Morelli

72 posts

Most people overthink their first storage deal.

They spend months underwriting facilities that should've been filtered out in 5 minutes.

Filter things like:

Is the market oversupplied? Pass.

Physical occupancy 85%+ but economic occupancy below 70%? That's revenue hiding in plain sight.

Current rates 20%+ below comps? Real upside.

Seller not motivated? Move on.

I run 7 questions on every deal before I spend a single hour underwriting. Saves me weeks.

I put all 7 into a 1-page deal filter. Reply "send it" and I'm happy to share it with you.

English

@SwissKnifeInv My main defense against cash flow erosion is as follows: they can still lay off a lot more people. Argument against: they can still decide to continue to ramp up investment spend to aim to evolve the business.

English

The $PYPL bear case requires one thing: free cash flow to collapse fast. Fast enough to outrun $6 billion per year in buybacks. TPV is still growing. Revenue is still growing. Braintree margins are recovering toward 5%. Bears need to be right sooner than the buyback can work. So far, they have not been.

English

@DINGELFIRE The hippies won but there's hope with the already-ruined Gen Zs.

English

This is the Canada I miss.

Innovative. Industrious. Pragmatic.

bu/ac@buperac

The 1971 Canadian $10 bill will always remain the GOAT 🐐

English

Con los canapés terminados, los jordanes empapelados y el humo despejándose, newprinces $NWL camino a 12€

Kerry Caberga Valiu@kinders_inverso

Que buena oportunidad de compra en newprinces $NWL antes de que mañana presenten resultados con canapés y humo

Español

@evfcfaddict The market may be hating the dividend cut and lack of monetization of the DOMS stake. Business is still what it is. Stable business but lackluster growth.

English

2/2

I don`t get how anyone who was at the call now says: "I need to sell this now in the low 8s" - this makes 0 sense.

mcap 400m

doms stake 320m

ye debt ~190m

fcf ~45-50m

9x p/e

2,3x ev (-doms)/ebitda

I really like the management team and I think the downside is nearing 0 here.

English

1/2

Bought back some $FILA.MI in the low 8s (sold in the high 9s as I wasn`t happy with their cap allocation progress a few month ago).

Meanwhile they started a buyback programme, confirmed guidance, hinted synergies coming with the latest m&a starting to show up in 2027.

English

@DEgilsson Very reassuring results and guidance on Carrefour front. If I didn't miss anything, doesnt seem as though cash-flow drag will be large.

English

$NWI.MI NewPrinces Q1 2026: €1.5B revenue, €76.5M EBITDA (+21% LFL), €317M net cash, stable despite €27M real estate investment. Princes Retail EBITDA March-April +240% YoY. FY2026 retail EBITDA guided €110-120M, ahead of expectations.

Subsidiary, $PRN Princes Group: £506.6M revenue, £38.2M EBITDA (+17%), 89% FCF conversion. Italian segment margin +640bps YoY.

Acquisition imminent per management of Princes Group.

$NWL

English

@SwissKnifeInv @ahern_brendan Chinese mgmt does not have the same Western mindset of capital allocation. It is always growth first, capital efficiency second.

English

@morellifm1 @ahern_brendan Now is the time to go big in buybacks with the stock depressed.

English

$JD buyback "the Company repurchased a total of approximately 44.5 million Class A ordinary shares (equivalent to 22.3 million ADSs) for a total of US$631 million during the three months ended March 31, 2026. The total number of shares repurchased by the Company during the three months ended March 31, 2026 amounted to approximately 1.6%"

English

@SwissKnifeInv @ahern_brendan Very limited action on that front in the past two years. Mainly they use buybacks to avoid dilution.

English

@ahern_brendan $JD mgmt really needs to step on the buyback gas pedal. This isn’t enough with how much cash they have at these stock levels.

English

@JSE_Invest Would love to see some visibility on the New Businesses front: when will it break-even. Other than that the remaining business is gushing cash.

English

$JD out with another set of solid results. It remains super cheap imo. Some thoughts:

As top line continues to grow from its already gargantuan base, emphasis is shifting to margin expansion: Retail revenue grew only 1.8%, but operating profit rose 16.5%. Retail margin expanded to a record 5.6%. On a group basis, the margin expansion will become increasingly clear as New Businesses losses taper off; right now, this is still a considerable eyesore dampening an otherwise well-oiled behemoth.

Note that JD repurchased US$631m of shares in Q1, equal to ±1.6% of shares outstanding. It still had US$1.4bn remaining under the US$5bn buyback plan at quarter-end. The company has a lot of cash and it is putting it to use effectively on various fronts: top line and new business growth (the cash burn), investments into margin expansion (e.g. robotics), shareholder returns (meaningful buybacks and dividends).

Note also from the release: "During the first quarter of 2026, JD Logistics (“JDL”) launched an upgraded version of its self-developed embodied intelligent equipment, the “LangzuTech Packer” robotic arm" .

