Martin Koopman

718 posts

Martin Koopman

@martinkoopman

AI Innovator 🤖 Financial Tech Leader 💾 Kindness 🙏 CPO+Co-Head of AI @Broadridge Opinions are my own or stolen from smarter people

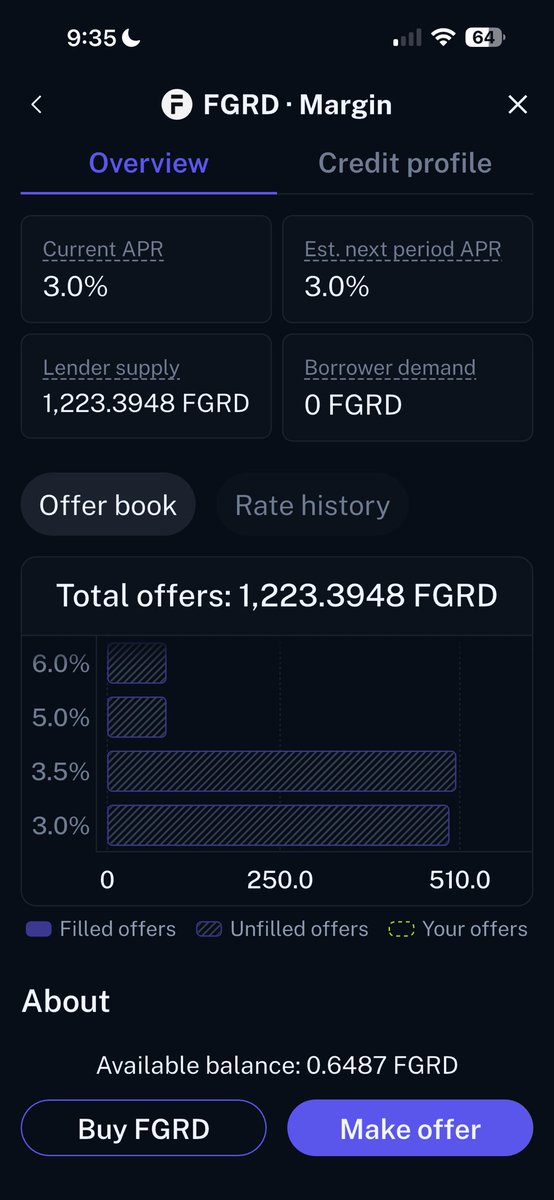

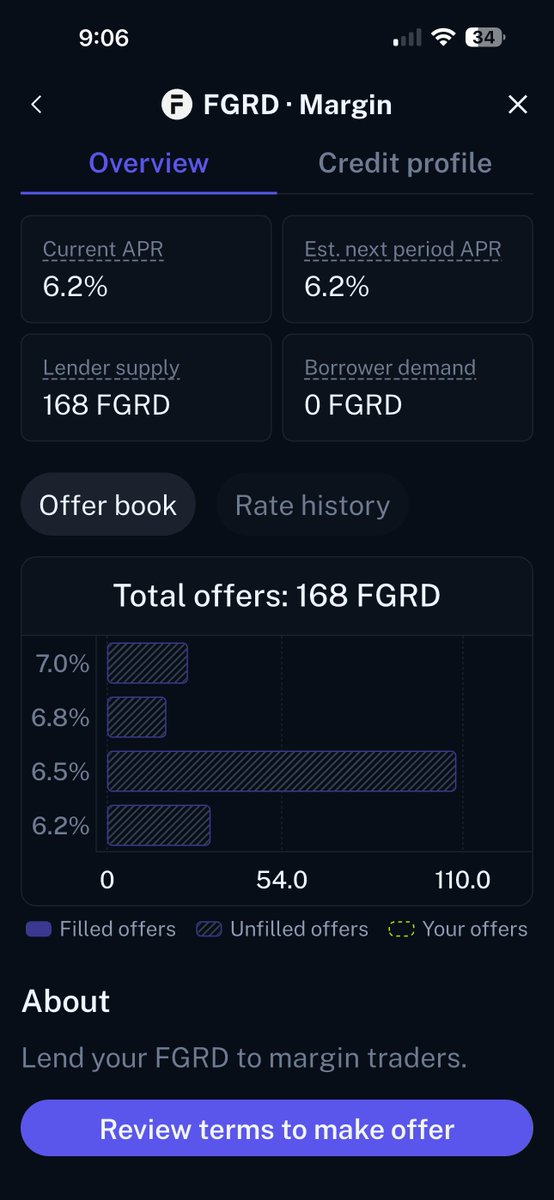

Three days ago I posted about @Figure pricing a secondary offering of its Series A Blockchain Common Stock. I said I'd follow up once the issuance hit the explorer. So here we are 🦙🔍 On February 18, FGRD closed. 4,375,000 shares of public equity - natively issued, traded, and settled entirely on blockchain. Goldman Sachs, Morgan Stanley, and Cantor ran the books. SEC registration went effective Feb 17. Priced at $32/share. Goldman Sachs underwrote a blockchain-native equity offering that bypasses DTCC entirely. Read that again. What Actually Happened The offering was upsized. Originally 4.23M shares - ended up at 4.375M. Total shares sold by selling shareholders: 4.6875M (457,500 more than planned). Demand showed up. Structure: non-dilutive. Existing investors sold Class A shares to underwriters, Figure repurchased 312,500 Class A shares back into treasury for ~$10M. No new share issuance. Clean. FIGR (the Nasdaq-listed Class A) is sitting around $35.50 today. $7.96B market cap. Analyst consensus Buy, avg target $59 (+66%). Q4 2025 earnings drop Feb 26. The Full Stack, Live I mapped out the architecture in my last post, but now every layer is operational: → Issuance: onchain (Provenance Blockchain) → Trading: Figure's non-custodial ATS - 24/7/365, limit order book → Settlement: instantaneous via $YLDS → Custody: self-custody wallets → Lending: Democratized Prime (DeFi protocol on Provenance for stock-based borrowing/lending) → Governance: direct onchain voting, no proxy firms → Convertibility: 1:1 into FIGR (Nasdaq Class A) Every layer of the equity capital markets stack - rebuilt on blockchain. Running. Figure Securities (FINRA/SIPC member, BrokerCheck verified) operates the ATS. Third-party wallets can plug in directly - no introducing brokers needed. $YLDS Update I checked the chain again. explorer.provenance.io/asset/uylds.fcc Three days ago when I posted: Supply: $463.9M Holders: 2,491 Transactions: 34,276 Today: Supply: $593.7M Holders: 2,583 Transactions: 36,149 That's +$130M in supply and +92 new holders in three days. $YLDS - Figure's SEC-registered, yield-bearing stablecoin backed by Treasuries + repo - is the settlement currency for every FGRD trade. Your settlement layer earns yield while idle. The growth tracks with the FGRD launch activity. More equity trading onchain = more $YLDS needed for settlement. FGRD Onchain : Live Data Last time I checked, the blockchain stock marker on Provenance was empty: a shell waiting for the offering to price. It's not empty anymore. explorer.provenance.io/asset/nfgrd Asset Name: fgrd Supply: 4,744,999 Holders: 61 Transactions: 484 Marker Status: Active Marker Type: Restricted Mintable: true Governance: enabled 61 wallets holding onchain equity in a publicly traded company. 