EVV

580 posts

@iononrecourse 20 years from now, theres was a time in 2026 when you can buy large cap MF REITs trading at 6.5-7.0% cap rate and borrow from IBKR in the mid 4% and run it 120-130% gross and just go to the beach.

English

There was a time in the mid '90s when one could buy land in the Atlanta exurbs for less than the net proceeds from selling the timber on that land. The market moved fast and some sellers didn't realize what they had.

Some of those parcels sell for 25k+ per acre now.

I was too focused on another niche (dumb) to join in the fun.

A lot of real estate investing looks obvious in the rear view mirror, but not at the time.

This was one of those that was obvious at the time.

English

看到日本的自杀式汇率干预,感觉美国现在已经站在选择的悬崖边上。贝森特不可能不知道油价继续涨上去的后果是什么:金融系统会面临一场总核爆。如果说只有危机能迫使人们接受变革,那么这句话不仅适用于莫内建立的欧盟,同样适用于彻底变革彼此曾作为战略假想敌的中美关系。

为什么AI半导体和存储带领了广度如此之差又如此巨幅的牛市?现在市场不是看不到危机。是看到了危机会以某种方式被解决,但因为不知道这个方式具体是什么,仍然保持极大的紧张度,始终不见兔子不撒鹰。所以风险溢价居高不下,资金FOMO意愿虽然异常强,却都云集在这些高确定性板块,导致指数涨幅建立在广度异常窄的情况下。

那么为什么加密/软件/中概/私募信贷这些边缘资产看上去在触底呢?可以证明的是,金融末日的场景已经被定价进了这些资产,而现在边际资金所期待的是一场可以大幅降低风险溢价的事件发生,那么也许在这之后就是风险偏好和资金流向的剧烈逆转。

我们等一周,或者不到一周,可能就能知道答案是否如此。

Aelia Capitolina@Areskapitalon

"Les hommes n'acceptent le changement que dans la nécessité et ils ne voient la nécessité que dans la crise."

中文

EVV retweetledi

"I haven't seen a real new idea in trading in at least 15 years."

Tom Costello (@tcoste110) ran money at Tudor, Moore Capital, and Caxton. Built one of the first NLP-driven equity systems in 2003.

20 years managing capital, never had a down year.

"Comparing what a retail trader does to what a quantitative hedge fund does is like comparing driving a bus on the New Jersey Turnpike to winning a Formula One race."

We cover:

- His hot take: no genuinely new trading idea in 15 years — only better people doing the same things faster

- Why everyone in quant finance is a genius — and why that makes you ordinary, not special

- Crypto is "super smart guys cosplaying at finance" — built for retail, which is exactly why it's the easiest money in finance right now

- Why AGI won't beat the hedge fund industry — all the readily-capturable alpha is already captured

- The status trap: why the path that made Paul Tudor Jones a billionaire won't work for the kid trying to copy it in 2026

- His friend the investment banker who'd quit it all to run a 10-employee ambulance supply company worth $150M

- Why excitement is "wildly overbid" in finance — and why wanting an exciting trading job is itself a disqualifier

- The most honest end of the financial industry — and why the media has it exactly backwards

Thanks so much to Tom for coming on Odds on Open!

Highlights:

00:00 Intro

01:18 Building institutional credibility for early-stage managers

03:01 The Pareto distribution of hedge fund returns

04:25 Applying the Unified Field Theory of Finance to fair value

08:14 Trading against human incentives in a deterministic market

13:54 Why allocators don’t steal alpha from prospective PMs

25:16 Evaluating career edge in quantitative finance for 2026

30:48 Paul Tudor Jones and the art of game selection

33:42 Analyzing the economic viability of starting a new fund

35:16 Identifying common retail pitfalls: Mean reversion and arbitrage

38:55 Why there hasn't been a new trading idea in 15 years

50:33 Managing tail risk: Physics vs. deterministic financial distributions

59:10 Career pathing for PMs after a fund blow-up

1:07:53 SBF and FTX: Credibility vs. the "Founder-Genius" archetype

1:13:44 Establishing proof-of-concept through audited multi-year returns

English

EVV retweetledi

A lot of people have observed some ominous parallels between today's market and the dot com bubble.

