John C. Maxwell, III retweetledi

John C. Maxwell, III

46.7K posts

John C. Maxwell, III

@maxjcm

Investor #AI #Fintech, Father, Speaker, Author https://t.co/lCPpakQUba…

Katılım Haziran 2011

5.7K Takip Edilen10.2K Takipçiler

John C. Maxwell, III retweetledi

John C. Maxwell, III retweetledi

Investor demand for downside protection is plummeting:

The average 3-month put-to-call skew of S&P 500 single stocks is down to 0.04, the 4th-lowest reading over the last 20 years.

This measures how much more investors are paying for downside protection via put options than for upside exposure through call options.

The lower the reading, the less investors are paying to protect themselves against a market decline.

The average 3-month put-to-call skew has fallen -75% since March, posting the sharpest drop since April-May 2025.

This metric is even lower than during the 2021 meme stock frenzy.

Investors are no longer thinking about downside risk.

English

John C. Maxwell, III retweetledi

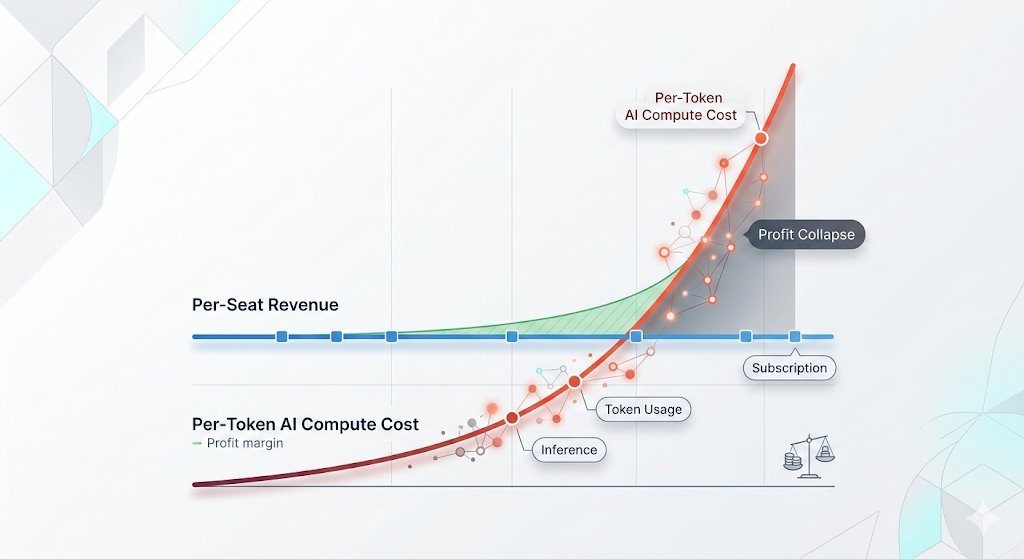

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

English

John C. Maxwell, III retweetledi

Keir Starmer does NOT want the World to see how badly British Patriots want their country back

Would be a shame if it went viral on 𝕏

English

John C. Maxwell, III retweetledi

Americans are defaulting on their student loan debt at a record pace:

Delinquent federal student loan debt jumped +$12.2 billion in Q1 2026, to $171.4 billion, an all-time high.

This has officially surpassed the $166.8 billion peak recorded in Q4 2019.

At the same time, the proportion of seriously delinquent loans rose +0.7 percentage points, to 10.3%, the highest since Q1 2020.

This comes as 2.6 million borrowers defaulted in Q1 2026, followed by ~1.0 million in Q4 2025.

The average borrower entering default is now nearly 40 years old, up from 36.4 before the 2020 pandemic.

The US student loan crisis is intensifying.

English

John C. Maxwell, III retweetledi

Wall Street Wins, Main Street Defaults

“…the Federal Reserve Bank of New York (FRBNY) published new data showing that the share of Americans behind on a range of household consumer debts reached all-time highs in the first quarter of 2026.

As the nation hurdles toward an historical record of $19 trillion in total household debt,

Americans saw the highest rates of auto loan delinquency that FRBNY has ever recorded,

rates of credit card delinquency near those last seen at the height of the 2008 financial crisis,

and student loan delinquency at its worst since before the COVID-era payment pause….”

