Sabitlenmiş Tweet

Jacob Kim

266 posts

@kuretide

Currently making a value investment in $INV $AUR $ABCL

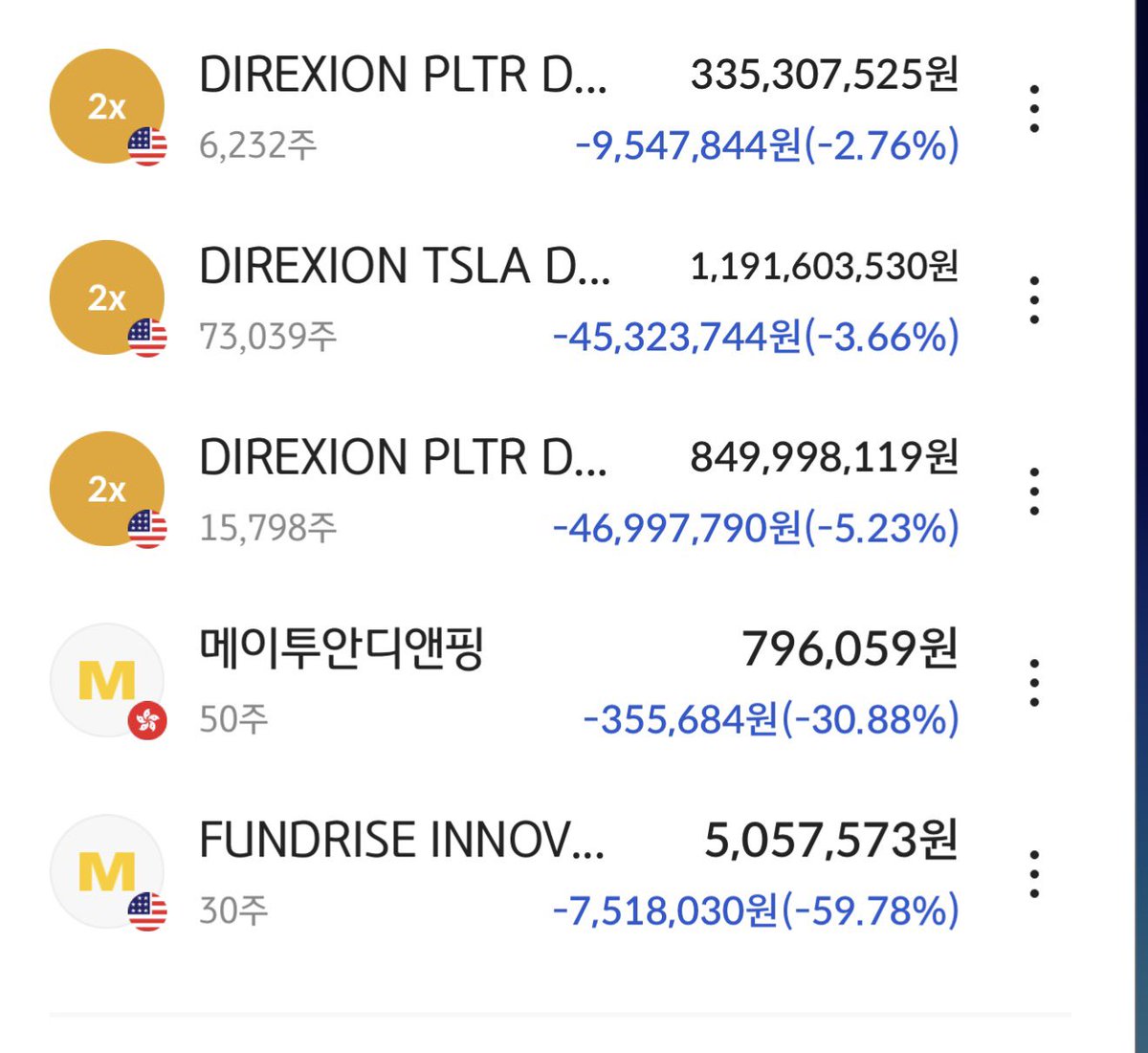

직원들이랑 술먹다가 투자 하냐고 물어보길래 미국장 손절 -25퍼 하고 새마을금고랑 신협 예적금 하고 있다고 하니까 술 사주셨다 3satl 적립 예정

