GrowthStockGuru retweetledi

GrowthStockGuru

9.4K posts

GrowthStockGuru

@man_growth

Co-Host of @slaptheaskshow with @lukeknouse Growth Stocks on the OTC and Nasdaq. Actively looking for the next big blockchain innovations #bitcoin #stablecoin

Episode 31 ➡️ Katılım Eylül 2020

2.3K Takip Edilen1K Takipçiler

GrowthStockGuru retweetledi

GrowthStockGuru retweetledi

Comcast running ads shilling their new network upgrades

Probably nothing

$HLIT

Comcast@comcast

Before, during, and after severe weather strikes, we're strengthening infrastructure, mobilizing resources, and implementing innovative AI and machine learning technology to help communities weather the storm.

English

@BryzonX @johnnyli_xf Been looking through your profile @BryzonX it is been full of gems. I love your thesis on $HLIT. Looks like a hidden gem in the AI infrastructure build out. I am long as well

English

@johnnyli_xf I really appreciate that bro! Just been posting my thoughts as they come. Much love!

English

@BryzonX @AtlasShrug1 Will be interesting to see how earnings go Monday afternoon

English

I’d also like to note that the Nokia x NVDA partnership really influenced my decision as it validated my thesis that software is the only way upgrade telecom & broadband because there is no way they can dig into the ground and replace every single cable

This for 1 requires a lot of time and money

English

I have just went long Harmonic Inc. $HLIT

Here’s my thesis:

As you may know by now $NVDA recently invested in $NOK to upgrade telecommunication networks to run AI at the edge on cell towers

They are using Nokia’s anyRAN software to turn their cell towers into mini data centers to monetize AI

This method completely overhauls the need to physically rebuild all of the current physical infrastructure companies like T-mobile already have in place with just a simple software update

Why does this matter for Harmonic?

Well broadband/cable companies have been left in the dust for the longest due to their network infrastructure being stuck in the 90's where they aren't able to process the massive amounts of data that AI generates

At GTC 2026, Comcast and Charter (the 2 biggest broadband companies) confirmed they are moving $NVDA RTX 6000 Blackwell GPUs out of distant data centers and into their local neighborhood hubs

They are transforming their networks into a distributed AI Grid

You can't just put an NVIDIA GPU in a hub and expect it to work with a 30 year old cable network

Harmonic has a monopoly on what's called "vCMTS" which modernizes broadbands network infrastructure with a simple software upgrade just like NOK

This means broadband companies like Charter & Comcast will finally be able to monetize AI in business and residential areas using $NVDA GPU's to do things like offer personalized commercials to individual customers using AI at the edge in real time

Here is the huge opportunity for Harmonic..

As of 2026, broadband companies have gone into a state of emergency because they are unable to monetize AI like they want so they are going through a MASSIVE CAPEX cycle specifically for 'Network Evolution'

Comcast and Charter are spending $22 billion combined over the next few years to build a "Smart Grid." with 2026 being the most aggressive as they aim for over 50% of their capex to be spent to speed up the process

This is reflecting in Harmonics book as they now have a record $570M in backlog, up 77% YoY and recorded a 3.5 book to bill ratio in Q4 2025 ALONE 🤯

A $1.2B market cap with a $570M backlog which is probably at $600M+ now since this was announced months ago

Underneath the hood you may notice that the numbers look horrendous, however this is because they just sold their old legacy video business to go all in their "Virtualization" high margin SaaS business which is now growing at 33% YoY at a 55% margin showing off some serious operating leverage

The TAM for Cable Modem Termination Systems (CMTS) is estimated at $5.18 billion for 2026 with only 15%-20% of the entire global broadband infra virtualized giving them a HUGE runway for growth in the coming years

Harmonic is currently only doing $450M in revenue. This means they have only captured less than 10% of their immediate SAM, despite having a monopoly..