- @BorrowerJustice

English

English

John C. Maxwell, III retweetledi

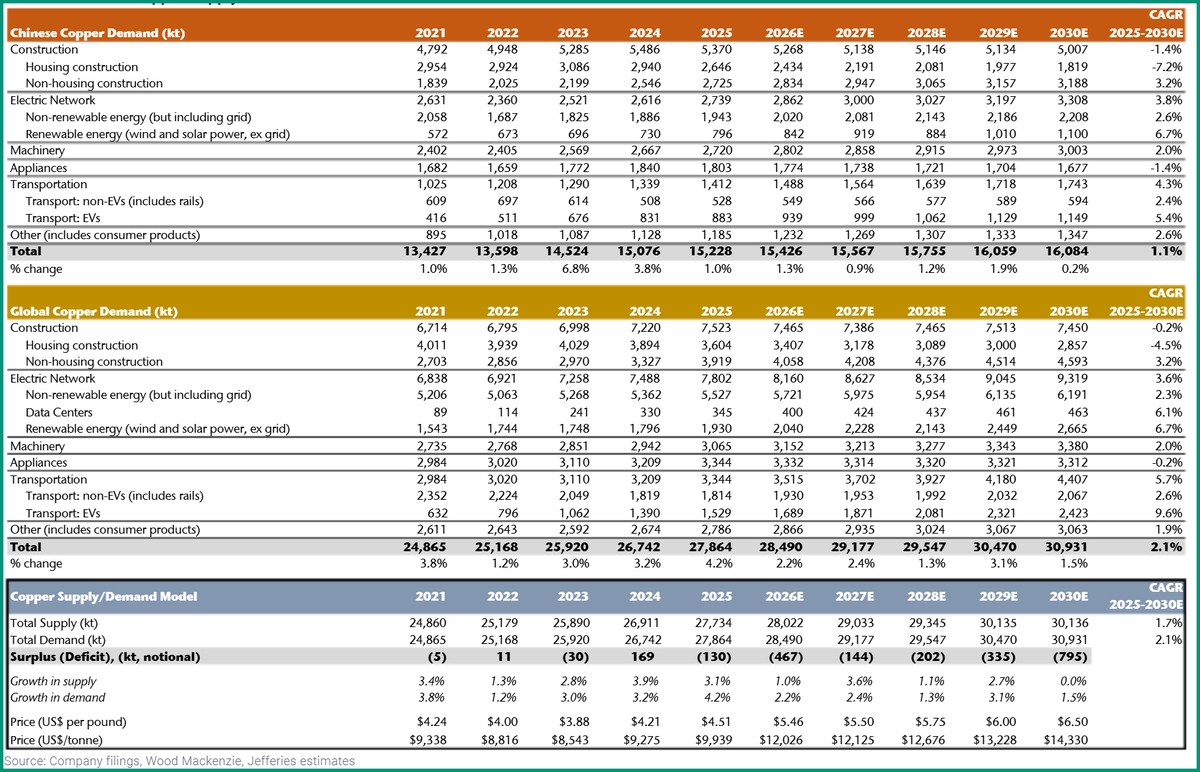

Global Copper Supply-Demand Model

Copper Supply and Demand Outlook

The copper market is expected to enter a period of growing deficits due to significant supply constraints and increasing global demand.

Jefferies' supply and demand model forecasts that total global copper demand will grow at a CAGR of 2.1% from 2025 to 2030E, reaching 30,931 kt by 2030, while total supply is projected to grow at a slower CAGR of 1.7%, reaching 30,136 kt in the same period.

This imbalance is expected to result in a widening deficit, with a notional deficit of (795 kt) projected by 2030E.

English

John C. Maxwell, III retweetledi

The large private credit fund that marked its NAV down from 100 to 81 in January just marked it down again, now to 77.

Are all loans down 23% YTD, or are half the loans down 46%, or are one quarter of the loans down 92%?

Which is worse?

