mahesh

248 posts

mahesh

@mchander110

Civil Engineer having expertise in contract management in construction industry| Value investing learner|

Mumbai Katılım Aralık 2015

106 Takip Edilen37 Takipçiler

@gurjota No body can predict what is going to happen in future.Any guidance is assessment only based on past data. Retirement planning has to be a long term and data shared by you shows that for a period more than 5 years,returns are between 10 to 12 % which is inline with guidance.

English

If your financial advisor told you Nifty gives you 12% CAGR, they lied to you.

If your retirement planning is based on Nifty giving 12% CAGR, you're in for a rude shock.

Returns in next 15-20 years are likely to be same or lower than the past.

Plan wisely.

English

@BaluGorade I think he is contradicting himself. The idea of maximum returns from max uncertainty he admits that he got from a book on investing. Reading definitely helps to streamline thought process to tackle various issues and take decisions.

English

Ridham Desai says reading books is a waste of time.

Personally, I have gained a lot from reading.

Surprising.

x.com/NDTVProfitIndi…

English

@InvestorOfJAMMU PPFAS entered NH some where in Dec 24 and price was 1200 to 1300. Highest was in June 25 around 2200 .pl check .

English

The day Parag Parikh Flexicap fund entered Narayana Hrudalaya, the stock made its top. But never averaged it.

Out of fashion now. Few months back, it was commanding 60 PE.

English

@gurjota There is no point in linking quality of life with any monetary figure of 8 to 10 Cr. One can have a goo quality of life with a small net worth. On the contrary a person with high net worth May not. One has to align his thought process for living a happy and peaceful long life .

English

After 8-10 crore, your own home and a nice car, there is not much difference in the quality of life between you and billionaire investors like RK Damani.

Time is the currency of life. Money is not.

Both of you have limited amount of time on earth; infact you may have twice or more time than RK Damani, so you are richer than him.

Dal roti is dal roti whether a billionaire eats or you do.

Become financially independent, which is around 8-10cr.

Have good food. Workout. Sleep well.

Meet your parents and friends.

That’s all there is to life.

Greed has no end.

Sooner you figure this out, happier you will be.

English

Other than Parag Parikh Flexi Cap Fund,

Which fund would you hold for the next 10 years?

English

@unseenvalue Very insightful as always. You are doing a great service to the investor community. This is definitely going to do gene editing as you have stated repeatedly in presentations on the Substack.

English

#LaurusLabs, at today’s not-so-cheap valuations and hovering near its all-time highs, is not a HOLD if your view is just 3 months. But stretch that view to 3 years, and it still might be.

This gap comes down to time. As Howard Marks and Nassim Taleb remind us, risk and value shift with the clock. What feels expensive and fragile in the short run can turn reasonable once time allows the business to prove itself.

In 'Fooled by Randomness', Taleb tells a story about a retired dentist who is a skilled investor. The dentist expects to earn about 15% more than safe government bonds each year. But he checks his portfolio many times a day. This habit causes stress because, in the short term, prices move almost randomly. Taleb calls this “noise”, which simply means meaningless fluctuations that do not reflect real value.

Over very short periods, like minutes or days, the chance of seeing a gain is barely above 50%. This means that over three months, price movements are driven mostly by luck and maybe Q4 FY26 numbers or, rather, the interpretation of those. If a stock is already “not-so-cheap”, its price reflects a lot of optimism. There is little room for disappointment. Even a small negative surprise can push the price down. It's always albout the rate of change relative to the asking run-rate (valuations)

In 'Most Important Thing', Marks explains that risk often comes from paying too high a price. When you buy an expensive stock, you have almost no “margin for error”. This simply means you have little room to be wrong and still be okay. In the short term, bad luck or shifting sentiment can cause sharp falls. He also points out that being early can feel the same as being wrong, especially over short periods.

Taleb offers another example in 'Fooled by Randomness'. He describes the idea of building a ski resort in Miami. Imagine a rare blizzard hits, and the resort makes a huge profit in its first year. That success does not make it a good decision. It was simply luck. In the same way, making money on an expensive stock over 3 months may just mean you were lucky, not right.

Things look different over longer periods. As time passes, real business performance begins to matter more than daily price swings. Taleb notes that over a year, the odds of seeing gains improve greatly. Over 3 years, the company’s actual progress has a much better chance to show through the noise. What the business earns and builds starts to matter more than short-term sentiment.