However, I expect this to grow even faster because now there are actual government incentives behind this

1st)

Starting May 8th, the FCC is starting an initiative called "Delete, Delete, Delete" which is a legal mandate for cable companies to stop wasting billions maintaining 30 year old copper wires & old hardware hubs

This is freeing up tens of billions in maintenance CapEx being redirected to upgrading their network

2)

The gov is currently handing out $42B in BEAD grants for rural high speed internet. To win these grants, operators have to deploy fast. You can’t build a physical hub in a month, but you can deploy Harmonic’s software in days essentially paying broadband to upgrade their network

For the longest the biggest risk was their customer concentration risk

but as of May 2026, rest of world revenue grew 33% YoY and now makes up 41% of their business

Meaning they are no longer just a USA merchant, they are becoming the global standard for the AI Grid with Comcast & Charter leading the way for the rest of the world to follow suit

Lastly, the chart looks absolutely stunning

It is clearly inflecting as management is making it clear that they are no longer a boring video business, but a pure play global AI infrastructure enabler

Now trading above all monthly moving averages which are starting to curl up and now breaking out of this massive bull flag

I really like this name going forward and think the cat comes out of the bag in their next earnings

NFA.

English

GrowthStockGuru retweetledi

GrowthStockGuru retweetledi

The DoW is investing aggressively in autonomy, and the defense landscape is shifting. Incumbent and emerging players are competing on more equal footing. wsj.com/business/defen… (1/3)