English

John C. Maxwell, III retweetledi

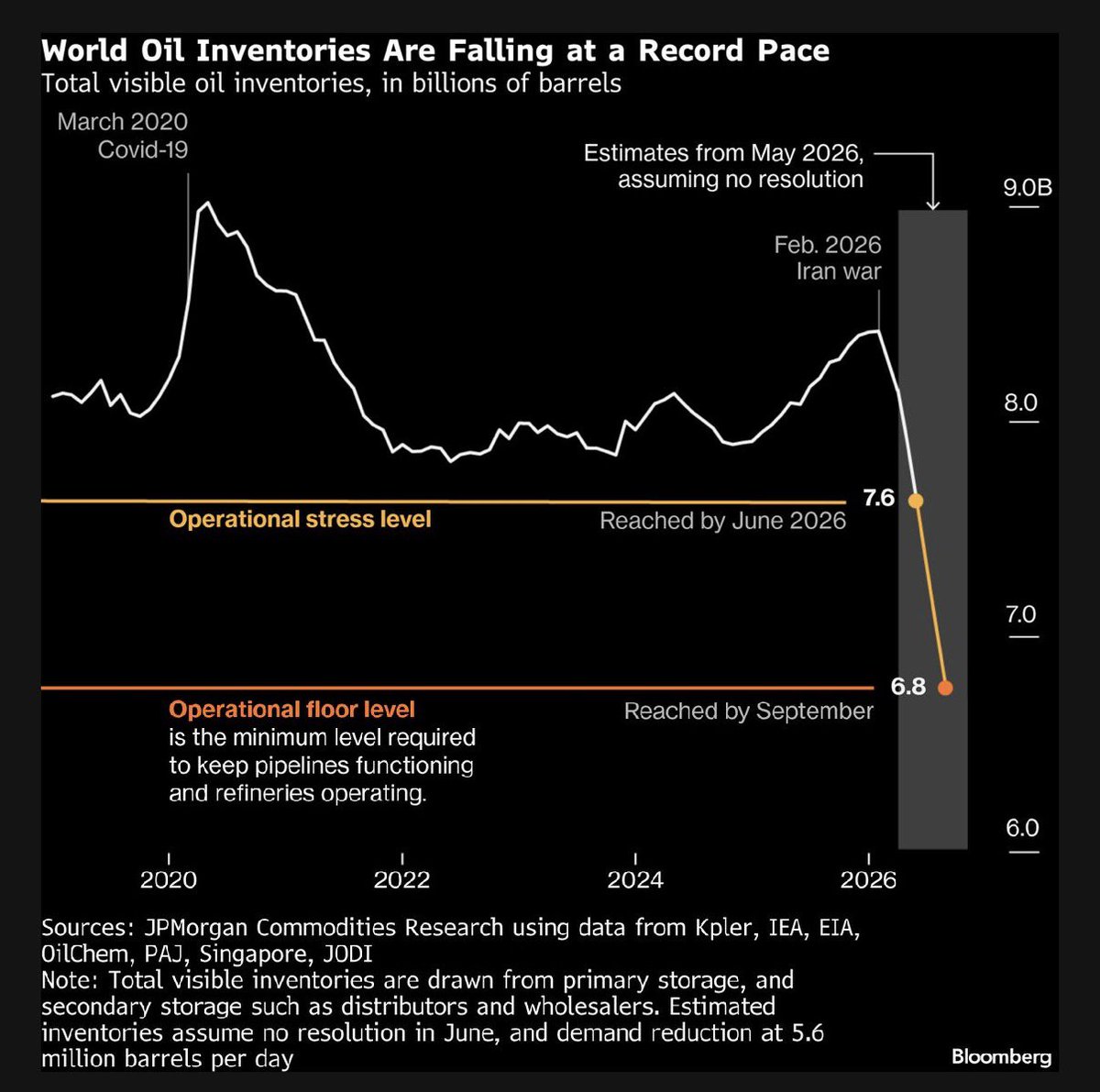

Bloomberg:

“The world has burned through oilinventories at a record speed as the Iran war throttles flows from the Persian Gulf…

The rapidly shrinking stockpiles mean that the risk of even more extreme price spikes and shortages is getting ever-closer, leaving governments and industries with fewer options to cushion the impact of the loss of more than a billion barrels of supply, two months into the near-closure of the Strait of Hormuz.”

#economy #oil #markets #middleeastwar

English

John C. Maxwell, III retweetledi

John C. Maxwell, III retweetledi

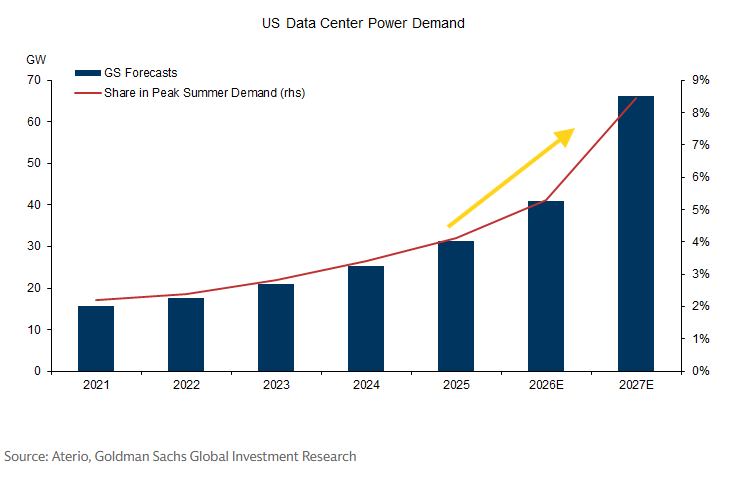

Goldman: Even after adjusting for potential delays and cancellations... we expect US data center power demand to more than triple from 31 GW in 2025 to 66 GW in 2027...

