Sabitlenmiş Tweet

@Jeff

9.8K posts

@Jeff

@moreanabolics

anomalies, dumbbells, JD candidate "I go to the bottom line in everything, and throughout my entire life, I have crossed this bottom line." - Dostoyevsky

Katılım Nisan 2024

1K Takip Edilen583 Takipçiler

@Villaverde4NC @gtconway3d @realDonaldTrump The real misrepresentation here is pretending weakness and talks-without-teeth ever deterred Tehran. They didn't. Dominance might

English

@gtconway3d @realDonaldTrump I'm not sure who advised him, but apparently someone convinced Trump that mutual economic destruction is "deterrence." So much winning.

English

Blockading a blockade is the work of a pure stable genius like no one has ever seen before. Only @realDonaldTrump could have thought of this.

It's like, "You think you can shoot at us? Well, we'll show you—we'll shoot ourselves!!"

We should all have tears in our eyes.

English

@L1569Uptown The hell is ECPI University, there's no law school ...

English

@moreproteinbars Steak is not medium rare...try again, not fit to eat.

English

@marceelias Keep "explaining" what's actually happening, champ. The rest of us will stick with not needing a $5/month decoder ring to spot the pattern.

English

Most legacy media aim to give you both sides of what people are saying about voting rights. Democracy Docket's goal is to explain what's actually happening. Support and subscribe now. bit.ly/4a7l1TR

English

As survivors, we are defined by courage, resilience, and truth.

The stories of Epstein’s survivors are OUR stories too. We share your pain, your frustration, and your pursuit of justice.

The names of co-conspirators in those documents deserve to be revealed, and those who protected Jeffrey Epstein for decades must finally be held accountable.

English

@zerohedge The BTFD generation is apathetic, we're going much lower.

English

MPTA explores cost cutting measures for Silver Line wsoctv.com/news/local/sil…

English

@L1569Uptown @CMPD Imagine, instead of platitudes and self congratulations, she was out shopping for law enforcement drones that could have been at Cotswald in seconds. These people are the most incompetent fools lacking any capacity of leadership.

English

We are so grateful for the Charlotte-Mecklenburg Police Foundation's support as well as all of the businesses and community partners that we got to connect with today at the foundation's spring luncheon. Opportunities like this help us strengthen relationships, share our officers' great work and continue building a safer, more engaged community together.

In 2025 alone, the Police Foundation invested more than $1.6 million in initiatives that directly support our core priorities: reducing violent crime and disorder, strengthening community engagement and improving employee wellness and morale.

@CMPFoundation

English

@HunterOfCheetos If one needs to be told that, they need another hobby.

English

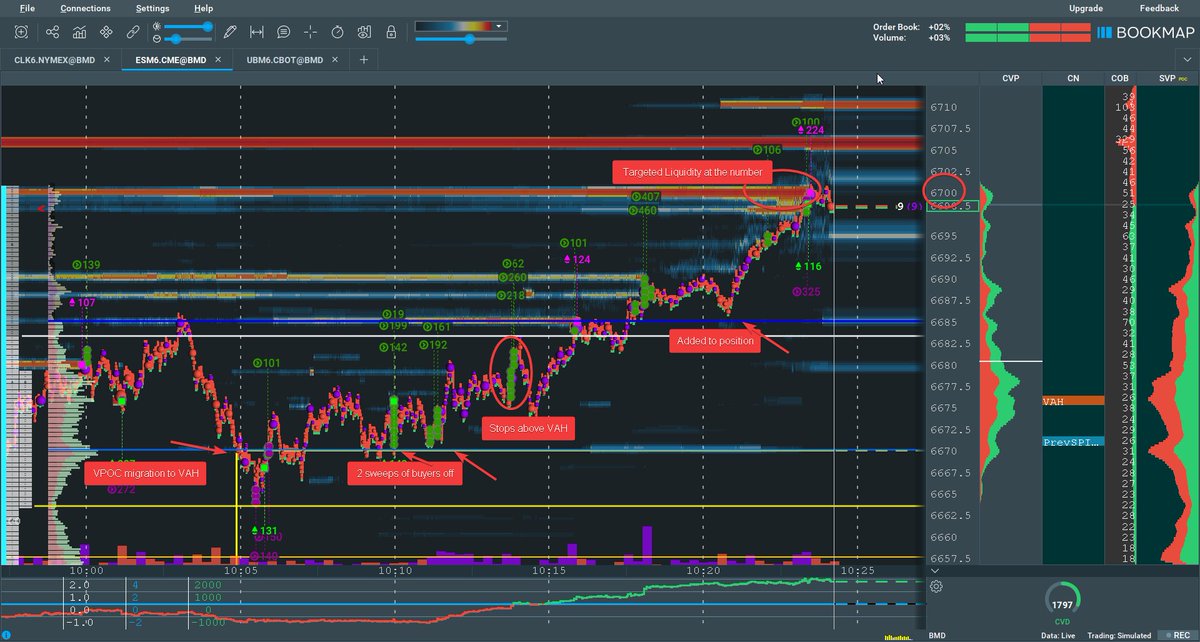

I got four messages today from traders who blew up their accounts.