English

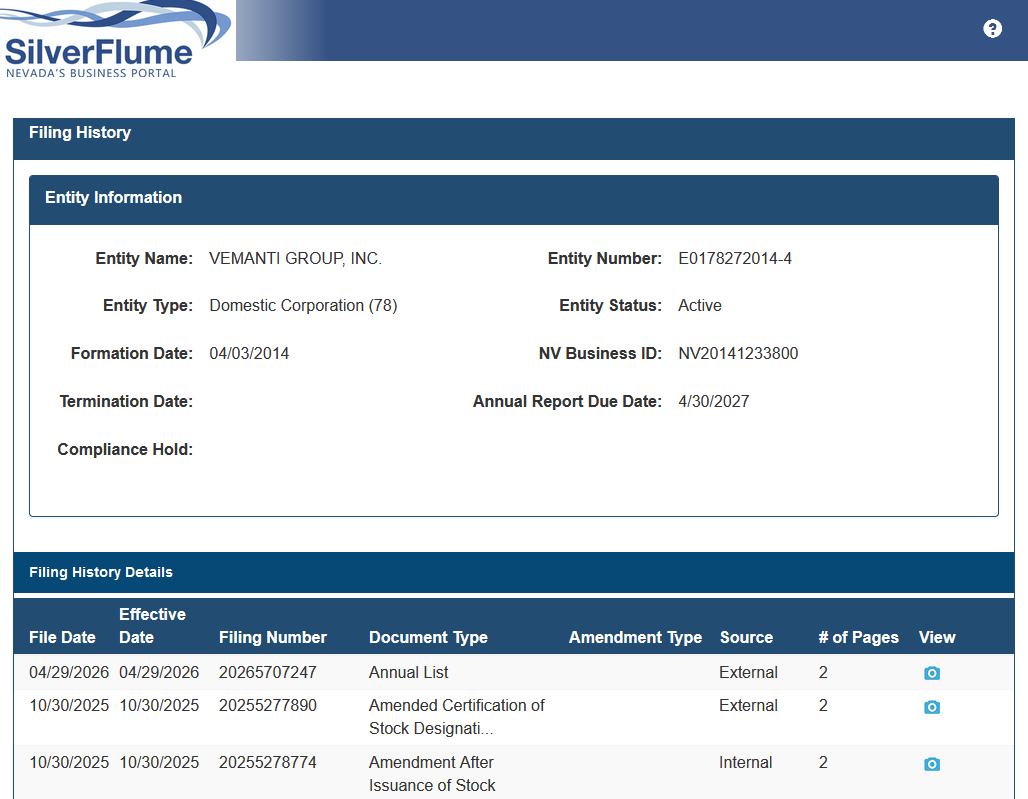

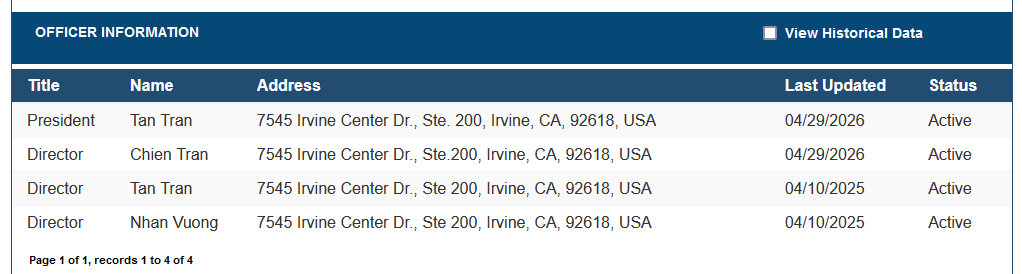

@StockTrader187 @Romulus4488 @tanctran Got it, wonder what this filing is then. Just an annual update as to what is going on at the company?

English

GrowthStockGuru retweetledi

Frontier Airlines:

“And to my friend Spirit Airlines. Rest now. We have the watch. See you in Valhalla.”

English

GrowthStockGuru retweetledi

GrowthStockGuru retweetledi

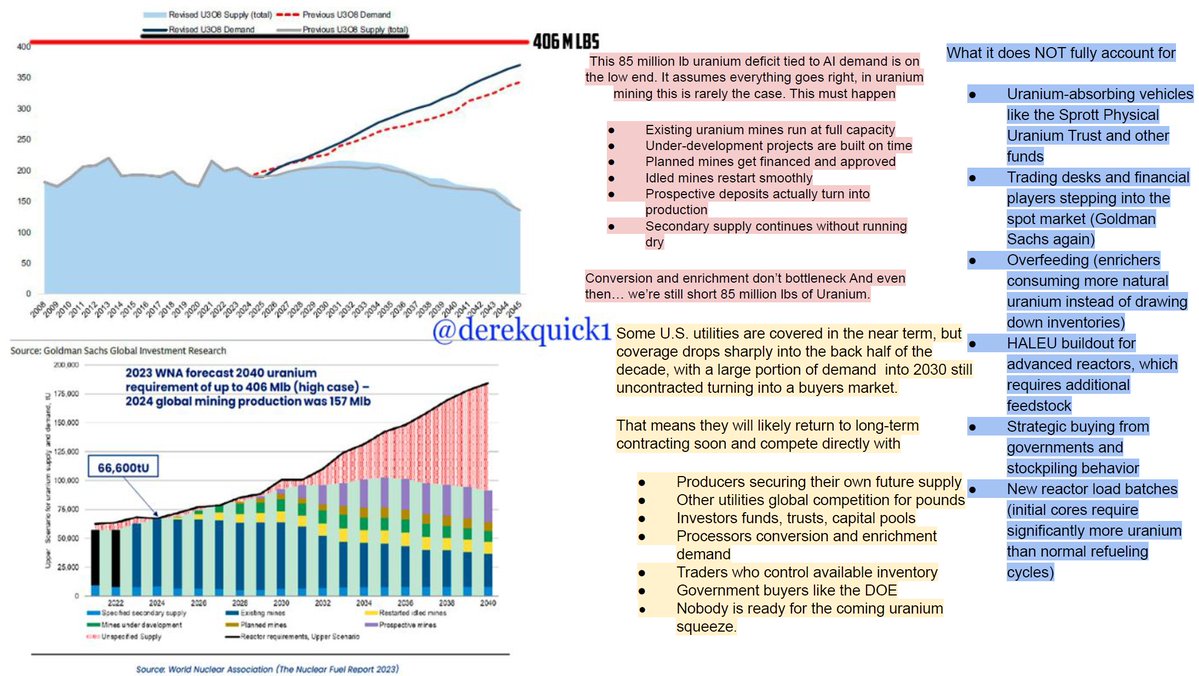

Uranium & Nuclear Energy Stock Squeeze via the Global AI Power Paradox is HERE, $1,000 Uranium is probable as it is the true bottleneck sector. U.S. Uranium producers have a smaller market cap combined than that of Dogecoin.

Leopold Aschenbrenner dropped his Situational Awareness report in mid-2024 with charts that sounded insane about AI demand for power. He grew his fund from $225 million to $5.5 billion since investing in stocks related to the sector but he missed something.

