Oli

118 posts

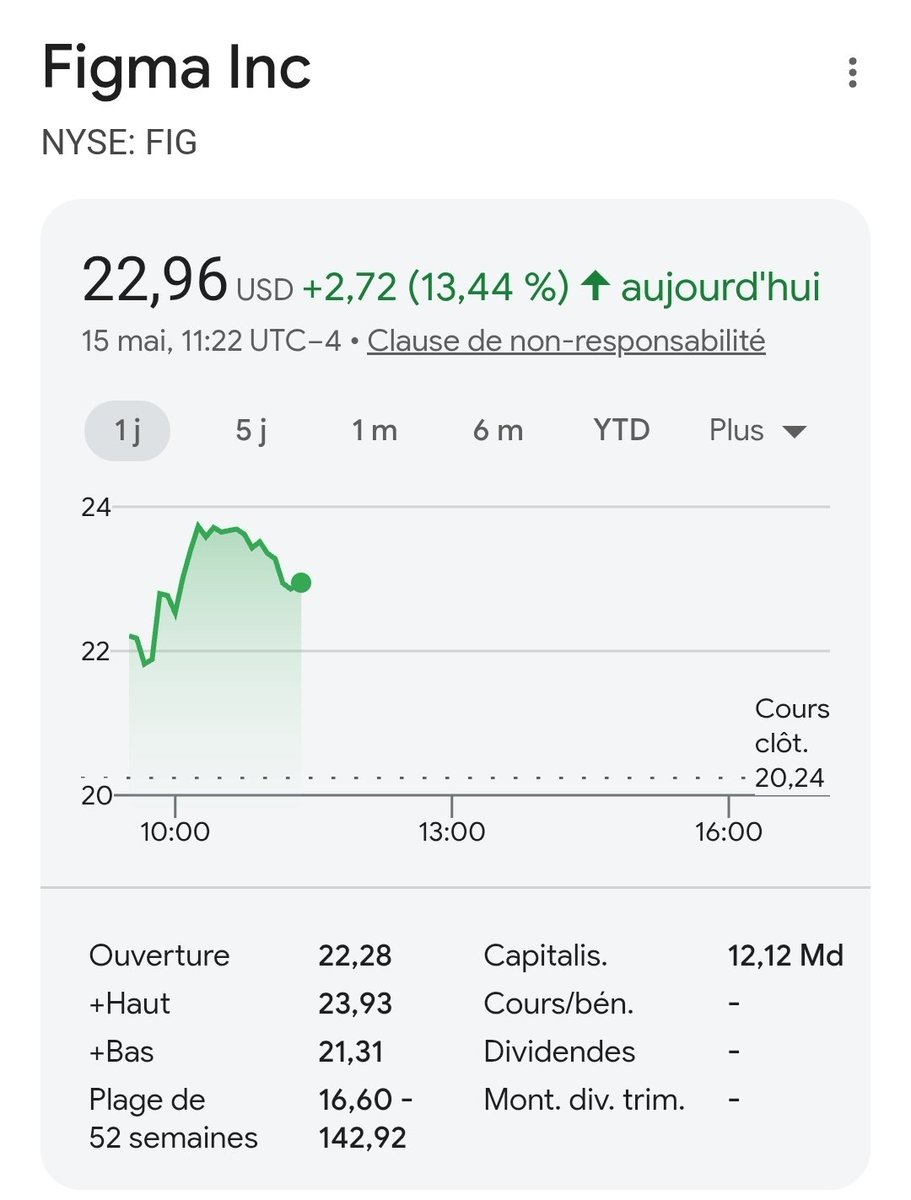

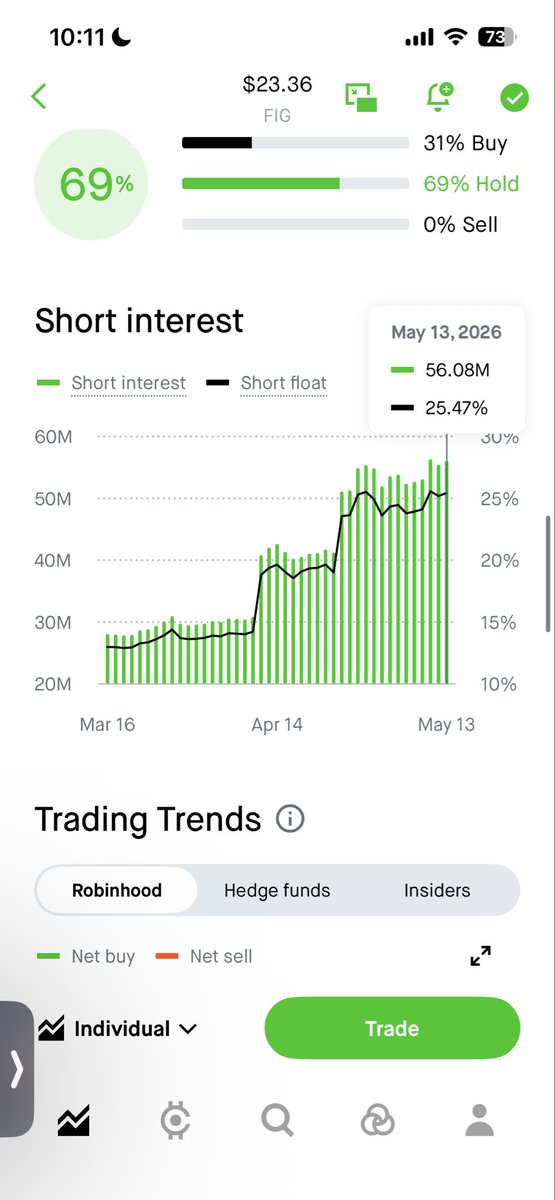

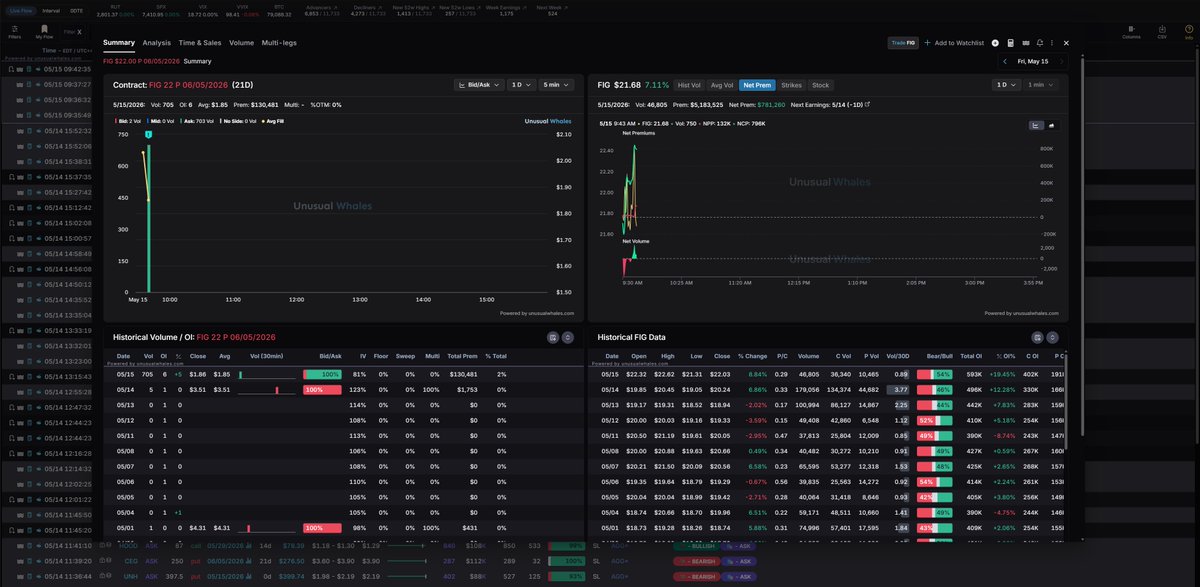

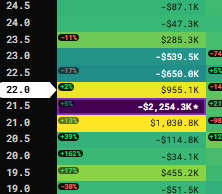

$FIG (Figma) J'ai vu juste. beat massif. Le marché s'est complétement trompé. + 12% en after. 📈 🟢 Revenue : $333M vs $316M attendu. Beat de +5.5%. 🟢 Croissance : +46% YoY. Le marché priçait une décélération. C'est une accélération. On était à +40% au Q4. 🟢 EPS : $0.11 vs $0.06. Beat de +83%. 🟢 Marge opérationnelle : 16%. Le double de la guidance annuelle à 8%. 🟢 NDR : 139%. Chaque client dépense +39% de plus chaque année. Le panier moyen explose. 🟢 FCF margin : 27%. $89M de free cash flow en un trimestre. 🟢 Guidance relevée : +$55M sur le revenue annuel. +$40M sur l'operating income. Comme je l'avais préssenti, le narratif SAASpocalypse disait que l'IA allait tuer Figma. Les chiffres disent l'inverse. L'IA accélère la