NikG retweetledi

NikG

303 posts

NikG retweetledi

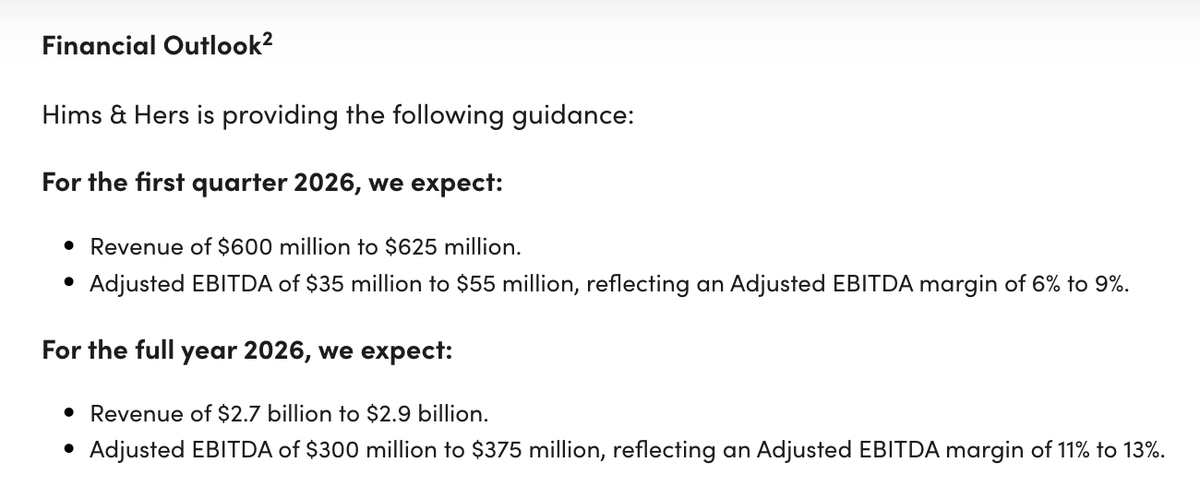

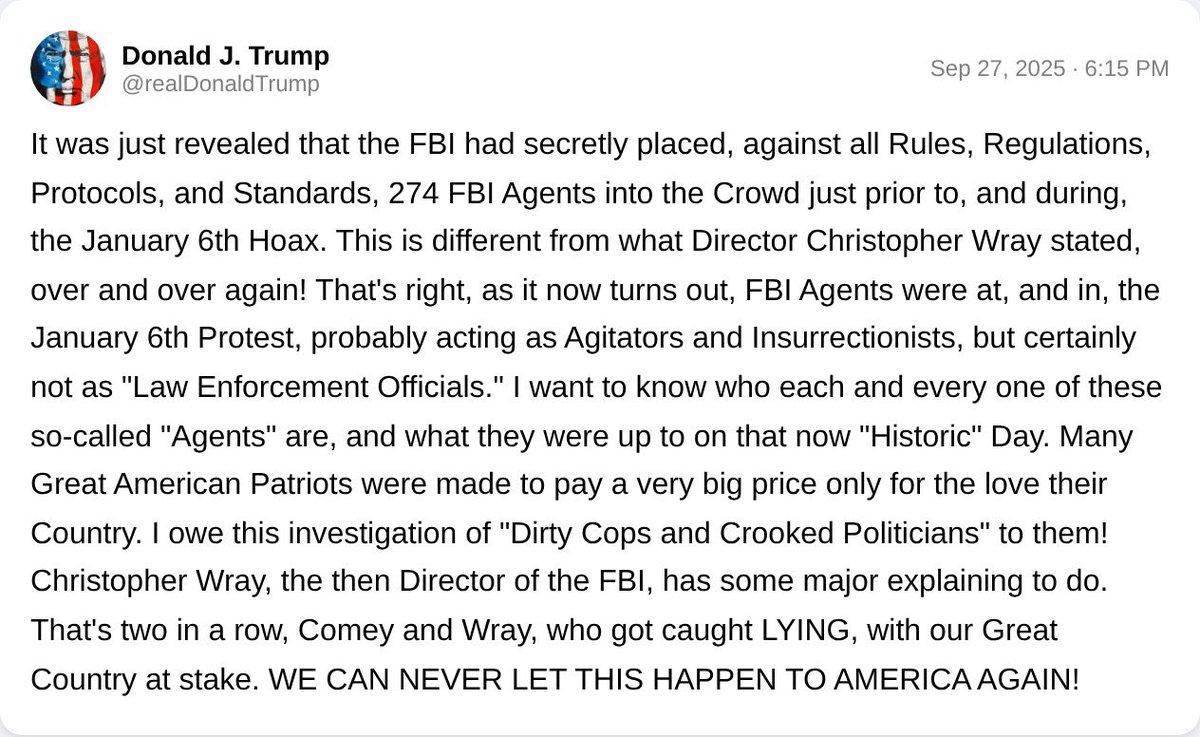

🚨 $HIMS 2026 GUIDANCE

Q1 2026

- Revenue: $600 to $625 million

- Adjusted EBITDA: $35 to $55 million

FULL YEAR 2026

- Revenue: $2.7 to $2.9 billion

- Adjusted EBITDA: $300 to $375 million

English

$EWZ A lot of talk about Brazil.

Over the next few days, I'll focus on posting stocks set to benefit.

$NU chart will be posted today.

What other Brazilian stocks do you like?

Echo Analysis@EchoAnalysis

$EWZ Bull Case — macro, liquidity & structure aligned 🚀 Brazil is coming off one of the tightest monetary regimes globally: • Nominal rates ~15% • Real rates ~10.75% — among the highest worldwide That’s a feature, not a bug. As inflation cools, rate cuts are expected. When rates fall from these levels, liquidity doesn’t trickle in — it surges into risk assets. At the same time, $EWZ offers powerful diversification away from US equities: 🇺🇸 US markets are deep into Wave 5, stretched and crowded 🇧🇷 Brazil is earlier in the cycle, with easing ahead, not behind On the chart: 📈 Monthly golden cross confirmed 📈 ~4.5% dividend yield 📈 Wave 5 target has ~166% upside Macro + structure + yield. These are the setups that don’t stay quiet for long 👀

English

$ZIM - 𝐖𝐢𝐧𝐧𝐢𝐧𝐠 𝐓𝐨𝐠𝐞𝐭𝐡𝐞𝐫

Over the past year, I wrote hundreds of posts about $ZIM.

People kept asking me, why do you keep writing about $ZIM?

It wasn’t about repeating myself.

It was about precision.

I wanted to explain the opportunity so clearly, from every possible angle, that anyone reading could think for themselves.

Not follow me.

Not trust me.

Think.

Based on facts.

Based on logic.

Not opinions.

If the thinking was clear enough, they wouldn’t need conviction from me.

They would have conviction in themselves.

The goal was never to convince anyone to buy $ZIM.

The goal was to make the situation so simple, so stripped of noise, that each person could arrive at the conclusion on their own.

So that one day they would sit in front of their computer, look at their bank account, and feel proud.

Not grateful to me.

Proud of themselves.

Because they understood the logic.

Because they made the decision.

Because they trusted their own thinking.

That was the whole point.

And judging by the messages I’ve received, it seems like many did exactly that.

Many joined along the way.

Many changed their financial lives.

And today, it feels like we win.

Together.

And winning together is infinitely better than winning alone.