As I've mentioned in letters I expect JD's investments into robotics accelerate, and as they do, the market may begin to treat $JD as more of a robotics play, meaning this gives further potential for a re-rating, in addition to the reasons highlighted above.

English

@finphysnerd Think the multiple is actually much lower given it throws off lots of cash flow.

English

Here's a fun, speculative idea. Medica Sur $MEDICAB is a single asset company the owns the top ranked hospital in Mexico for the last 14 years. The company is a long term compounder that has returned 18% annually since 2003 and is trading at around 12x earnings. Very illiquid,

English

@Carlos_MoraM @lucenseinversor Ha dicho que espera que para enero'27 hayan cambiado a la marca GS, no?

Español

@lucenseinversor Algo que debe cambiar NewPrinces es que siempre dan más información por medio de canales no oficiales que por sus propias press releases..

Español

$NWL NEW PRINCES para los que sigáis la compañía os recomiendo ésta entrevista al máximo accionista y CEO Angelo Mastrolia👇🏻

youtu.be/mO36NsQT3ts?is…

YouTube

Español

@realroseceline Gross margin % is down YoY true, however most of the decline in EBIT is attributable to higher investments.

English

$PYPL wasn’t a disaster quarter, but it confirmed something we already know and something I’ve been saying for a long time. The business is still growing, but the quality of that growth is getting worse and worse. That is a big deal!

At first glance, everything looks fine. Revenue is up 7%, TPV is up 11%, and transactions are growing. That is enough to create the illusion that the biz is still strong. But when you follow that growth down the income statement, reality sets in quickly. The business is moving more volume, but not turning it into profit. In other words, the economics suck!

Transaction margin dollars only grew 3%, while operating income actually declined. GAAP EPS fell 6% despite all that payment volume. That gap between volume growth and profit growth is the big problem. It tells you the incremental economics are getting worse, not better.

Margins speak volumes and make this even clearer. Operating margin compressed by roughly 200 basis points, and transaction margin dropped meaningfully as well. In a payments business, margin is not just a number, it is the moat. When margins compress, it usually means competition is intensifying and pricing power is weakening.

That lines up with what you would expect. Payments has become one of the most competitive spaces in the world, with players like Stripe, $ADYEY, and even $AAPL and $GOOG are constantly pushing in. It becomes harder to differentiate, and easier for merchants to route volume elsewhere. Over time, that pressure shows up directly in margins.

There is also a more subtle issue that I think matters just as much. Transactions per active account actually declined slightly, and total accounts were basically flat. This used to be a network effect story where engagement kept compounding. Now it is starting to look more like a utility that people use when needed, not something that deepens over time.

The free cash flow story also needs a closer look. Adjusted free cash flow looks strong on the surface, but a big part of that comes from timing around BNPL receivables. The actual free cash flow number declined year over year.

Then you get to guidance, which is really what drove the stock. $PYPL is guiding to declining EPS in the near term and roughly flat earnings for the full year. That is the part that resets expectations. It tells you this is not a one quarter issue, this is the current trajectory of the business.

When you put it all together, the picture becomes pretty clear. Growth is still there, but it is weaker in quality, margins are moving in the wrong direction, and earnings are not following the top line. That combination forces the market to rethink what kind of business this really is. It starts to look less like a compounding growth story and more like a mature, competitive payments platform.

That is why the multiple compresses. Not because the company is broken, but because the future looks less attractive than it did before. At around 10 times earnings, the market is no longer pricing in a high quality compounder. It is pricing in a slower business with more pressure and less control over its economics.

🌹

CMG Venture Group@CmgVenture

$PYPL | PayPal beat earnings and revenue estimates in Q1 but provided weaker than expected guidance. The stock is -8.1% this morning. 🔹 EPS: $1.34 vs. $1.27 est. ✅ 🔹 Revenue: $8.35B vs. $8.050B est. ✅ Key takeaways: 🔸 Transactions revenue: +7% YoY 🔸 TPV: +11% YoY 🔸 Active accounts: 439M (+1% YoY) 🔸 FY EPS outlook: low-single digit decline to slightly positive growth (no change) 🔸 Q2 EPS outlook: -9% YoY, $1.27 ($1.34 est.)