Always trade with stops people. Know where your getting out before you get into a trade.

English

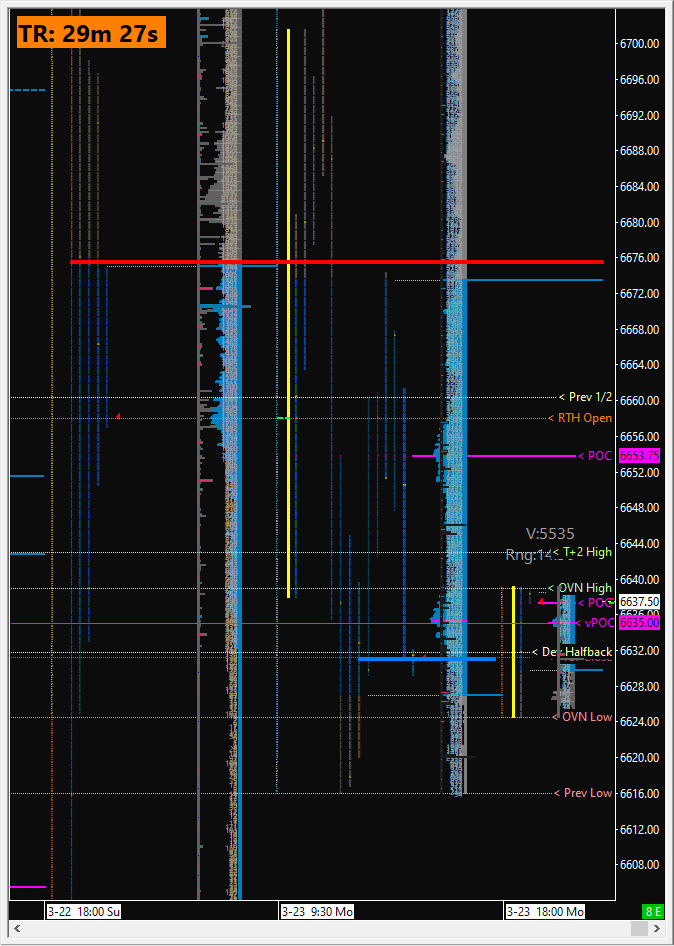

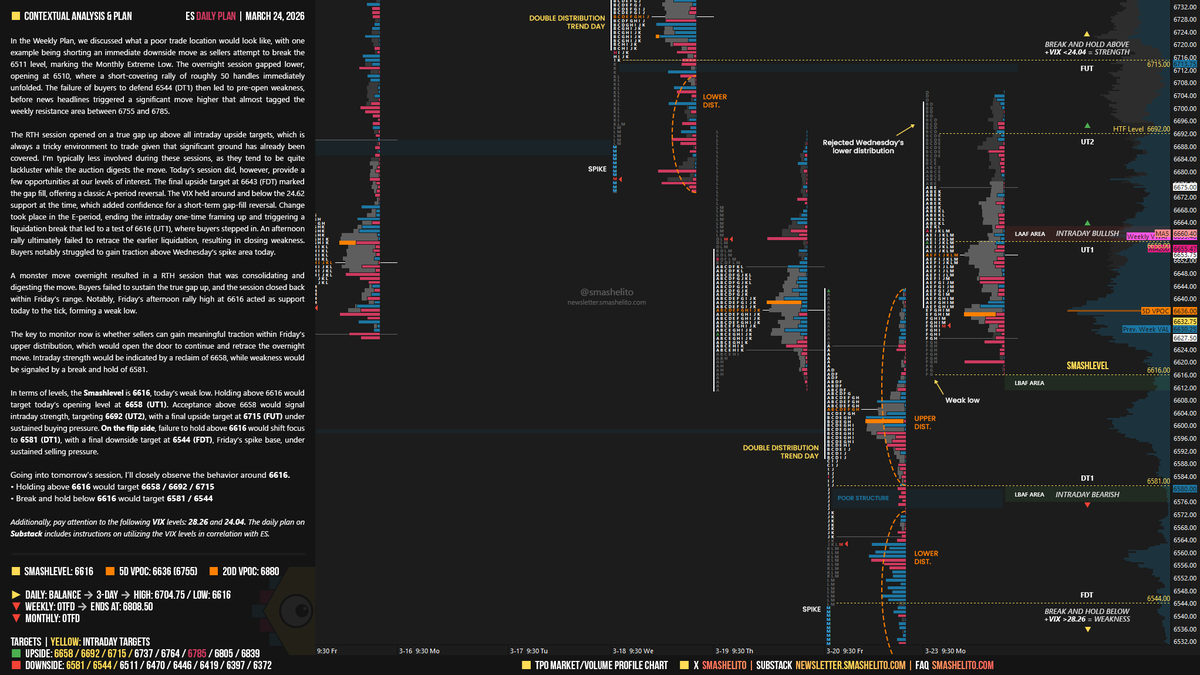

#ES_F Daily Plan | March 24

A monster move overnight resulted in a RTH session that was consolidating and digesting the move. Buyers failed to sustain the true gap up, and the session closed back within Friday’s range. Notably, Friday’s afternoon rally high at 6616 acted as support today to the tick, forming a weak low.