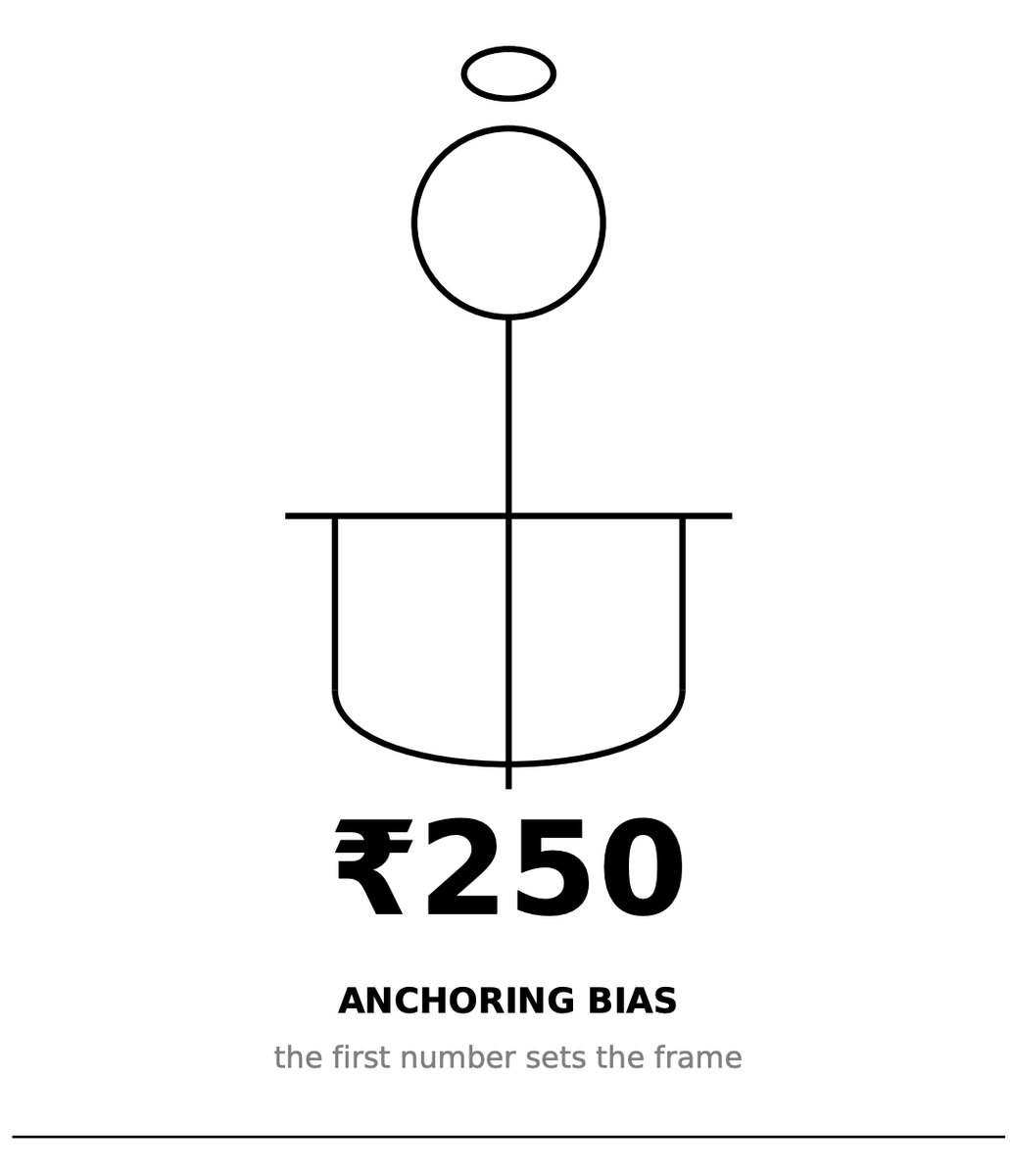

Back in 2023, I was one of the few bullish voices on Laurus. Talk is cheap, so I backed that view with my own money. Sell ratings were common at the time, and many were anchored to targets around 250, which weighed heavily on sentiment.

