The God Particle@_Sgr_A_Star

$IREN

The bad news is that as of the the end of Q1 ~7700 GPUs were still not billing. The poor revenue figure of 33.6M for the quarter is proof of it - it's also indicative of the fact that the incremental ~7000 GPUs that started billing started extremely late in the quarter so as to generate next to no revenue in the period.

The revenue ramp has been slow. IREN is now 0 for 2 with regards to meeting their ARR guidance. No doubt about it!

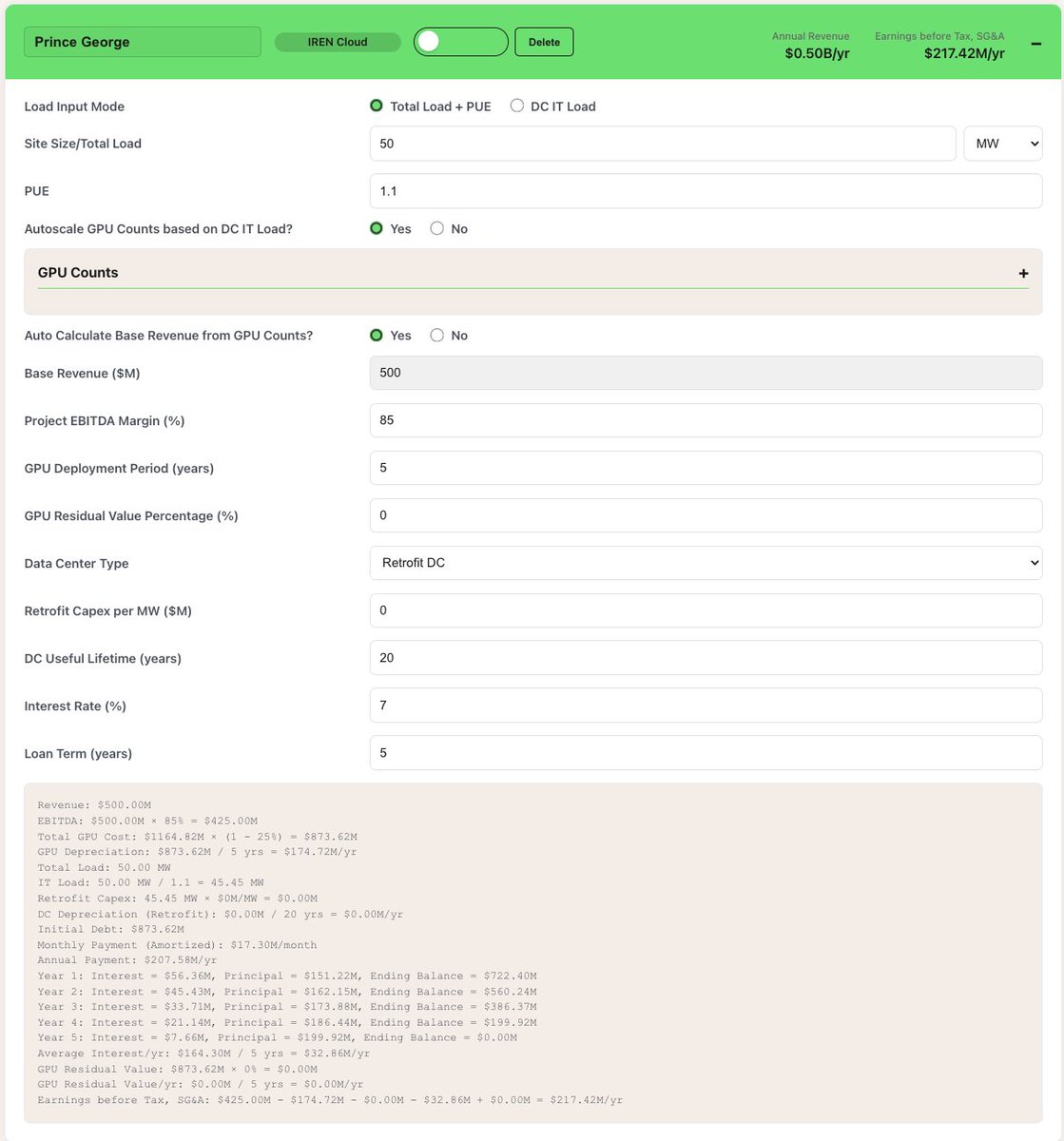

The good news is all (22K) GPUs have arrived at Prince George as of the end of Q1.

