nnarum

173 posts

Hey all,

Expect our first Developer Insight to land tomorrow morning (8AM Pacific). We'll be talking through the return of the Director, our recently announced Distortions activity for Destinations, and more.

TWID will be going live on Friday, after our second Developer Insights article focused on the Weapons Sandbox.

See you soon.

English

$HIMS Nice move today on the CFO buying shares and the first insider buyer in 2 years 🤯📈

That being said, a gap has now occurred and its very common for insider purchase rallies to reverse course...

I expect $HIMS to close this gap in the coming days as a result, I will be looking to pick up more shares around that price in anticipation for a bigger breakout 📈

English

Marathon Season 2 starts June 2

⚬ Pitch-black runs in Night Marsh

⚬ New defensive Runner Shell: Sentinel

⚬ A fresh start with a full gear reset

Play the full game on PS5 during Open Play Week June 2–9: play.st/4fHWvf1

English

@TheValueTrade Feels like we need a catalyst. Not sure just chopping will get us there on it's own.

GIF

English

$HIMS way too many people do not understand how quickly $HIMS will go to $40...

This is a no brainer..

English

@wave3trades Hope shouldn't be a word you use when investing though. It gives room to doubt your conviction and thesis.

English

$HIMS| Wow some crazy candles there!

Short sellers Covering?