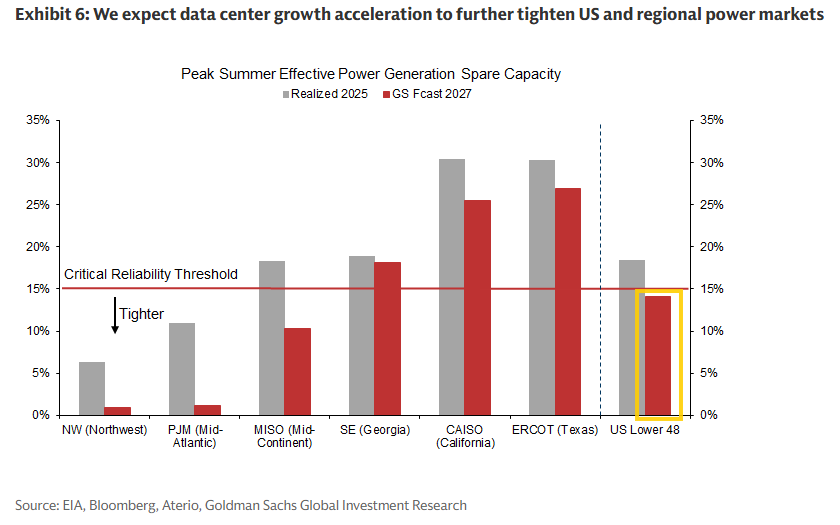

Consequently, we expect this acceleration in data center power demand growth to further tighten US power markets, which we estimate are already critically tight in some regions (Exhibit 6). At the national level, we forecast the share of US data centers in total peak summer power demand to increase from 4.1% in 2025 to 5.3% in 2026 and 8.5% in 2027, leading to incremental tightness in the US power market..

We see increasing risks that [some] markets may have to turn some future data centers away and recommend hedging the upside risks to local power prices.

English

John C. Maxwell, III retweetledi

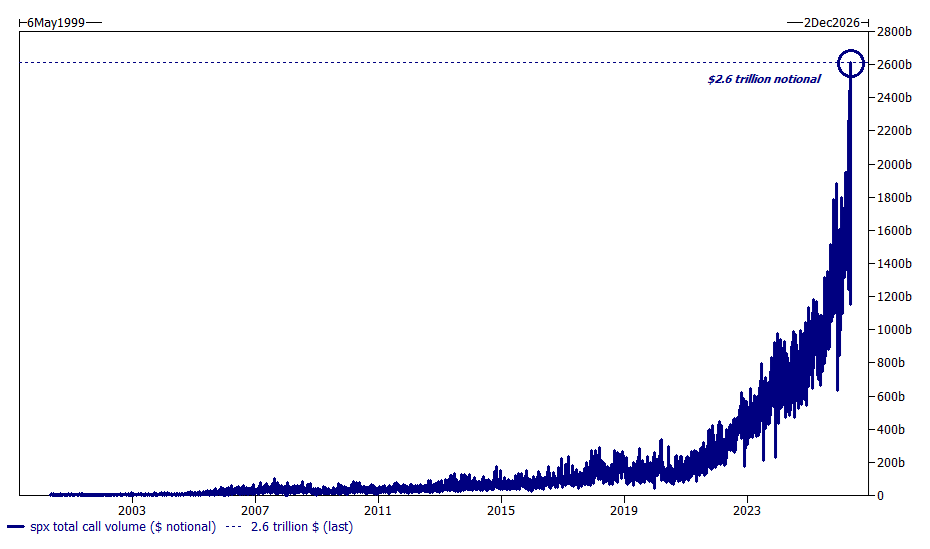

The market just did something it has literally NEVER done before.

The S&P 500 traded $2.6 trillion in call options yesterday.

The highest single day call volume in market history.

When traders buy massive amounts of calls, the market makers selling those calls are forced to hedge by buying the underlying stocks.

That buying pushes prices higher.