484 transactions already processed. Restricted marker type - same compliance-gated structure as $YLDS. Onchain governance enabled, meaning FGRD holders can vote directly from their wallets. No proxy firms. The holder distribution is live too - top wallet holds 2,800 FGRD, and it fans out from there. You can see every single holder address on the explorer right now. Public equity. Fully onchain. Verifiable by anyone with a browser. FGRD ≠ xStocks Plenty of projects have "tokenized equities." Most of them wrap existing DTCC-settled shares in a blockchain token. A receipt sitting on top of legacy rails. FGRD is the equity. Natively issued on Provenance. No wrapper. No custodian holding the "real" shares somewhere else. No DTCC. SEC-registered. FINRA/SIPC member ATS. Convertible 1:1 to Nasdaq-listed Class A. The bridge design is what makes this work at scale: → Hold FGRD → convert → sell on Nasdaq → Hold Nasdaq shares → convert → trade 24/7 onchain → Use onchain shares as collateral via Democratized Prime Same equity. Two venues. Two settlement systems. Bridged. Liquidity fragmentation? Solved. The Ladder Update In the last post I mapped the RWA complexity curve: → Treasuries (BUIDL: @BlackRock / @Securitize) ✅ → Credit (ACRED : Apollo / @Securitize) ✅ → Equities (FGRD : @Figure / Provenance) ✅ ← NEW The hardest asset class on the ladder. Real-time price discovery, continuous trading, deep liquidity, a century of regulatory plumbing. Done. Goldman-underwritten, SEC-registered public equity settling onchain in a yield-bearing stablecoin. 24/7 trading. DeFi composability from Day One. Three days ago the marker was empty. Today it has 61 holders and 484 transactions. The full stack is live. 🦙🔍

Regulators don’t regulate technology; they regulate outcomes like investor protection, fairness, and market integrity. But when rules focus on preserving legacy market structures, they risk freezing yesterday’s systems in place, and missing new market designs that may better achieve those goals. That’s the premise of my new paper, Fairness by Design: Verifiable Execution in On-Chain Markets. Discussion of tokenized equities and on-chain securities markets often emphasize efficiency gains. This paper asks a different question: what if blockchain’s most important contribution is its ability to make fairness and accountability properties of the system itself, rather than enforced solely after the fact? And how should securities regulation adapt to this fundamentally different architecture? Using order execution as a case study, I argue that the difficulty of enforcing best execution is not primarily a failure of enforcement or compliance culture. It is structural. Fragmented liquidity, conflicted routing incentives, payment for order flow, and latency games make it difficult not only to achieve best execution, but even to know when it has occurred. By contrast, some on-chain markets are experimenting with fairness as infrastructure: execution rules that are constrained, observable, incentive-aligned, and in some cases cryptographically verifiable at the moment of trade. In some of these systems, investors can even directly express preferences among price, speed, atomicity, and privacy, rather than relying on opaque, discretionary routing. The paper does not argue for deregulation or for replacing law with code. Instead, it asks whether verifiable execution guarantees could complement existing securities law as markets move on-chain. In a world where tokenized securities and on-chain settlement are no longer speculative, the question isn’t whether regulators should engage with infrastructure-level guarantees, but whether they can afford not to. This is the first paper in a planned series, Fairness by Design, applying this framework to custody, disclosure, capital formation, and more as part of the broader question, why on-chain capital markets?