English

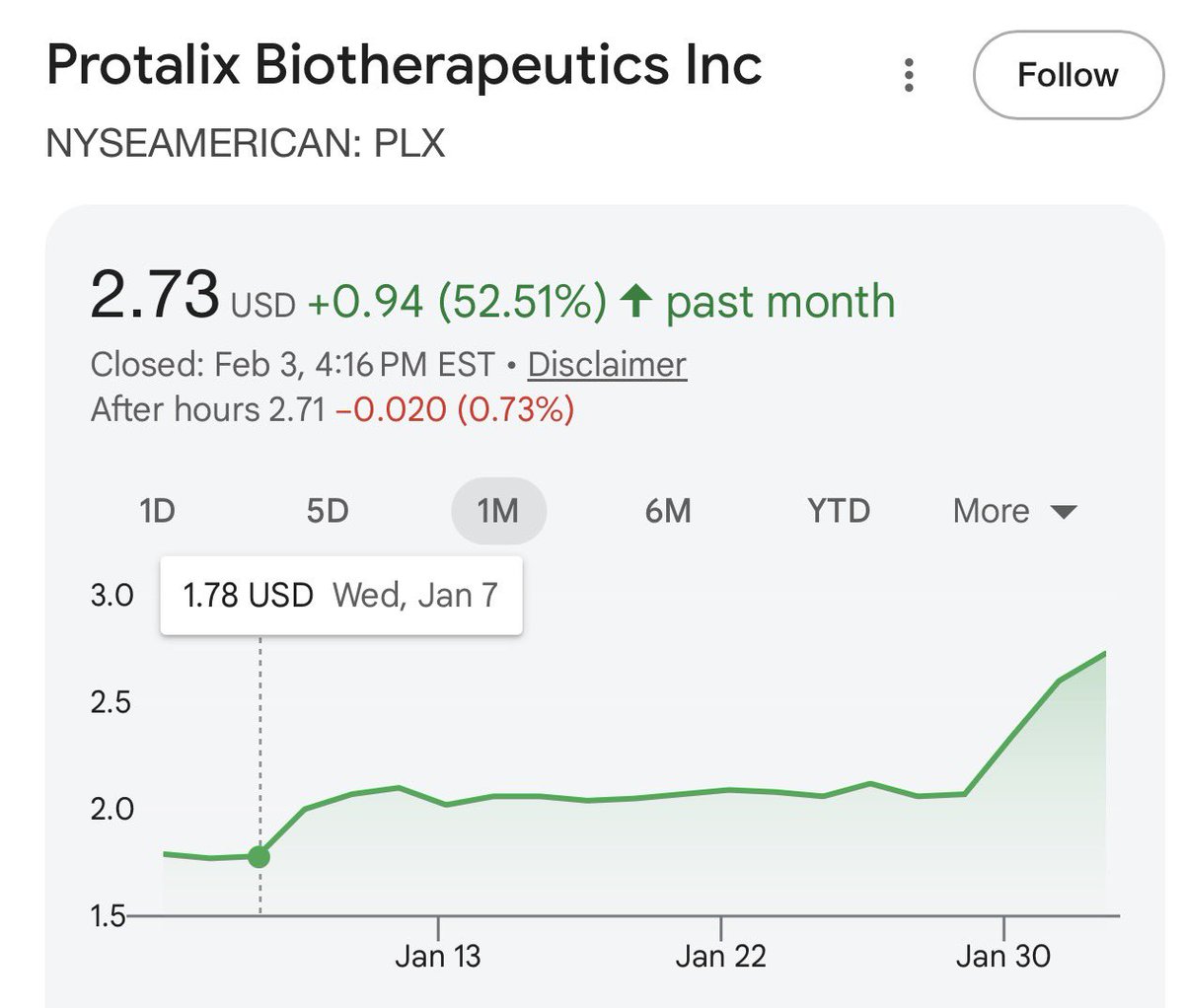

$PLX is up 52.5% from our initial recommendation just a few weeks back, driven entirely by new data that should have re-rated the stock materially higher. It now represents 10.4% of my portfolio. A detailed write-up on what changed and why there’s more upside is coming tomorrow.