The real bottleneck is here, Uranium & Nuclear energy via baseload power. And that’s about to ignite the uranium/nuclear supercycle. The AI Power Paradox straight from the data.

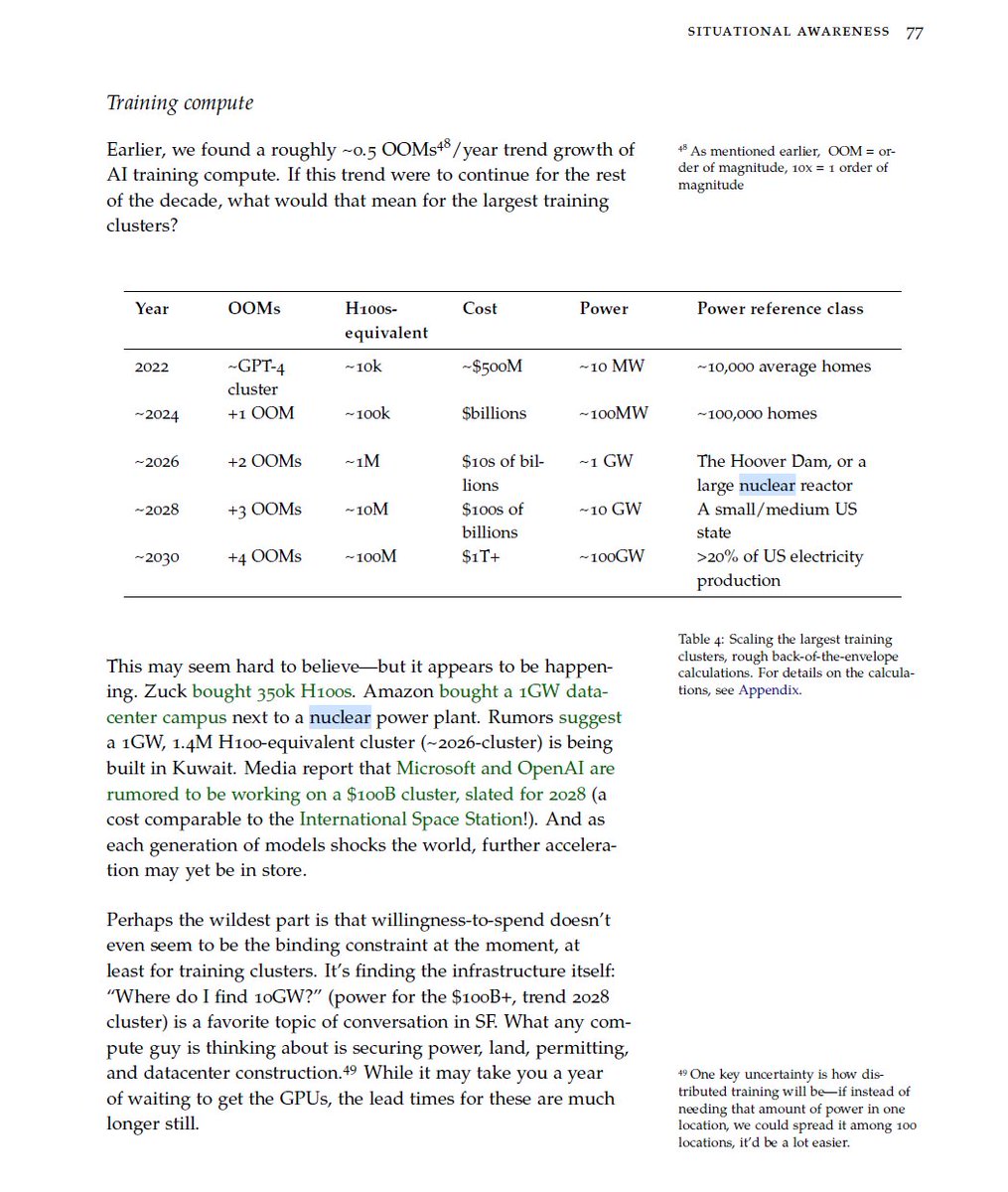

Page 77 in his report- by 2030 the largest single AI training cluster alone would need 100 GW >20% of total U.S. electricity production.