Marks explains that while prices can drift in the short run, terminal value pulls them back over time. Terminal value is simply what a business is truly worth based on what it can earn and build.

For Laurus Labs, the CDMO business is that anchor. Over the next five to seven years, this segment alone could cross 10,000 Cr. in annual sales. Then, post-2033, the precision fermentation and bio-engine should be all guns blazing.

If a company grows well, it can “grow into” a high MCap. This is why a stock that looks expensive today may still work out over a few years. Over 3 years, a strong business may justify a high starting price. Over 3 months, you are mostly exposed to chance.

Taleb compares short-term risk to a version of Russian roulette with many chambers. You might avoid losses several times, but the risk is always there. Without a margin of safety, a sudden drop can happen at any time. This is why short-term investing in expensive stocks can feel unpredictable and fragile.

In the end, time changes the nature of the bet. Over 3 months, randomness dominates, and a high price leaves little protection. Over 3 years, business performance has time to come through, and value can catch up with price. The same stock can look risky or reasonable depending on how long you plan to hold it.

Laurus Labs is our core family holding, and none of this is an investment recommendation.

English

@BaluGorade If one can afford , must buy otherwise life May depreciate faster

English

Cars depreciate. Life does too.

If you can afford it, buy it. Enjoy the ride. Protect your family. 👍

English

@BaluGorade Important learning for me from recent fall in the stock market- always have some cash to take advantage of such events leading to asymmetric earning in the long run which can boost the overall portfolio performance. This may be a better strategy than being fully invested .

English

Cash holdings in popular funds:

Old Bridge Focused = 17%

Parag Parikh Flexi Cap = 19%

Bandhan Small Cap = 12%

HDFC Mid Cap = 8%

HDFC Flexi Cap = 4%

Motilal Oswal Midcap = 4%

Cash is also a position. 👀

Source - Value research

English

@BaluGorade @EquityDeliveryX Raunak Onkar also deserves credit being head of research at PPFAS

English

Chirag Setalvad, S Naren and Rajeev Thakkar are the gems in our equity market

Balu Gorade@BaluGorade

March portfolio is out. They are still holding 19% cash. No major deployment even during the recent correction. Rajeev Thakkar ji - The nation wants to know, when will the cash be deployed? 👀

English

@BaluGorade The fund has made substantial purchases in existing stocks. The cash percentage seems to be high because of the reduction in AUM due to fall in prices of stocks

English

March portfolio is out.

They are still holding 19% cash.

No major deployment even during the recent correction.

Rajeev Thakkar ji -

The nation wants to know, when will the cash be deployed? 👀

English

@BaluGorade I am doing SIP in PPFAS flexi cap for the last 8 years. As on date xirr of 17%. It has fallen only around 6 % in the last one month. So deserves to be one of the best choice for investment.

English

- Parag Parikh Flexi Cap

- HDFC Flexi Cap

- Bandhan Small Cap

These three continue to be the most bought funds on the Kuvera platform.

Meanwhile, investors are writing off Quant and Motilal.

English

@raghavwadhwa PPFAS has not bought Aptus value housing finance. Pl chech

English

✨Parag Parikh Flexi Cap in 2023 vs 2026.

Same fund. Same fund manager. Completely different portfolio.

India's largest actively managed mutual fund quietly made one of the biggest strategic pivots I've seen — and most investors holding it have no idea what changed.

I went through 3 years of monthly disclosures. Here's what Mr. Rajeev Thakkar actually did:

𝗧𝗵𝗲 𝗕𝗶𝗴 𝗡𝘂𝗺𝗯𝗲𝗿𝘀

AUM in early 2023: ~₹30,000 Cr AUM in March 2026: ~₹1,34,000 Cr That's 4.5x in 3 years.

But the portfolio didn't just grow. It shapeshifted.

👉𝗦𝗵𝗶𝗳𝘁 #𝟭: 𝗨𝗦 𝗧𝗲𝗰𝗵 𝗗𝗲-𝗥𝗶𝘀𝗸𝗶𝗻𝗴

2023: Foreign equity was ~17-18% of portfolio

→ Alphabet ~5%, Microsoft ~5%, Amazon ~4%, Meta ~4%

→ US tech was the defining identity of this fund

2026: Foreign equity dropped to ~10.5%

→ Alphabet ~4%, Microsoft ~2.7%, Amazon ~2.4%, Meta ~2.7%

→ Still there, but no longer the star of the show

They didn't panic-sell. They just stopped adding. As AUM grew 4.5x, the US allocation was diluted by design. Quiet, deliberate rebalancing.