demande. Les clients adoptent Figma Make massivement. MCP transforme Figma en infrastructure du design AI. Plus l'IA génère de code, plus on a besoin d'un cockpit visuel pour affiner. Figma n'est pas un perdant de l'IA. C'est le Human-In-The-Loop layer. À $20, le marché paye 8x le revenue pour 46% de croissance et 27% de FCF margin. C'est à mon sens un +100% sans problème. Je vend rien sous 40$

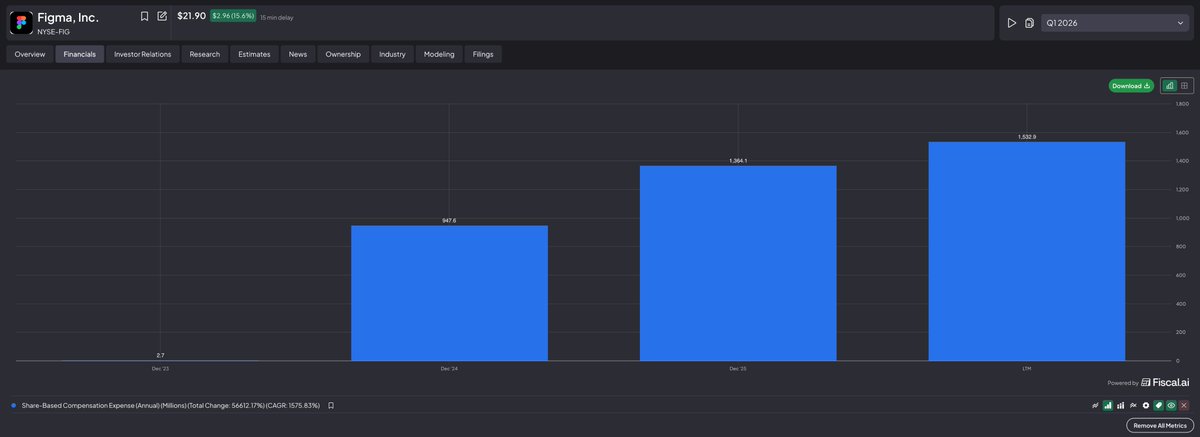

$FIG reports blow out results... with massive revenue growth. This isn't shocking, and I will *not* be buying the rip. 1) Overheads are exploding at least as much as revenue growth. 2) Everyone and their gran is using AI-powered applications to ship this ship that.. and Figma goes somewhere in that supply chain 3) Figma is still early days as a product suite, so it's still in early growth stage (i.e. fast) Share-based comp is obscene and will REMAIN so. The company isn't reporting any net profit and will continue to focus (both in rhetoric and in actual fact) in growth, expanding the value offering, hiring more people etc. Current market cap >$10bln. Q1 revenue: $333mln Profits? None.

$FIG reports blow out results... with massive revenue growth. This isn't shocking, and I will *not* be buying the rip. 1) Overheads are exploding at least as much as revenue growth. 2) Everyone and their gran is using AI-powered applications to ship this ship that.. and Figma goes somewhere in that supply chain 3) Figma is still early days as a product suite, so it's still in early growth stage (i.e. fast) Share-based comp is obscene and will REMAIN so. The company isn't reporting any net profit and will continue to focus (both in rhetoric and in actual fact) in growth, expanding the value offering, hiring more people etc. Current market cap >$10bln. Q1 revenue: $333mln Profits? None.

$FIG