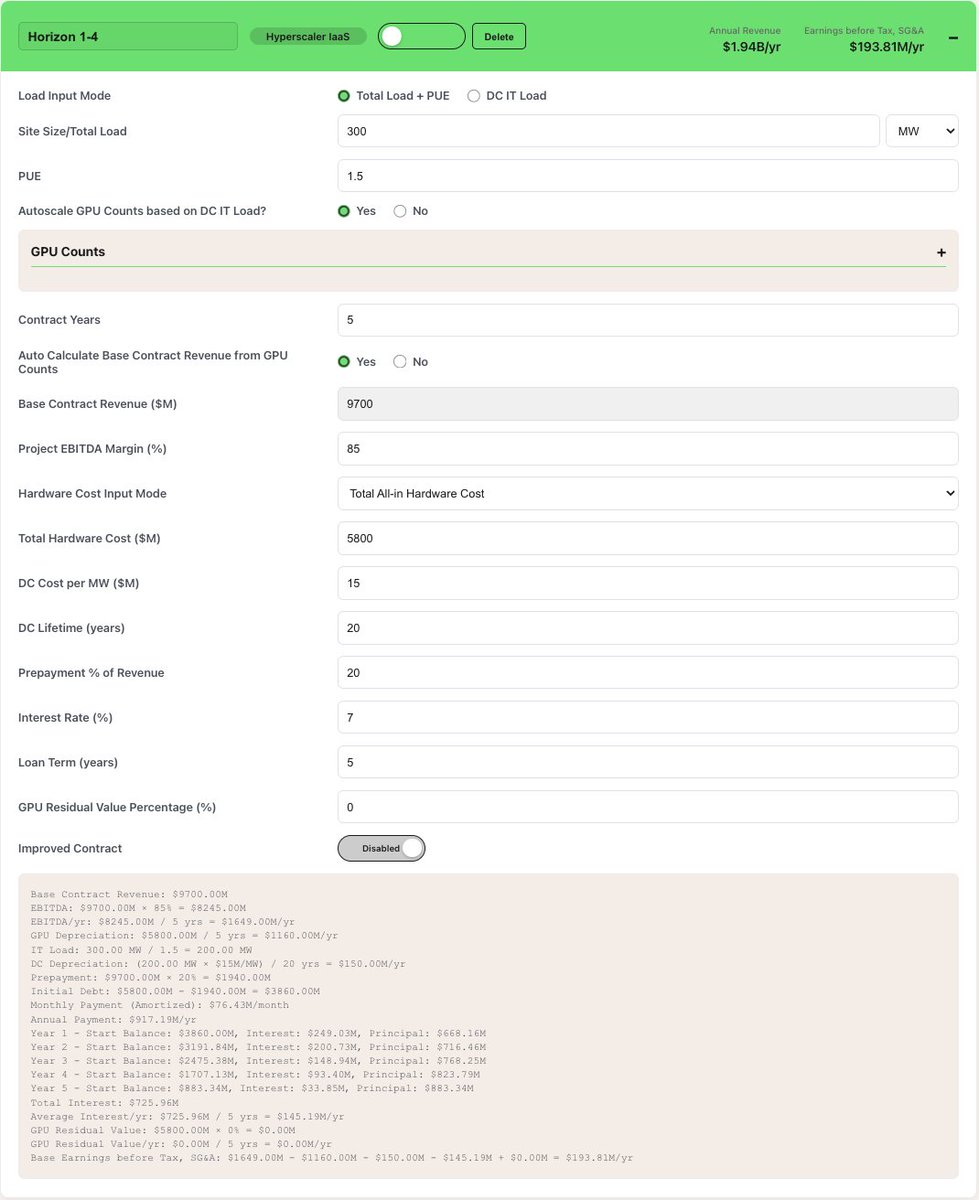

When a GPU is shipped and accepted by IREN, the gross value (cost) of the GPU is added to the balance sheet. Two separate lines on the balance sheet capture the total value of GPUs received for purchases and leases.

When you pair that data with the fact that IREN up to this point has disclosed the cost of every tranche of GPUs they've purchased to date, it allows us so solve how many GPUs have been shipped/accepted by IREN.

As of the end of Q1, the company had 1.1B worth of GPUs on the balance sheet against 1.2B worth of GPUs they've purchased for Prince George. The $96M delta is a tranche of 1200 leased GB300s (liquid cooled) that the company hasn't received yet because they've yet to commit to the how the new 10MW DC hall at PG will be utilized (source: Dan Roberts spaces with @FransBakker9812 and @bitcoinbutcher1).

As mentioned in my previous posts, when a GPU contract starts, the remaining value of the contract is added to the RPO "contract book". Using the next 12-month RPO as a proxy for exit ARR, we can convert that figure to billing GPUs.

Using the balance sheet, cost of GPUs, and RPOs allows us to track GPUs in stages from procurement to received to billing. Looks a little like the table below.

The data also verifies the comments on the earnings call about the remaining GPUs ongoing "commissioning".

Although these GPUs were supposed to be billing as of the end of Q1 (e.g., "500M ARR"), it's reassuring that the data suggests the GPUs had arrived by the end of Q1 - and whatever issues at PG (be it GPU delays, or operational issues) are now behind them.

May the skies be clear moving forward! Whew!