Z@ZeeContrarian1

Protalix Biotherapeutics $PLX Today we dig into a biotech stock that didn’t move, both globally and especially in Israel. These are two markets that performed very well overall, yet still left a few companies behind. Shall we begin? $PLX is a micro-cap biotech trading at a market cap of roughly $140M and an enterprise value of only ~$110M. The company is cash-flow balanced. We often use the term “under the radar” loosely, but $PLX truly redefines it. A simple search on Bloomberg shows that only three analysts cover the stock, all from very small and obscure research houses. The situation is so extreme that Bloomberg’s FA function shows estimates only through next year, and even those are barely meaningful. The company and the opportunity This is not the $PLX you may remember. About 6.5 years ago, after a series of business mistakes brought the company close to bankruptcy, $PLX hired an experienced executive from $TEVA Pharmaceutical Industries, Dror Bashan, as CEO. Since then, quietly and perhaps too quietly, he has turned the company around. Today, $PLX has three core assets. Asset #1: Gaucher disease drug This orphan drug is sold through two channels: 1.Direct sales to the Brazilian government, contributing a few million dollars annually to EBITDA. Helpful, but not transformational. 2.Sales through Pfizer ( $PFE). Here, two things went wrong: •The previous management signed a near-zero profitability agreement with Pfizer. •Pfizer does not actively promote the product in the U.S. and does not market it at all in Europe. With only tens of millions in revenue, the product is immaterial to Pfizer and, at first glance, shouldn’t excite us either. But there is a catch. That zero-margin contract expires in 2030. The current absurd situation will not continue. At a minimum, we estimate $5M+ in incremental annual profit starting in 2030. In a blue-sky scenario, $PLX could pressure Pfizer to return the product, potentially before contract expiration. That would be a company-changing event. For now, we treat this as upside optionality. Asset #2: Fabry disease ERT drug (ELFABRIO) ELFABRIO is sold by the large European pharma company Chiesi, with $PLX receiving royalties and milestones. The Fabry ERT market has three competitors, generates close to $2B annually, and grows at 5–7% per year. PLX expects Chiesi to reach ~20% market share by 2030, translating into roughly $100M of annual revenue to PLX, at approximately 90% operating margins. Asset #3: Gout drug $PLX is developing a gout therapy that aims to offer better efficacy and safety than the leading drug from Amgen, which has already surpassed $1B in annual sales and is heading toward ~$2B at peak. Phase 2 results are expected in 2027. If successful and perceived as a billion-dollar drug, $PLX ’s valuation would increase dramatically. Putting it all together With high probability, $PLX should reach roughly $100M in EBITDA by 2030 from its commercial assets alone (Fabry + Gaucher). Even discounting cash flows at 12% and assuming 23% tax, that business alone is worth approximately $450M. Add: •Tens of millions in milestones along the way •Upside from renegotiating or reclaiming the Gaucher product from Pfizer And you easily reach a $500M valuation. The gout drug, assuming only a 5% probability of success, is worth roughly $100M today, based on a conservative 3x peak sales multiple, discounted back. Summing everything conservatively gets you to ~$500M, or 3.5x the current valuation. Someone who clearly agrees with this math is the CEO, who continues to buy shares in the open market and even takes bonuses in stock. Bottom line You’re still reading? Go buy.

English

NikG retweetledi

My list of supplements right now:

Vitamin D3

Vitamin K

Vitamin B (has B1, B2, B6, B12)

Potassium / Magnesium

Nitric Oxide

Calcium / Magnesium / Zinc

Creatine

Anything else I need to add to this?

If so, what does it do?

Thanks for any advice.

English

@ZeeContrarian1 I am trading volatility, vols are getting bid on a daily basis, I see stocks I usually bought long term IV in like CAT at like 26, which is now 10 points higher. Even higher than during the April highs. I can tell you, nobody knows what’s going on but atm nobody wants to be short

English

NikG retweetledi

A pastor who has been living in his car for the past two years with his wife, dog, and 1-year-old daughter received $400,000 from a crowdfund thanks to Content Creator Jimmy Darts in less than 24 hours.🙏🏾❤️💸

English

@thegarybrecka how to fall asleep quick and have a better deep sleep - potentially supplements to support that apart from the usual ashwaghanda, magnesium and melatonin

English

What do you want me to talk about more on my podcast?

I want to help you guys out as much as I can.

English

NikG retweetledi

Chris Stapleton!!

Never heard The National Anthem any better than this.

A worthy Superbowl performance.

English

THE FAT-LOSS RECIPE VAULT

33 High-Protein Recipes for:

- Losing stubborn fat

- Eliminating cravings

- And fixing your body composition

Like + Comment "33" and I'll send you a free copy (24hrs only. must be following or I can't DM)

English

I see why you took a lot of this stuff out of the budget but the $3.6 mil for pastry cooking classes for male prostitutes in Haiti is going too far and I’m glad the Dems demand that be put back in.

🤦♂️🤦♂️🤦♂️

😂😂😂

Libs of TikTok@libsoftiktok

OMG.. you cannot make this up.. These are some of the things the Democrats are demanding we fund: - $3 million for circumcisions and vasectomies in Zambia - $833k for transgender people in Nepal - $4.2 million for lgbtq people in the Western Balkans and Uganda - $3.6 million for pastry cooking classes and dance focus groups for male prostitutes in Haiti - $500k for electric buses in Rwanda - $6 million for media organizations for the Palestinians - $300k for a pride parade in Lesotho - $882k for social media and mentorship in Serbia

English

NikG retweetledi

There won’t be a second date, but at least she knows that 56% of the murders are committed by 13% of the population.

English

@RichardGrenell 100% accurate, but unfortunately German society has been so strongly influenced by the left wing government financed media that people started to internalize this view, very sad

English

NikG retweetledi

🚨President Trump has just released a video on the killing of Iryna Zarutska:

“We have to be viscous, just like they are. It’s the only thing they understand.”

“We cannot allow ... vioIent repeat offenders to continue spreading destruction and death."

English