The Bello retweetledi

NGX vs Ecobank: A ₦627 Billion Market Cap Discrepancy Investors Cannot Ignore

So, I was discussing with the TG members during our usual Sunday session, something we have consistently hosted every Sunday since 2021, free of charge. One of the topics we discussed was why continuous dilution should never be ignored when building long-term positions in companies. As we started breaking down the banking sector, we got to @GroupEcobank. We noticed major discrepancies in the reporting of its outstanding shares compared to what @ngxgrp currently displays on its platform, which, ideally, should be the go-to and most reliable source for investors.

So, I decided to do a deeper dive.

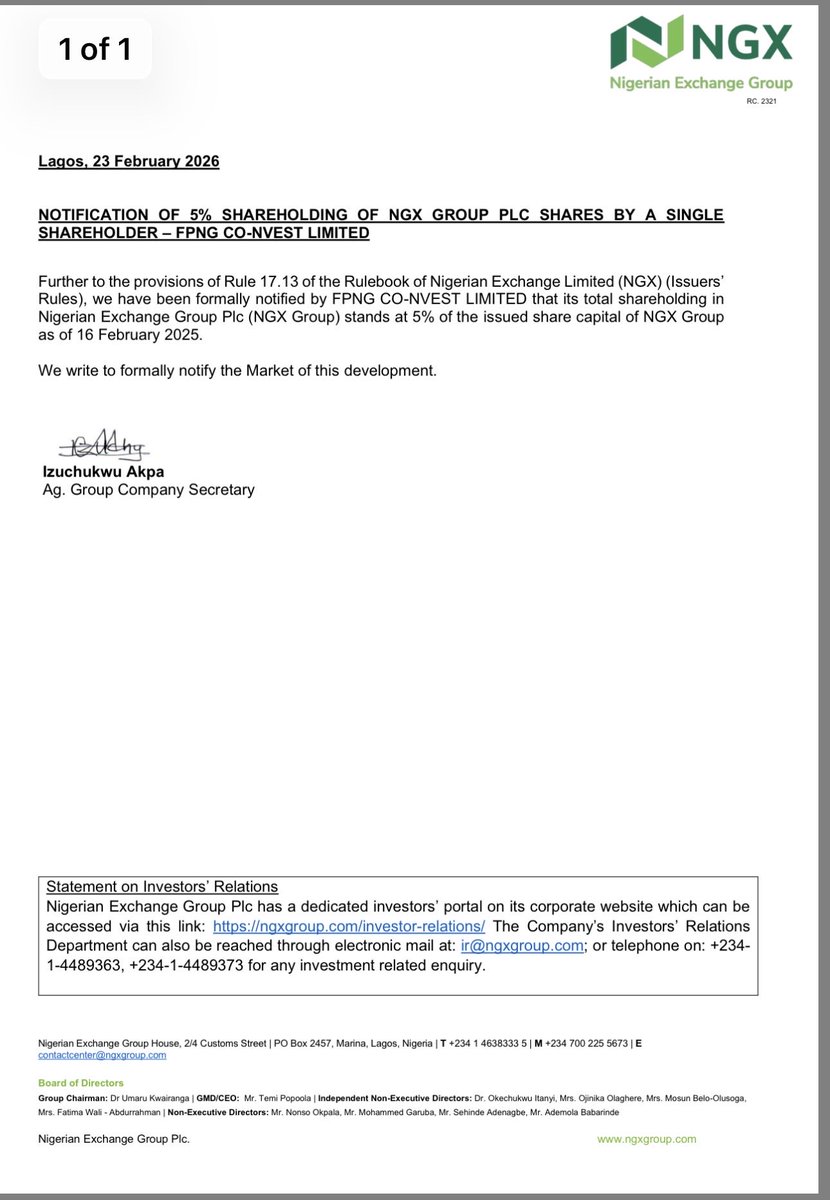

The first screenshot is from the @ngxgrp platform, which currently shows Ecobank’s total outstanding shares at 18,155,073,977. Multiplying that by Friday’s closing price of ₦97.4/share gives a market capitalization of ₦1,768,304,205,359.80.

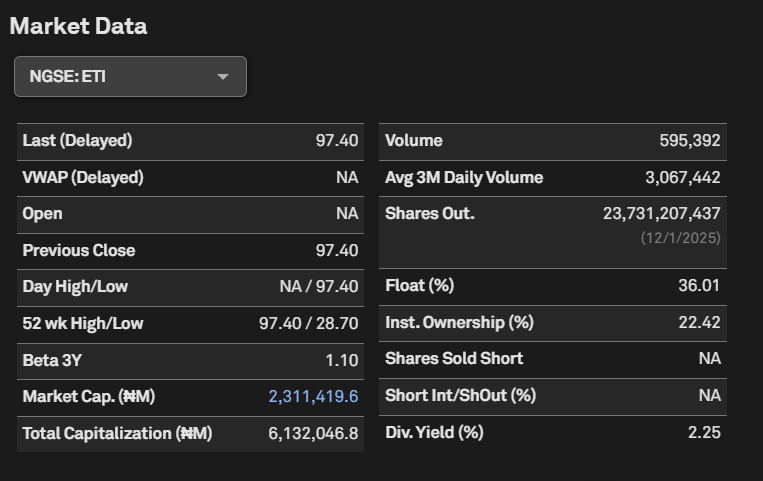

The second screenshot is from S&P Capital IQ, which reports Ecobank’s outstanding shares at 23,731,207,437 shares. Interestingly, the last update there was dated 1 December 2025. Using the same closing price of ₦97.4/share gives a market capitalization of ₦2,311,419,604,363.80.

The final screenshot is extracted directly from Ecobank’s Q1 2026 financial statement under Note 14, page 29. The company itself reported outstanding shares of 24,592,619,000 shares. Multiplying this by ₦97.4/share gives a market capitalization of ₦2,395,321,090,600. What shocked me even more was that the same outstanding shares figure was also reported in Q1 2025.

Now, today is a weekend, so I do not currently have access to the Bloomberg Terminal to cross-check further, but working with these three data points raises serious questions.

So, who exactly should investors believe here?

Personally, I would naturally rely on the company’s own financial statements because they are the primary source, and I should know their actual outstanding shares.

NGXGROUP Market Cap for ETI = ₦1,768,304,205,359.80

Ecobank Q1 2026 Financial Statement Market Cap = ₦2,395,321,090,600

Difference = ₦627,016,885,240.20

That difference is highly material and honestly quite alarming.

Even if we compare S&P Capital IQ with Ecobank’s reported figures, we still get a discrepancy of about ₦83.9 billion, which remains very material. Meaning even S&P Capital IQ appears to be underreporting Ecobank’s market capitalization.

Now, this becomes a serious issue if @ngxgrp is not accurately reporting something as fundamental as outstanding shares. Market capitalization is one of the most basic valuation metrics investors rely on daily. If discrepancies of this magnitude exist, then it raises broader questions around data integrity and market transparency.

What does this mean for the future of our market if basic company information is either underreported or overstated? This is 2026; these are issues we should have moved past long ago. It honestly breaks my heart because these were part of the same structural issues that contributed to market inefficiencies during the 2007/2008 era.

And Ecobank is not even the only example. Even @ngxgrp previously had issues with the reporting of its own outstanding shares at some point (although I do not know if that has now been rectified).

This is why I always encourage investors to scrutinize everything. It is not just about making money. It is also about ensuring our market institutions uphold accuracy, transparency, and investor confidence.

I drop my pen here.

English