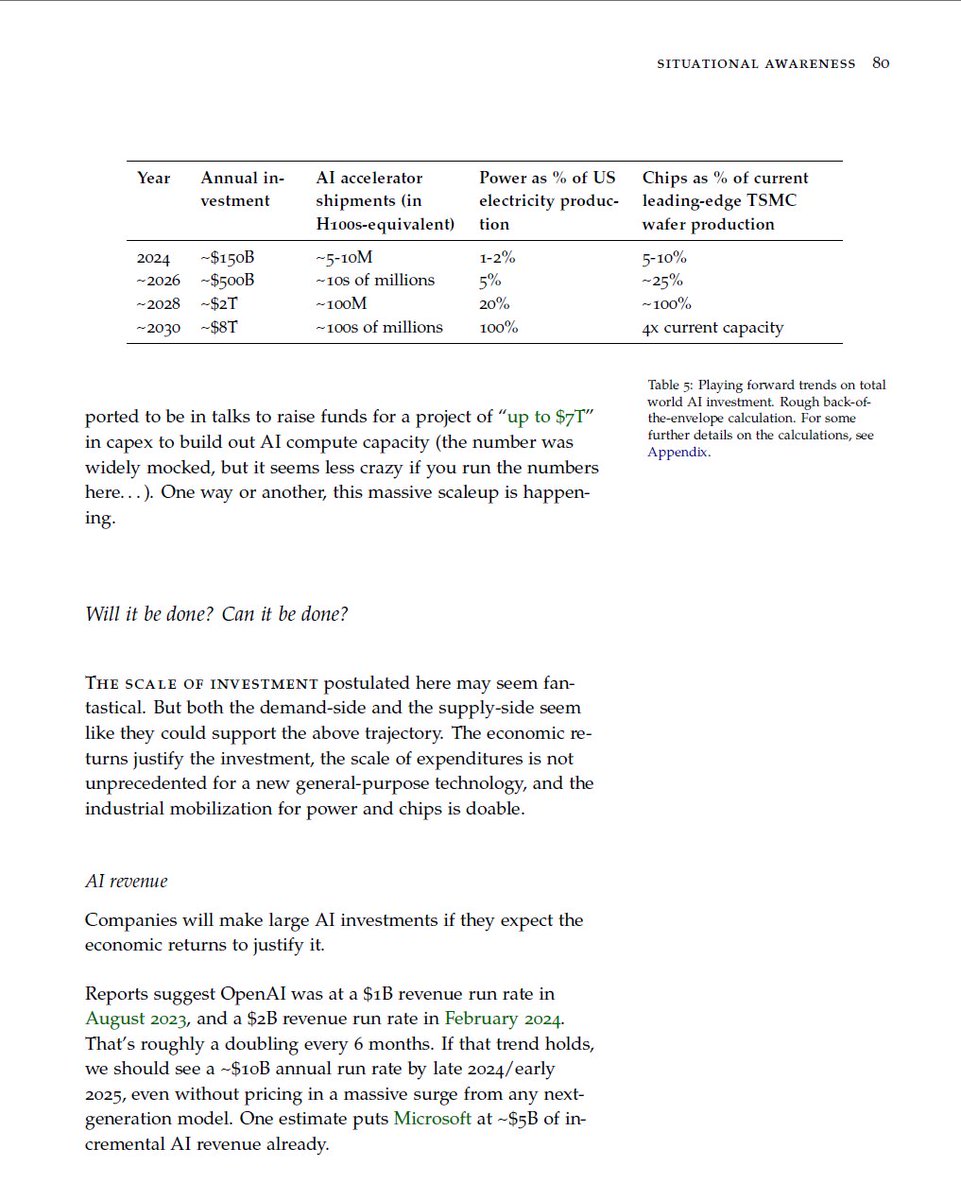

Page 80-Table 5, overall AI compute training + inference across everyone hits 100% of current U.S. electricity and $8 T annual investment.

