Stefan retweetledi

🚨Breaking news: 🦋

@Nasdaq just LOST its Motion to Quash.

Read that again s l o w l y . . .

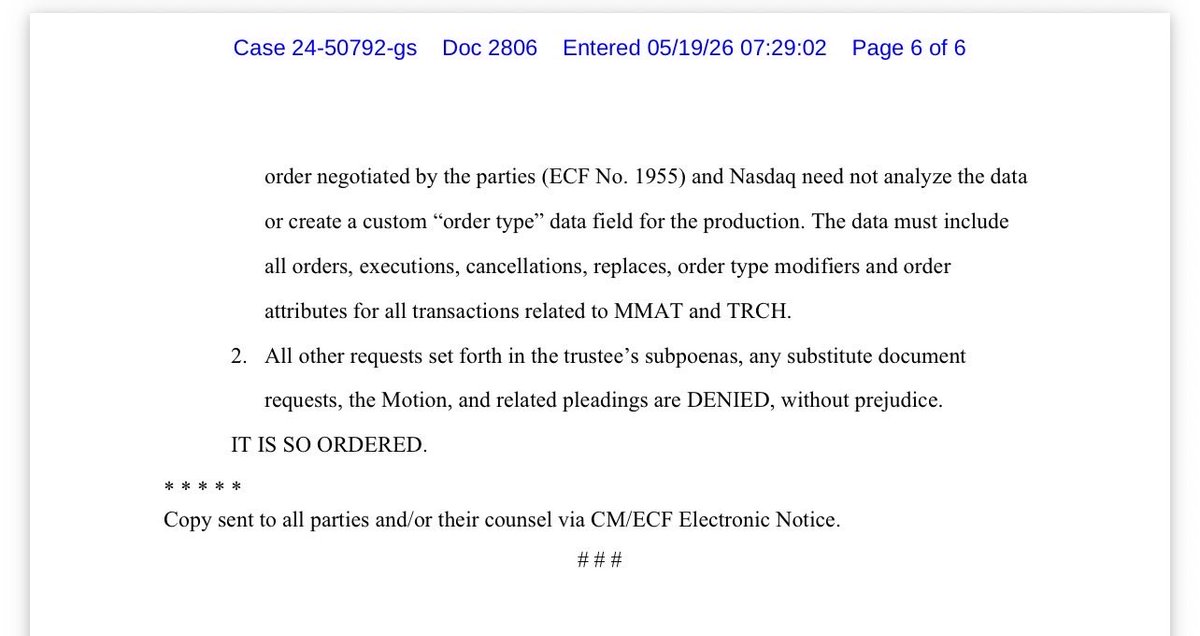

The Bankruptcy Court in Nevada has now ordered Nasdaq to produce extensive $MMAT/TRCH trading data under Rule 2004, including RASH and CORE data, order attributes, cancellations, replaces, executions, and related transaction records covering nearly FOUR YEARS.

The Court was NOT persuaded by the ‘undue burden’ argument, noting that producing ~15GB of spreadsheet data is not exactly impossible for… Nasdaq. (One $10 usb stick)

Even more important, the Court explicitly recognized the Trustee’s AUTHORITY to investigate whether wrongdoing occurred on behalf of the estate, including potential claims tied to stock trading activity.

Translation:

This investigation is very much ALIVE.

For months, some people mocked and undermined the Trustee’s efforts, claimed discovery would never happen, and acted like every subpoena didn’t get served initially and that it would be crushed before daylight. Instead, the wall keeps cracking.

FINRA discovery.

Now Nasdaq discovery.

And the Court explicitly referenced separate pending motions involving Citadel, Virtu, and Anson.

Interesting times ahead.

Turns out Rule 2004 is not just a decorative suggestion.

To the Trustee and legal teams, incredible respect.

It takes courage to walk into rooms filled with institutions that have virtually unlimited resources and say:

‘Produce the data’

And to the echo chambers already warming up their spin machines tonight…

You may want to read the actual order first. 🤝

Blessings to all.

English