The biggest difference being valuation.

But I'd point out that valuations were not especially high in 2007 in spite of having bubble-like conditions in the places that it mattered the most.

We didn't have euphoria in the summer of 2007. It was not a stock market mania. And yet we still had a 57% meltdown.

All bull markets and bubbles are different. History doesn't repeat itself, but it does rhyme.

English

EVV retweetledi

EVV retweetledi

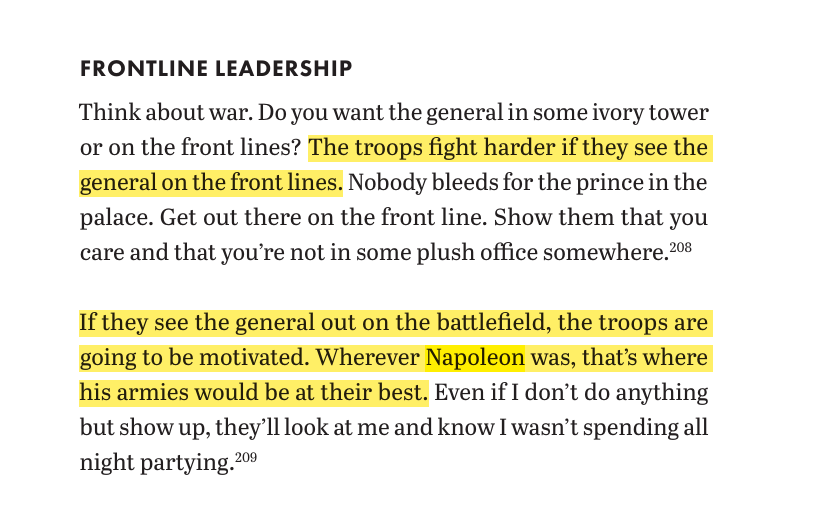

Napoleon's True Genius via @elonmusk

Napoleon's troops followed him into cannon fire because they'd seen him standing in it first.

Nobody bleeds for the prince in the palace.

Great book by @EricJorgenson

h/t @PEoperator

English

@midteensyield True but if Powell would define the oil shock more as a demand shock event than an inflation event, plus what Kevin Warsh said about redefining the standard of inflation, then a monstrous era of monetary easing can be expected.

English

猜测周三的FOMC有可能会是一个转折点:对高油价的认知从主要是通胀效应转化为主要是衰退效应,从1970年代式滞涨过渡到一种类似2020年covid的冲击。叠加Kevin Warsh的表态“用更科学的方法来衡量通胀”,市场会计价一个讲Volcker语言的Burns regime。这就是新的让美联储再次伟大运动。

Aelia Capitolina@Areskapitalon

油价上涨和科技股上涨不是矛盾的信号被市场”暂时忽略了其中一个”,它们是同一个底层regime的两个同时为真的表现。油价上涨推高通胀,通胀跑赢被锚定的名义利率,实际利率下降,被动宽松驱动资金涌入科技股。油价的上涨直接导致了科技股的上涨,它们之间是因果关系而不是矛盾关系。 用量子力学的框架来说,不是”市场在油价利空和AI利好之间选择了后者”,而是”在坍缩发生之前,油价上涨同时是危机和非危机,它的危机属性(银行浮亏扩大)和非危机属性(被动宽松加速)同时存在且同时为真”。市场不是在忽略危险信号,市场是在一个危险信号本身就是上涨动力的叠加态里运行。 通胀不是一个有固定方向性含义的变量,它的含义完全取决于系统处于哪个状态。在坍缩前的状态里通胀等于宽松,在坍缩后的状态里通胀等于紧缩。

中文

EVV retweetledi

Now that Warsh is going to be confirmed. Assuming Powell resigns Governor that day. (as he should). Warsh will vote for a cut in June. Waller, Williams, Miran or someone like him & Bowman make 5 votes for a cut. Only 2 middles have to join the cut.

English

EVV retweetledi

EVV retweetledi

Wow.

The White House just announced that grid infrastructure is essential to national defense.