Most people laughed. Now in 2026 the 2026 row he projected 1 GW clusters, 5% of U.S. power is already happening in real time. xAI Colossus, Meta Prometheus, Google campuses, Amazon nuclear-adjacent builds we’re living Leopold’s table. And the stocks that rode the first wave? Many are up 1,500% to $3500%.

• NVDA GPU scaling is driving 300%+ increases in power needs every few years. H100 → Blackwell → Rubin racks now hit 100+ kW each. New chips are more efficient per FLOP, but cluster sizes are exploding so fast that total power draw still skyrockets. Some centers are postponed until they can find power.

• Global data centers already consume 415 TWh annually. IEA base case: 945 TWh by 2030 which is double current levels. Some high-growth scenarios hit 1,000+ TWh even sooner. AI workloads -accelerated servers are growing 30% per year and driving almost half the increase.

• Big Tech is dropping hundreds of billions in capex $130B+ in Q1 2026 alone from Microsoft, Google, Amazon, Meta. NVIDIA AI factories are city-scale: 100 MW to 1 GW+ per site.

• Grids can’t keep up. Permitting, transformers 5-year backlogs, transmission bottlenecks, intermittent renewables all failing. Only reliable, always-on baseload works at this scale nuclear restarts + SMRs and nat gas. Renewables + batteries don’t cut it for 24/7 AI training/inference.

Why Uranium & Nuclear Go Parabolic to $1,000/lb scenario, This is a tiny, supply-constrained market meeting explosive, urgent demand the classic squeeze setup as it has done in the cyclical past.

• 85 million lb structural annual deficit (Goldman Sachs) from AI alone , 1.7B+ lbs over 20 years even with some new supply and no issues with current mines which is rare.

The largest Uranium producer is establishing a reserve for new buildouts locking up cheap uranium the market expected.

• U.S. reactors need 50M lbs/year. U.S. producers made <3% of that last year. Sprott Physical Uranium Trust alone now holds over 81 million lbs nearly 2 years of fuel for the entire U.S. fleet.

There is a Russian Uranium ban now that really starts to take effect into 2027.

• Mining lead times are 2+ years minimum even for permitted projects. You can’t just flip a switch.

• Historically in the 1970s Big Oil flooded into uranium and mined hundreds of millions of lbs while America built 55 reactors in 10 years. Today?

The Mag 7 and especially $NVDA ecosystem players have the capital to do the same, they’re already signing multi-GW nuclear deals Meta’s 6+ GW spree with Vistra/Oklo/TerraPower, Microsoft TMI restart, Amazon 1.9 GW PPA + SMRs, Google Kairos, etc.

Securing power is now existential for AI growth. But we can now build nuclear FAR faster than the 1970s boom. SMRs (small modular reactors) are factory-built like Legos modules ship to site and assemble in 2–4 years vs 7–10+ years for traditional large reactors.

-Global nuclear build out accelerating 70+ reactors under construction 400 operational 300+ permitting.

DOE studies show 80% of retiring U.S. coal plants are perfect for coal-to-nuclear conversions, reuse the existing grid connections, cooling towers, switchyards, workforce, and sites for massive time/cost savings 15–35% cheaper.

Advanced manufacturing, AI-optimized designs, 3D-printed components, and HALEU fuel make scaling even quicker. U.S. policy tailwinds are insane, Russian uranium banned, nuclear declared critical for national security and AI, funding for SMRs/fuel cycle, faster permitting.

With U.S. national security at risk AI supremacy vs China, energy independence, powering the entire AI economy, the current administration in Washington is going all-in, executive orders streamlining NRC approvals, Defense Production Act on domestic uranium/fuel, co-locating SMRs with AI data centers, and treating nuclear as critical infrastructure.

This is becoming a U.S. energy independence + GDP imperative. The Leverage Is Stupid At current $86.45/lb spot and $91.50 which is what matters most.

Many U.S. producers are already profitable but have open contract windows like $UEC.

• But when uranium moves to $120–$200 sustained (or higher in a true squeeze) margins explode.

• $UEC at a $37 cost to produce Uranium-From

$87 → $200 = +220% margin.

From cycle lows? 4,000% increase in margins.