English

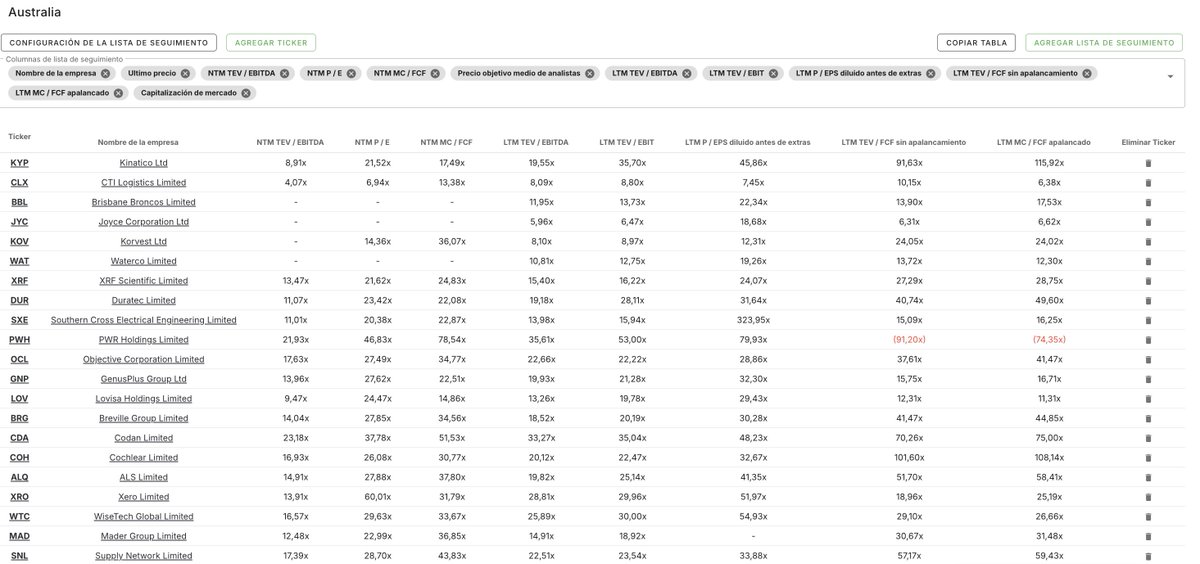

Durante estos días de calma, he aprovechado el tiempo libre para construir una lista de seguimiento de empresas australianas 🇦🇺que, tras un primer cribado, presentan características interesantes: dos de ellas ya en cartera.

En cuanto a la supuesta ventaja de las microcaps...lo más atractivo cotiza a múltiplos bastante exigentes, lo que relativiza bastante esa ventaja teórica.

La intención es replicar este ejercicio país por país.

Quizás sea el embrión de Galician 3.0.

PD: Desconozco el motivo, pero no me dejó ordenar por market cap.

Español

@DINGELFIRE @archer_rs Plenty of stories of Euros who come to North America and immediately buy a cheap pickup truck

English

@archer_rs I only won't buy one because of comically small lanes and parking spots and 2x the fuel costs thanks to excessive taxation.

English

Europeans are not "blocking" US supersized pick up trucks, they are for sale here. We do not buy them because of three reasons.

1 - They are poorly made

2 - They are unreliable

3 - They are stupid

ft.com/content/3eb796…

English

@Daniel___Gordon Está muy barata en respecto a la capacidad de generar caja. Market Cap de Eur700MM contra FCF pasado de 160-200MM.

Español

Esto es lo que me hizo replantear mi inversión+ costo de oportunidad que para mí es importante...

Español

Newprincess $NWL

1)NWC = Activos Corrientes Operativos – Pasivos Corrientes Operativos ( tarde payable) salió negativo pero es normal retail..Pero genera riesgo si las ventas se ralentizan o los proveedores exigen mejores condiciones..

Español

@DEgilsson This is a key part to the investment thesis given the rel size of Carrefour and what I believe the market seems to be worried about. I wish they had been more straighforward about this in the presentation and not as casual with it in the Q&A.

English

@DEgilsson Yes, I saw this later. Interesting because it appears Mastrolia is in conflict with what CFO is saying: "Expect to BEven and gen. +ve cash-flow in '28 from retail". Though perhaps the view is -ve in accrual basis until '28 but cash neutral, and they expect cash-flow +ve in '28.

English

$NWL.MI NewPrinces down 30% from results day high in 72 hours. Record FY2025 results. Manufacturing EBITDA €210M exactly in line with guidance. Princes Group ahead of plan. Net cash €319M. Shareholder equity €971M. Let me explain what likely happened and why the price is wrong in my opinion.

English

@DEgilsson Sorry, coming back to the cash-neutrality on Carrefour, could I ask where you saw this? Looking at the latest presentation right now: 1.03.45 CFO: "By FY28 we expect the retail side of the business to be break-even and generate positive cash-flow"

English

Good catch. It is a ballpark estimate based on the CFO stating 90% of group assets are owned, 31 of 33 manufacturing plants fully owned, 2 leased from the Simington’s acquisition and then they separately confirmied a high level of property ownership within the Carrefour network. The IFRS 16 jump from €99.9M to €402.8M reflects consolidating all Carrefour Italia obligations onto the NWI balance sheet for the first time, that being equipment, logistics, office space, store locations, but that number alone does not tell us the precise owned versus leased split within the retail network. The annual report footnotes should give the exact breakdown

English

@DEgilsson Btw the only caveat with what you've written is that I think your number for the % of retail stores at Carrefour is the opposite. I believe 90% are leased, hence the large increase in IFRS leases.

English