$INV CEO call at 5:00pm ET on April 27, 2026 featuring executive commentary from the chief executive officers of Accelsius, AeroFlexx, and Refinity. The call will provide investors and analysts with a direct, in-depth look at the commercial progress, operational execution, and capital formation strategies across Innventure’s operating companies. During the event, CEOs Josh Claman of Accelsius, Andy Meyer of AeroFlexx, and Bill Grieco of Refinity, will discuss recent milestones, customer and partner traction, and market opportunities of their respective companies. ir.innventure.com/news-releases/…

최근에 깨달았다. 돈을 많이 모아야 하는 이유는, 내가 좋아하는 사람을 더 만나기 위함보다는 내가 싫어하는 사람을 더 이상 보지않을 수 있다는 것이다. 보기 싫은 사람만 안 봐도 수명이 최소 10년은 늘어날 거 같다.

Big development for $SOLS + $CC (also $INV $VRT $ETN): Nvidia Director of Data Center Cooling and Infrastructure Ali Heydari showcased OMNICOOL at the ARPA-E Energy Innovation Summit, a 250kW pod cooled by pumped two-phase R-515B and R-1234yf (supplied by $SOLS + $CC) achieving PUE <1.05 and ZERO water consumption. Heydari is on the record that PG25 has limits and this validates two-phase on the $NVDA roadmap (note this project started 4 years ago). This was done in collaboration with $VRT and $ETN (Boyd). $VRT is also a $INV partner. Incrementally positive for these names but is another datapoint that this is a competitive market and $INV / Zutacore likely will not be alone in two-phase cooling. IMO refrigerant players Solstice Advanced Materials $SOLS and Chemours $CC are the best way to play two-phase cooling, as they are positioned to win regardless of vendor.

Goldman Sachs projects global power demand from data centers to grow 220% by 2030 relative to 2023 levels. At the same time, the global data center liquid cooling market is projected to grow from $4.07 billion in 2026 to $27.65 billion by 2033, at a CAGR of 31.5%, according to recent industry analysis. The driver is straightforward. AI, machine learning, and next generation computing are pushing chip densities beyond what air cooling can manage. The industry is not debating whether liquid cooling will become the standard. It is debating how fast. Accelsius is recognized among the key market players shaping this space, delivering two-phase direct-to-chip cooling solutions built for the demands of today and the infrastructure requirements of tomorrow. This is the kind of market Innventure was built to enter. A validated need. A technology solution. And a company built to scale. Learn more about Accelsius: accelsius.com Sources: Goldman Sachs Research, Masanet et al. 2020, IEA, Ember, Cisco

Big development for $SOLS + $CC (also $INV $VRT $ETN): Nvidia Director of Data Center Cooling and Infrastructure Ali Heydari showcased OMNICOOL at the ARPA-E Energy Innovation Summit, a 250kW pod cooled by pumped two-phase R-515B and R-1234yf (supplied by $SOLS + $CC) achieving PUE <1.05 and ZERO water consumption. Heydari is on the record that PG25 has limits and this validates two-phase on the $NVDA roadmap (note this project started 4 years ago). This was done in collaboration with $VRT and $ETN (Boyd). $VRT is also a $INV partner. Incrementally positive for these names but is another datapoint that this is a competitive market and $INV / Zutacore likely will not be alone in two-phase cooling. IMO refrigerant players Solstice Advanced Materials $SOLS and Chemours $CC are the best way to play two-phase cooling, as they are positioned to win regardless of vendor.