English

Joseph Guinta

1.3K posts

@joeguinta

Managing Member - Fair Haven Capital LLC - Investment Manager - Former Hedge Fund GP. Nothing that I say should be considered Investment Advice.

Additional 87M shares traded on 8/25 leaving 621M left to be sold before we see selling pressure abate. At this rate it’s looking like an additional ~2 weeks before we can see a bounce in $KVUE

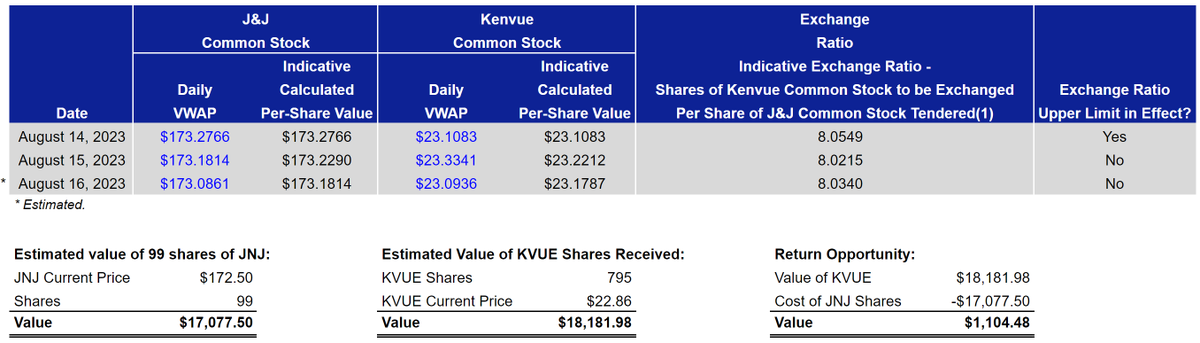

$JNJ / $KVUE Exchange Offer - current numbers based on VWAP pricing through 1pm ET. Upper limit is not in effect (likely won't be), and the ratio is somewhere around 1 JNJ for 8.02x KVUE.