Higher prices force more hedging.

More hedging pushes prices higher again.

This is called a gamma squeeze.

It works incredibly well on the way up.

It’s brutal on the way down.

The same loop that drove the S&P higher every day reverses with the same force when the calls expire or the trades unwind.

We’re no longer watching investors price in earnings or growth.

We’re watching options flow drag the largest index in the world.

The question is not if it unwinds, the question is when.

you want to know which stocks we’re buying next, turn on notifications this is VERY important.

Many people will wish they followed us sooner.

The Assembly@InTheAssembly

🚨 Something very unusual just happened. Someone purchased an insane amount of VIX calls. In other words, a big player is betting the market will crash soon and he's doing it with a lot of money. Nobody drops millions on VIX calls unless they know something we don’t. VIX calls only pay off when volatility explodes, which almost always means stocks are getting smoked. The last time the VIX was sitting this calm before getting blown up was early April 2025. 8 trading days later, the VIX exploded from under 17 to over 60. The S&P 500 had one of its worst 2-day drops since the 1987 crash. Trillions in market cap wiped out. We will keep watching. When we make a new move in the market, we will let you know. Turn on notifications so you don’t miss our alerts, this is extremely important. Many people will wish they followed us sooner.

English

John C. Maxwell, III retweetledi

Most people look at the oil price.

The forward curve already told you everything weeks ago

A quick primer first.

When the contract trades BELOW spot, that's backwardation.

The market is saying: the commodity today is worth more than the commodity later.

It signals tight supply, low inventories, or acute stress in the physical market.

When backwardation appears in crude, it usually means one of 3 things:

Inventories are falling fast

Supply is disrupted

Buyers are paying a premium to secure barrels now

All 3 now are currently true.

Since the Iran war began, Brent has been in deep backwardation.

The Strait of Hormuz disruption removed 20% of global seaborne oil from normal routing overnight.

Buyers scrambling for non-Gulf barrels pushed spot prices up sharply while deferred contracts stayed lower, pricing in an eventual resolution.

That spread IS the market's fear, quantified.

There's also a roll yield implication.

In backwardation, rolling a long position earns the roll you sell the more expensive expiring contract and buy the cheaper next one.

It's one reason commodity funds have outperformed during the war period beyond just the spot price move.

Now watch what happens to the curve if the Iran MoU gets signed.

Spot premiums compress.

The curve flattens or flips toward contango.

That move will show up in the forward curve before it shows up in headlines.

The curve has already voted.

The question is what it votes next.

English

John C. Maxwell, III retweetledi

The base case for US Oil Production in the EIA Annual Outlook is a 4 year plateau and then declining. #OOTT

EIA@EIAgov

English

John C. Maxwell, III retweetledi

‼️Big Tech cash is disappearing at a RAPID PACE:

Combined free cash flow across Microsoft, Alphabet, Amazon, Meta, and Oracle is projected to FALL more than -70%, to ~$100 billion, by the end of 2026.

This figure peaked at ~$250 billion in early 2024, even as trailing net income continues surging toward a record ~$450 billion.

This comes as AI capital expenditure is consuming nearly every dollar, with the combined 2026 CapEx expected to surpass $715 billion.

In simple terms, these companies are reporting record profits on paper while simultaneously running out of actual cash, forcing them to issue a projected $175 billion in new debt in 2026 alone, more than 6 times the pre-AI cycle average, according to BofA.

When earnings and cash flow move in opposite directions this aggressively, equity valuations built on earnings alone become extremely fragile.

English

John C. Maxwell, III retweetledi

John C. Maxwell, III retweetledi

$500M Loss as JPMorgan Led Group Is Reportedly Stuck With Full $5.3B Qualtrics Debt

Bloomberg reports JPMorgan and banks are stuck holding the full $5.3 billion in risky debt for Qualtrics’ acquisition after investors bailed. AI fears hammered software deals.

They’re now marking it down and staring at a $500 million paper loss.

English

John C. Maxwell, III retweetledi

“People Are Going to Lose Money Here” - Gundlach Warns on Semi-Liquid Private Credit

“…The products have been “kept opaque and not granularly described,” he said.

“That’s why everybody wants their money back: They’re starting to realize they might be the bag-holder.”

Gundlach took issue specifically with private credit firms calling their funds “semi-liquid” in nature.

“Semi-liquid is kind of a diabolical name,” Gundlach said.

“Half the time it’s liquid.

It’s liquid when you don’t want your money, and it’s illiquid when you do want your money.”…”

English