This includes transformers, transmission lines and conductors, substations, and high-voltage circuit breakers.

Companies working to electrify America will have a big tailwind.

English

EVV retweetledi

Ranked number 12 in the world and tucked in the West Village.

The space is beautiful, the staff is incredibly welcoming, and the coffee is incredible.

Arcane Estate Coffee

37 Cornelia St, New York, NY 10014

English

EVV retweetledi

EVV retweetledi

American stocks had been underperforming the rest of the world for several months. And the very bottom was of this was on February 27th, right before the war started. The US started a war, and since then its stock market has outperformed the rest of the world.

English

EVV retweetledi

Probably the best take I have heard on why there is so much fear around software exposure in private equity and credit because of AI

From David Sacks

"Historically we only had two good exits for software businesses. One was IPO. The other was M&A. Then these big private equity shops came along and gave us a third potential exit. You would sell to them and then they would raise the capital based on one third equity and two third debt. So it was debt financed buyouts.

It is something that has been around in the non technology part of the economy for a long time but was a relatively new entrant in the world of technology. And the reason for that is if you have debt financed a purchase, you need to have very stable cash flows.

Because if you miss and you cant pay your interest on the debt, you will lose all your equity because the debt holders will foreclose.

It was belief for a long time that software did have predictable cash flows, at least for the mature businesses."

English

EVV retweetledi

You don't know how big a fish you are till you try a big pond.

English

EVV retweetledi

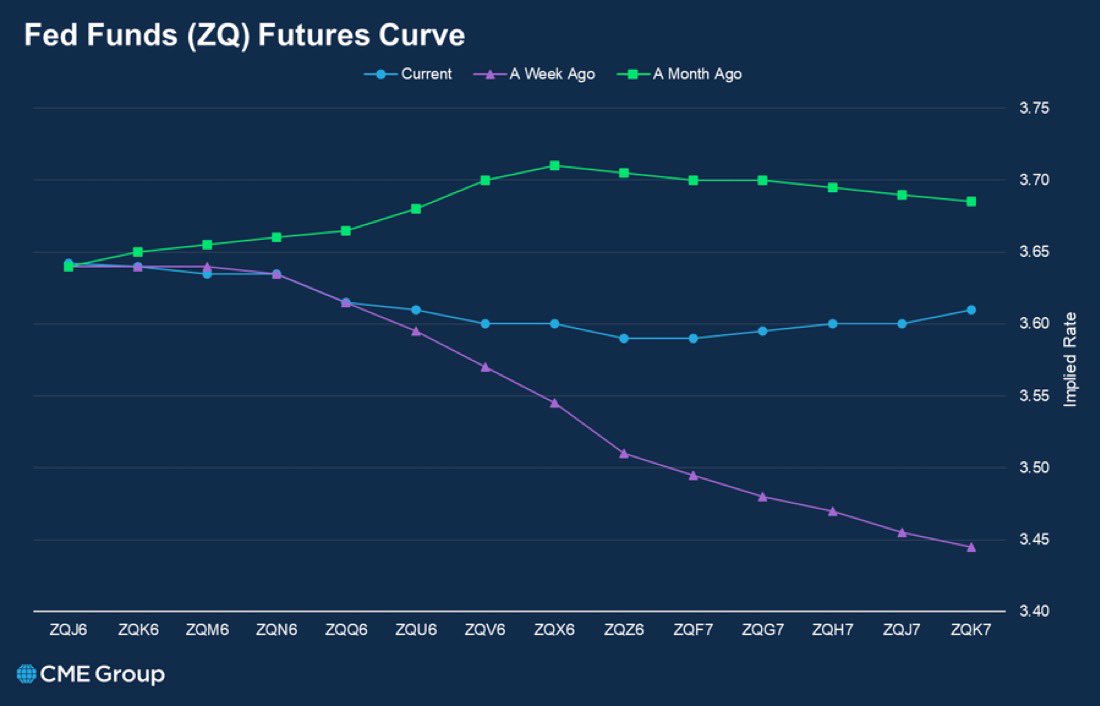

10Y Yield... how long can Bessent hold it below 4.4 before YCC?

English