👉𝗦𝗵𝗶𝗳𝘁 #𝟮: 𝗟𝗼𝗮𝗱𝗶𝗻𝗴 𝗨𝗽 𝗼𝗻 "𝗕𝗼𝗿𝗶𝗻𝗴 𝗜𝗻𝗱𝗶𝗮"

This is where it gets really interesting.

The stocks PPFAS has been aggressively buying are not what fintwit would call exciting:

→ Coal India — high dividend, government cashflow machine

→ Power Grid Corporation — ₹6.92% of portfolio, massive accumulation

→ ITC — grew from minor position to 5%+, added crores of shares every single month through 2025

→ HDFC Bank — now the #1 holding at 7.73%

→ ICICI Bank, Kotak Bank — steadily increased

These are cash-rich, dividend-paying, low-PE giants. Not the high-growth darlings that dominate social media watchlists.

👉𝗦𝗵𝗶𝗳𝘁 #𝟯: 𝗧𝗵𝗲 𝗖𝗮𝘀𝗵 𝗣𝗶𝗹𝗲

2023: Cash allocation ~12-13% 2026: Cash allocation ~24-25%

Read that again. India's largest active equity fund is sitting on roughly ₹33,000 crore in cash.

That's not laziness. That's a statement. Thakkar is telling you: "I can't find enough cheap stocks to deploy this money into."

When a value investor hoards cash, it means they think the market is expensive. When they do it while simultaneously buying Coal India and Power Grid, it means they're preparing for a downturn by loading defensive, dividend-heavy positions.

👉𝗦𝗵𝗶𝗳𝘁 #𝟰: 𝗧𝗵𝗲 𝗥𝗲𝗰𝗲𝗻𝘁 𝗠𝗼𝘃𝗲𝘀 — 𝗚𝗮𝘀 & 𝗛𝗼𝘂𝘀𝗶𝗻𝗴 𝗙𝗶𝗻𝗮𝗻𝗰𝗲

February 2026: Added Mahanagar Gas + Indraprastha Gas (city gas distribution)

September 2025: Added Aptus Value Housing Finance

November 2025: Added Indus Towers + TCS

Gas distribution + affordable housing + telecom infrastructure.

These aren't glamour plays. They're structural India bets — regulated businesses with predictable cashflows.

Meanwhile, exited: MCX, IPCA Labs, ITC Hotels, Himadri Speciality, HP Adhesives, Laxmi Dental

Pattern? Dumped the cyclical/speculative names. Loaded the boring compounders.

👉𝗧𝗵𝗲 𝗛𝗶𝗱𝗱𝗲𝗻 𝗦𝗶𝗴𝗻𝗮𝗹

Here's the number that tells you everything:

PPFAS portfolio PE: 17.51

Flexi cap category average PE: 27.28

PPFAS is running a portfolio that's 36% cheaper than its own category. While the rest of the market chases momentum, they are buying yield.

👉𝗧𝗵𝗲 𝗣𝗮𝘁𝘁𝗲𝗿𝗻 𝗕𝗲𝗵𝗶𝗻𝗱 𝗜𝘁

2023 PPFAS = "Global tech + Indian quality"

2026 PPFAS = "Domestic cash cows + massive cash buffer"

The fund hasn't changed its philosophy. It's still buying businesses below intrinsic value with strong cashflows.

What changed is WHERE that value exists.

In 2023, it was in beaten-down US tech (post-2022 crash).

In 2026, it's in boring Indian dividend aristocrats that nobody on Twitter wants to talk about.

Mr. Thakkar and Team aren't predicting a crash. They're positioning for a world where returns come from dividends and compounding — not from PE re-rating.

That's either very smart or very early. Usually, with Rajeev Thakkar, it's both.

English

@porinju @RajeevThakkar @PPFAS That’s the strategy and thought process of PPFAS . They don’t only preach and execute but live also. Wow… great and creative display. Fortunate to be associated with the fund for the last 9 years.