• At $1,000/lb? Profit jumps to $964/lb +1,792% vs current in a 19× margin expansion. Even from low-cycle $40, it’s +24,000%.

Equities will go nuclear long before the commodity fully reflects it. Uranium stocks are leveraged plays on the price of uranium- Like a 0DTE contract but more volatile.

Now people hear $1,000 and think this is expensive, well Raw uranium is still a tiny fraction of total costs. Full front-end fuel, uranium + enrichment + fabrication is only 15-20% of total electricity cost for new nuclear plants and 17% for operating plants per NEI data.

Raw uranium concentrate itself is less than 10% of overall generating costs (often 5-8% of LCOE or 0.377 ¢/kWh). Even at $1,000/lb, it barely moves the needle on total power price for reactors or AI data centers capital costs and buildout dominate.

This is why hyperscalers and utilities can absorb parabolic uranium prices without killing economics.

U.S. uranium producers combined are still smaller than meme coins. $UEC, $UUUU, $LEU and the handful with real assets/claims in Texas/Wyoming/West are sitting on billions of lbs of historic resources ready to restart once price justifies it.

The 1970s Uranium claim maps are locked and loaded. This is the Global AI Power Supercycle, Leopold’s 2030 vision was the warning shot and everyone flooded to Semiconductors $SNDK +3,350% 1 year, and other forms of energy $BE+1,667% 1 year.

But the market is still asleep to what baseload nuclear/uranium actually means for the next decade. Big Oil → Big Tech nuclear M&A wave incoming.

Uranium equities will massively outperform the commodity itself even those that are not making any cashflow. A Uranium Squeeze is coming.

The funny thing is, Leopold didn't get much traction either when he posted his paper for free, he did get hundreds of millions in funding to invest which paid off.

Who else sees the power bottleneck as the next 10x leg?

$NVDA made the chips. Now nuclear makes the baseload power. The Uranium squeeze is just getting started.

English

GrowthStockGuru retweetledi

Thank you Elizabeth Warren for killing Spirit Airlines, a budget airline for low income consumers

Elizabeth Warren@SenWarren

I've warned for months that a @JetBlue-@SpiritAirlines merger would have led to fewer flights and higher fares. @JusticeATR and @USDOT were right to stand up for consumers and fight against runaway airline consolidation. This is a Biden win for flyers! apnews.com/article/jetblu…

English

@StockTrader187 @Romulus4488 Do you have access to the annual list?

English

@NuclearFact Thanks for the reply and sharing your perspective

English

@man_growth It’s an investment based on the nuclear narrative and speculation, not fundamentals.

Hope is for some deals to be announced in the next 6-12months.

English

FELLOW DEGENERATES, listen up 🚀☢️

While you zoomers are still simping for $OKLO‘s hyped sodium-cooled toy (~$12-13B market cap, Sam Altman vibes, Meta mentions), the REAL alpha is $IMSR — trading at roughly ~7% of OKLO’s valuation with straight-up superior tech.

$OKLO at ~$13B.

$IMSR at ~$800M.

Same nuclear renaissance. One-tenth the price. That’s the story.

WHY THIS GAP IS INSANE:

•Molten salt chads dominate.

IMSR runs 600-700°C with fuel in the salt. Walk-away safe (freeze plug kills any runaway). OKLO sodium? Leak = instant fire.

•High-temp industrial heat beast.

Hydrogen, desalination, synfuels, chemicals, data center steam — IMSR does it all. OKLO is mostly power. IMSR is full-stack for AI + heavy industry.

$OKLO bros coping with “b-but partnerships!”

$IMSR chads are sitting in the 10x re-rate waiting room. When the market wakes up to better tech at 1/10th the price… gap closes violently.

This isn’t financial advice DYODD

Load $IMSR or cope later. ☢️💎🚀

English

Uranium & Nuclear energy squeeze is coming. I expect to see $200 Uranium prices long term in the next 12+ months. Sprott physical Uranium trust has basically taken out most of the supply utilities thought would be there a few years ago 81.2 million lbs of U308, over the next 5 years from AI demand we will see another 85 million lb structural deficit along with the 81 million Sprott has locked up. Might be one of the biggest squeezes in the last 50 years.

English