2026. He just sold half of Poseidon for 1.9B. That’s more cash coming for buybacks. Every share he retires makes your slice of the pie bigger.

(4) The bet that tells you everything.

In 2020 the stock was C$400. Prem was out of cash. So he used derivatives to make a C$850M bet on his own stock at C$481. The world thought Fairfax was cooked . That bet is now up C$3.2B. Every buyback makes it worth more. It compounds on itself.

(5) My floor math.

Bonds give me 4%. Buybacks give me another 4%. That’s 8% a year doing nothing.

But that 8% assumes the entire insurance business earns zero. It won’t. Real earning power is 5B on a 35B company. That’s 14%. The business grew book 20% last year.

It’s trading at 1.2x real book.

This is not the 2010 Fairfax that tested everyone’s patience. This is a monster hiding in plain sight.

English

@Sam_Badawi This is probably one of the most company illiterate tweets I've seen on the platform. 2 second Google search would show none of these two issues are remotely related.

English

$FICO is in its largest drawdown since the Great Financial Crisis.

The market is growing more cautious around credit risk following concerns tied to debt exposure at $OWL and $ORCL.

When sentiment shifts like this, even high-quality companies can see valuations compress sharply.

Generational buying opportunity or early warning of a broader credit event?

Aria Radnia 🇮🇷@QualityInvest5

$FICO is my second smallest holding but I can't remember the last time I was THIS pissed off over a selloff Like are we being serious? Of all companies to fall 20% in 2 days $FICO?! Moat is LITERALLY impenetrable, growth is as guaranteed as it gets What a joke, buying...

English

@HatedMoats My favourite is people taking victory laps over 5-10% downs as validation for their bearishness. My brother in Christ, it's been a week and one analyst downgrade from some no name firm. Chill tf out.

English

People here are really like:

I didn't invest in Y but invested in Z instead yesterday.

Today, Y is -1% and Z is +1%.

I am a long-term investor.

We are not the same.

English

@ThinknStocks @FinanceJack44 A nice guide is to look at when the CEO-Founder bought back shares. I got in at about 530

English

@FinanceJack44 On my watchlist. At what point would you consider entering?

English

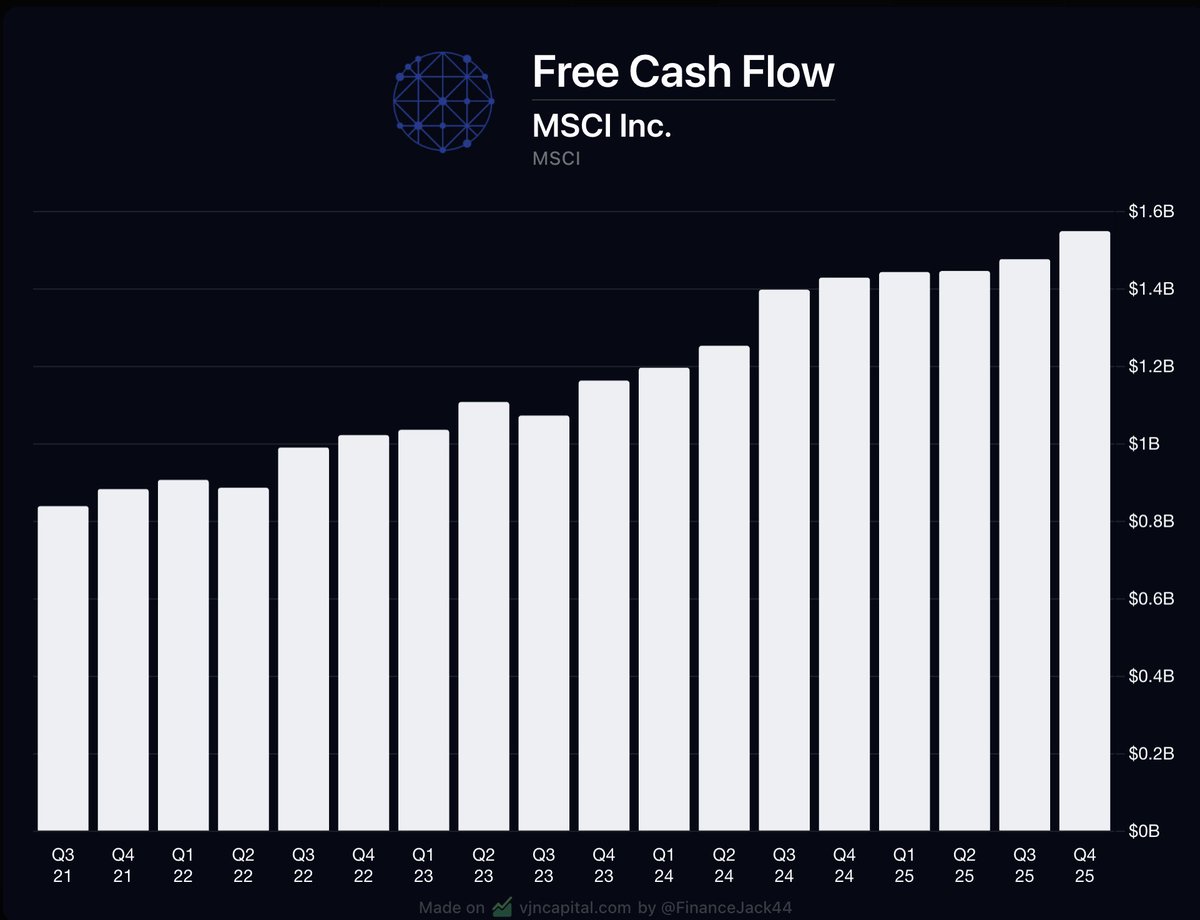

$MSCI, widely considered one of the highest quality companies in the market, is in the RED over the past year and has only returned 30% over the past 5 years.

This is in spite of the fact that revenue (+53%) and free cash flow (+76%) have continued to steadily compound.

The company still trades at a relatively high valuation of 34 TTM PE, but this is to be expected given its high margins, embedded moat, and consistent cash flow.

$MSCI is one I have my eye on if the stock price continues to underwhelm.

English