English

@unseenvalue Happy Teachers Day Sajal sir. Learning a lot from you.🙏

English

Thanks a lot, Venu — very thoughtful of you. Your claims may be valid, but it does suggest a rather demanding P/S, with expectations of a higher "run rate" already built in. I’ll try to frame, from a different perspective, why this one stood out among the Metals. It's in team!

SK@Venu1602

@unseenvalue My Guru. My Pride. Happy Teachers Day Sir🙏

English

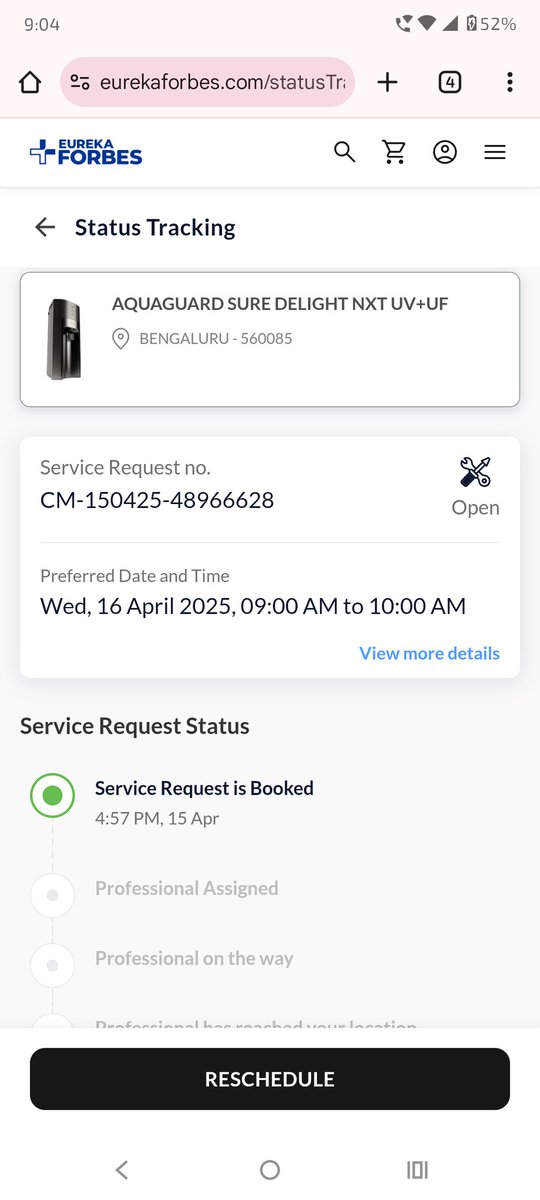

@chutneyji @EurekaForbes Same thing happened in my case. Professional never attended and got the message that complaint attended and closed. Then they sent the message to give feed back . Gave zero. Made a mistake in buying Eureka Forbes Acquaguard@ Eureka Forbes

English

@EurekaForbes when will the professional assigned? It's already 9. AM. When will the technician turn up. We have work to do cannot wait for your guy for while day.

English

"Randomness hai khaas … baaki sab bakwaas" 😃

Should we do a Zoom session on 'threatened' pharma tariffs and extreme uncertainty followed by Q&A?

Pricing? Reasonable!

INR 750 all-inclusive and free for existing paid Substack members.

English

@drmithunraj @unseenvalue That is wonderful.Sharing the speech By Dr Chhava at ISB convocation which will further build confidence of long term investors of LL.

youtu.be/W4AU8csRbM0?fe…

YouTube

English

'Reimagining Laurus labs 2030' by @unseenvalue at Substack.

100 minute session with multiple deep insights. A must listen for all longterm investors of #Laruslabs.

English

@unseenvalue Listened to the presentation. Wonderful work done Mr Sajal.Your way of explaining the concept , numbers and management quality is superb . Learning a lot from your tweets and now thro Substack. God bless you

English

Friends will remember today's presentation on Solara for a very long time. Let the stock do whatever it wants to do. Let it fall more. Let there be more pain. Let doubting Thomases feel complacent about their prediction powers. Santaap frontloaded. Sukh backended.

English

Road constructed by using bio bitumen developed by Praj @15% blending… a new product by Praj

Agarwal

drive.google.com/file/d/1JMwkBW…

English