The key to monitor now is whether sellers can gain meaningful traction within Friday’s upper distribution, which would open the door to continue and retrace the overnight move. Intraday strength would be indicated by a reclaim of 6658, while weakness would be signaled by a break and hold of 6581.

Smashlevel: 6616

English

@paxtrader777 @ces921 As if electronic ETH trading was available then...?

English

This is very good analysis. @ces921 and I met the fist time last summer. We had very similar outlooks on the markets. He comes at it from a much higher macro perspective then me, I am coming at this from a much more technical perspective along with an experiential approach.

Craig Shapiro@ces921

Every condition Paul Tudor Jones identified as present going into the Black Monday weekend is present today. The regime configuration, meaning the cluster of overvaluation, yield shock, constrained Fed, mechanical selling overhang, and geopolitical stress, is more completely assembled than nearly any point since October 1987. Individual conditions vary in magnitude relative to their 1987 levels; the analog is about the regime, not about matching historical levels precisely. The valuation overhang is more extreme. The geopolitical catalyst is more intense. The Fed is more constrained. The yield rate-of-change shock is operationally analogous. The mechanical selling amplifier, though structurally different, shares the same feedback architecture as portfolio insurance. The one structural difference that cuts both ways: circuit breakers exist now that did not in 1987. They prevent a single-session 22% waterfall. They also compress volatility into shorter windows post-open and can generate false stabilization signals that attract buyers before the next leg lower. The analog should be read as a regime characterization, not a level forecast. The claim is not that the S&P 500 falls 22% on Monday. The claim is that the configuration of conditions, overvaluation at historically extreme multiples, a yield shock eliminating the equity risk premium, a Fed with no capacity to respond, mechanical selling amplifiers ready to cascade, and an unresolved geopolitical trigger entering the weekend, is structurally identical to the regime that produced Black Monday. That regime produced a 22% single-session crash in 1987 partly because circuit breakers did not exist. In 2026, the same regime is more likely to produce a sustained repricing over days to weeks, with elevated risk of a disorderly session if any weekend catalyst compounds the existing damage. Near-term: Monday is a live risk. The specific risks are a gap down that triggers systematic selling, a VIX spike above 30 that inverts the term structure, and a 10-year yield that fails to rally on equity weakness, removing the last potential hedge. Medium-term: Even without a disorderly Monday, the structural case for a poor risk-reward skew over the next one to three months is independent of the near-term event risk. A negative equity risk premium at a CAPE of near 40, with the Fed on hold and yields rising, is not a setup that resolves with a single session of selling. It is a setup that requires either a material decline in yields, a material decline in equity prices, or a material upward revision to earnings. None of those three conditions is likely to emerge quickly. Monday is a live risk. The next three months carry poor skew regardless of what Monday brings.

English

@TBradleyNC @nicksortor The cratered, wrinkled face of a consummate liar. "The Body Keeps the Score."

English

Roy Cooper IS Tim Waltz, Gavin Newsome, and Abigail Spanberger.

NC is in trouble.

@nicksortor

Acyn@Acyn

Cooper: So my opponent, Michael Whatley, will be nothing but a rubber stamp for Trump. He says what Trump says. He does what Trump wants him to do. So if Trump is in this foreign war—even though he said he wasn’t going to enter such wars—then Michael Whatley is going to be for it. He’s also in North Carolina trying to convince people that prices are down, that we’ve defeated inflation, and that our economy is great. The people of North Carolina know that’s not true. Michael Whatley has been a partisan Republican Party leader for years. He has spent a lot of time in Washington. He became a big oil lobbyist and made a lot of money doing that. He was the chair of the North Carolina Republican Party and recruited right-wing candidates like Mark Robinson—the self-described ‘Black Nazi.’ This is the kind of candidate he supports, and in fact, he is also an election denier. He still insists that Donald Trump won the 2020 election. We do not need that kind of person representing North Carolina.

English

Maria Palmer was allowed to immigrate from Peru at the age of 17

She has repaid our generosity by dedicating her life to ensure that Hispanics who move to North Carolina (and Chapel Hill in particular) can avoid assimilation

English

@dampedspring @AahanPrometheus 7% down...headed to 10, the trend is broken, if one needs to know.

English

It's truly amazing that @AahanPrometheus offers this KISS strategy for free for anybody who cares. Strongly endorse him and his process. Blows away the expensive alternatives and unlike the norm has no massive ego. Just delivers the goods for free.

@aahan_prometheus@AahanPrometheus

Basic Trend Following: Primer We’re going to have a more substantive note from @prometheusmacro on how we construct our basic trend program with the empirics. 1/ This thread will focus on the concepts and exact steps to constructing our Basic Trend Program

English