Mike@MikeLongTerm

$HIMS $100 stock that Investors are willing to lend at 0% interest| Convertible Notes 🧵 Not Financial Advice! DYOR! Valuation is ridiculous at this kind of growth(60-70% FY2026 with Eucalyptus acquisition) P/S : 2.34x Fwd P/S: 1.37x This is clearly pricing in the business to fail or to die. While management found a way to improve working capital without diluting shareholders too much unlike other companies trading at 30x-40x-50x-100x P/S. Even at $100, that would still be cheap for me at P/S : 9.7x Fwd P/S: 5.7x For this kind of potential growth long term. And @MikeLongTerm dont plan to sell it at $100. Hims & Hers Health has issued two significant sets of zero-coupon convertible senior notes that sophisticated investors view as an attractive way to gain leveraged exposure to the company's growth story while enjoying bond-like downside protection. These instruments, issued in May 2025 and May 2026, reflect strong institutional demand for HIMS amid its expansion in telehealth, personalized wellness, international markets, and AI capabilities. The first issuance, in May 2025, raised $1 billion (upsized from an initial $870 million plus a fully exercised option) in 0.00% convertible senior notes due May 15, 2030. The second, completed in May 2026, brought in approximately $402.5 million (upsized from $350 million plus option) in 0.00% notes due June 1, 2032. Both are senior unsecured obligations issued via private placement to qualified institutional buyers under Rule 144A. They carry 0% interest and do not accrete principal, making them true zero-coupon structures. Conversion terms highlight the equity upside embedded in these notes. For the 2030 notes, the initial conversion rate stands at 14.1493 shares per $1,000 principal, equating to a conversion price of about $70.67 per share a 37.5% premium to the $51.40 stock price at the time of pricing. For the 2032 notes, the rate is 33.8590 shares per $1,000, implying a conversion price of roughly $29.53, a 32.5% premium to the $22.29 closing price on May 18, 2026. Holders can convert under specific conditions before set dates (November 15, 2029 for the older notes; March 1, 2032 for the newer ones) and more freely thereafter until shortly before maturity. Upon conversion, Hims & Hers may settle in cash, shares, or a combination, at the company's election. To mitigate dilution, Hims & Hers entered into capped call transactions with financial institutions. The 2030 notes feature a cap around $89.95 (75% premium to the then-stock price), while the 2032 notes have a cap near $50.15 (about 125% premium to the pricing-day price). These hedges, which cost tens of millions, reduce potential share issuance or excess cash payments if the stock rises moderately, benefiting existing shareholders while preserving the appeal for note buyers. Redemption and change-of-control provisions add further structure. Hims can redeem the notes for cash starting in 2028 (2030 notes) or 2029 (2032 notes) if the stock trades above 130% of the conversion price for a specified period. Holders gain put rights at par in the event of a fundamental change, such as a takeover. These features balance issuer flexibility with investor protections. What do these investors see in $HIMS unlike short sellers BS? Investors see these notes as a massive opportunity precisely because of the asymmetric payoff at zero interest cost. By purchasing the notes, they effectively lend capital to Hims & Hers at 0% while receiving a long-dated call option on the stock. If HIMS executes on subscriber growth, international expansion (including the Eucalyptus acquisition), AI-driven personalization, and margin improvement, the stock can rise well above the conversion prices, allowing profitable conversion and equity-like returns. Downside remains protected: at maturity, holders receive full principal in cash unless converted earlier, and the senior ranking provides priority over equity in distress scenarios. This convexity limited downside with uncapped (or capped at a high level) upside appeals especially to convertible arbitrage funds, hedge funds, and growth-oriented institutions. They can buy the note, hedge by shorting a portion of the underlying stock (delta hedging), and profit from volatility or the option's value. The zero coupon lowers the hurdle: investors forgo yield in exchange for participation in HIMS's secular tailwinds in personalized healthcare, where demand for accessible treatments in weight loss, sexual health, hair care, and more continues to expand. Strong demand, evidenced by both offerings being upsized, signals deep conviction that HIMS can compound value and exceed the conversion thresholds over the coming years Proceeds reinforce this alignment. Funds from the 2025 notes supported global expansion, AI investments, and technology infrastructure. The 2026 issuance targets similar goals, including the Eucalyptus deal and operational efficiencies. For a growth company, this represents low-cost, non-dilutive (initially) capital that fuels high-return initiatives without immediate cash interest burdens. If the stock performs well, conversion effectively becomes equity raised at a premium, cleaning up the balance sheet while avoiding large cash repayments in 2030 and 2032. Of course, risks remain. If $HIMS underperforms and the stock lingers below conversion prices, the notes function as low-yielding bonds, creating opportunity cost. Dilution can still occur beyond the capped call thresholds in strong upside scenarios, and accounting requires non-cash interest expense recognition. Market volatility, refinancing needs, or execution missteps could also pressure the notes' trading value. Yet these are standard trade-offs that sophisticated buyers willingly accept given the structure's embedded optionality and HIMS's momentum Hims & Hers' zero-coupon convertible notes exemplify modern hybrid financing for high-growth names. They provide the company with flexible capital to accelerate its vision while offering investors a compelling, protected bet on its future success. For these "senior" investors, they are bullish on HIMS's ability to dominate personalized telehealth, these instruments deliver a way to participate at effectively 0% interest, capturing equity upside with a measurable safety net. As the company executes, the path toward conversion could reward both management and these noteholders handsomely. Not Financial Advice! DYOR! Video Source: youtube.com/watch?v=2LRztt…

English

Who’s a player you COMPLETELY forgot played in a Timberwolves uniform??

I’ll start:

English

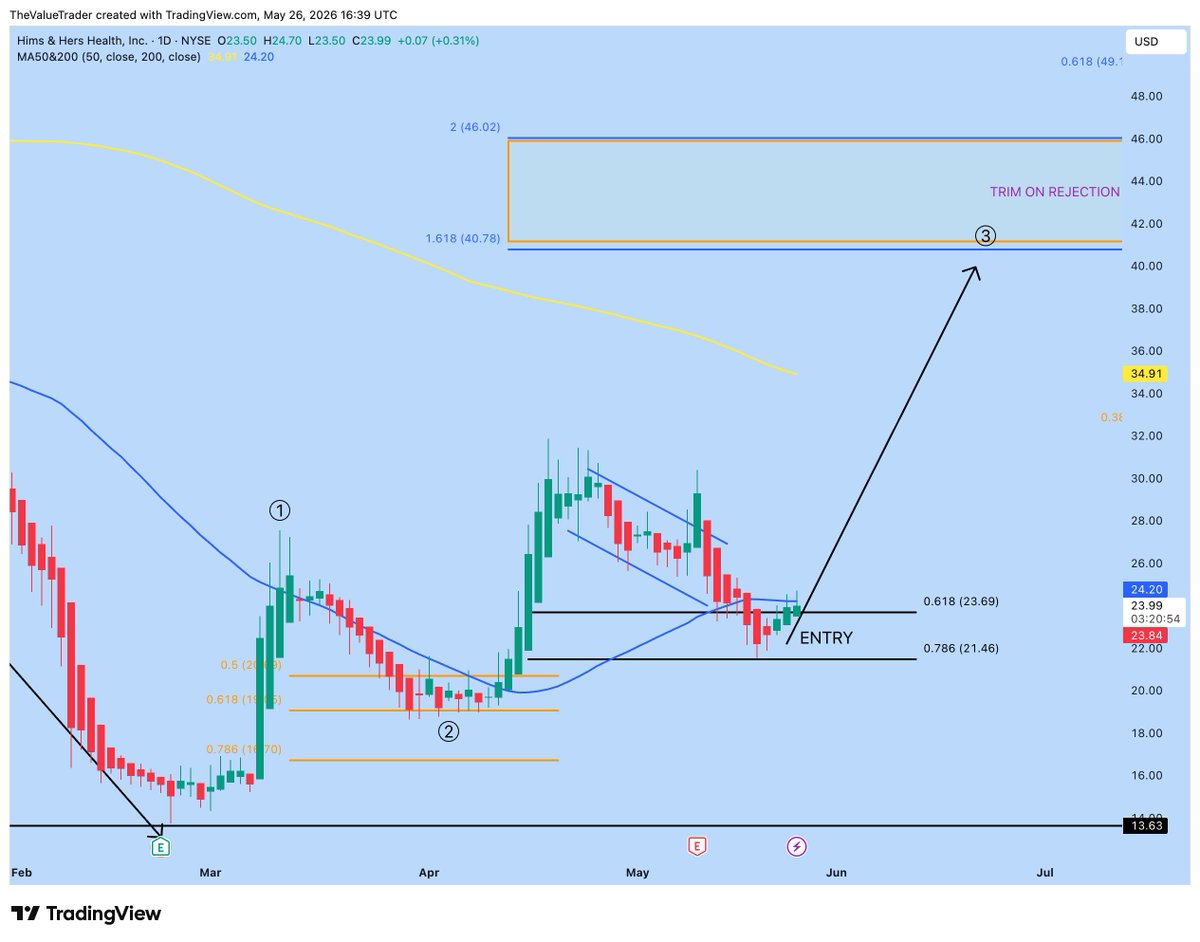

$HIMS

Structure is still intact

Target is still $41

The only thing that matters is patience and conviction

English

Yesterday, we raised $350M from a wide range of high-caliber institutional investors who believe in the long-term vision of what we’re building.

It was more than we set out to raise, and it tells me that the industry believes in the value of our model and the impact of our platform. Given the terms we received, it's clear that our investors are taking a high-conviction view of our strategy.

This offering was designed to keep us flexible and is structured to minimize dilution, while giving us an efficient way to scale aggressively, interest-free, across strategic areas: global growth, infrastructure, and AI-power customer tools.

All of that is how we’re positioning ourselves to keep growing this year and make progress towards our ambitious long-term targets. More than that, though, it is part of how we’ll help more people do a simple but life-changing thing: just feel great.

investors.hims.com/news/news-deta…

English

@TheLongInvest I don't need one position. There is always value somewhere.

English

If you could have one position pull back now

Which one would you take the most advantage of?

English

$HIMS nice test of support on the 200 WMA and bouncing

English

English

💊 $HIMS Just announced increased size of dilution at 11:59 PM

(Up from $300 Million this morning)

English

@wave3trades Lesson learned, one right pick can do the trick. Sticking with it is the toughest part.

English

If you would have bought $10,000 worth of these stocks at IPO, today you would have...

$ASTS $86,000

$PLTR $133,000

$SNDK $333,000

$SHOP $602,000

$NVDA $90,128,000

$COIN $7,800

$BYND $305

English

@xVexity @KobeissiLetter All those words to say TACO. He's just using his own headlines to day trade.

English

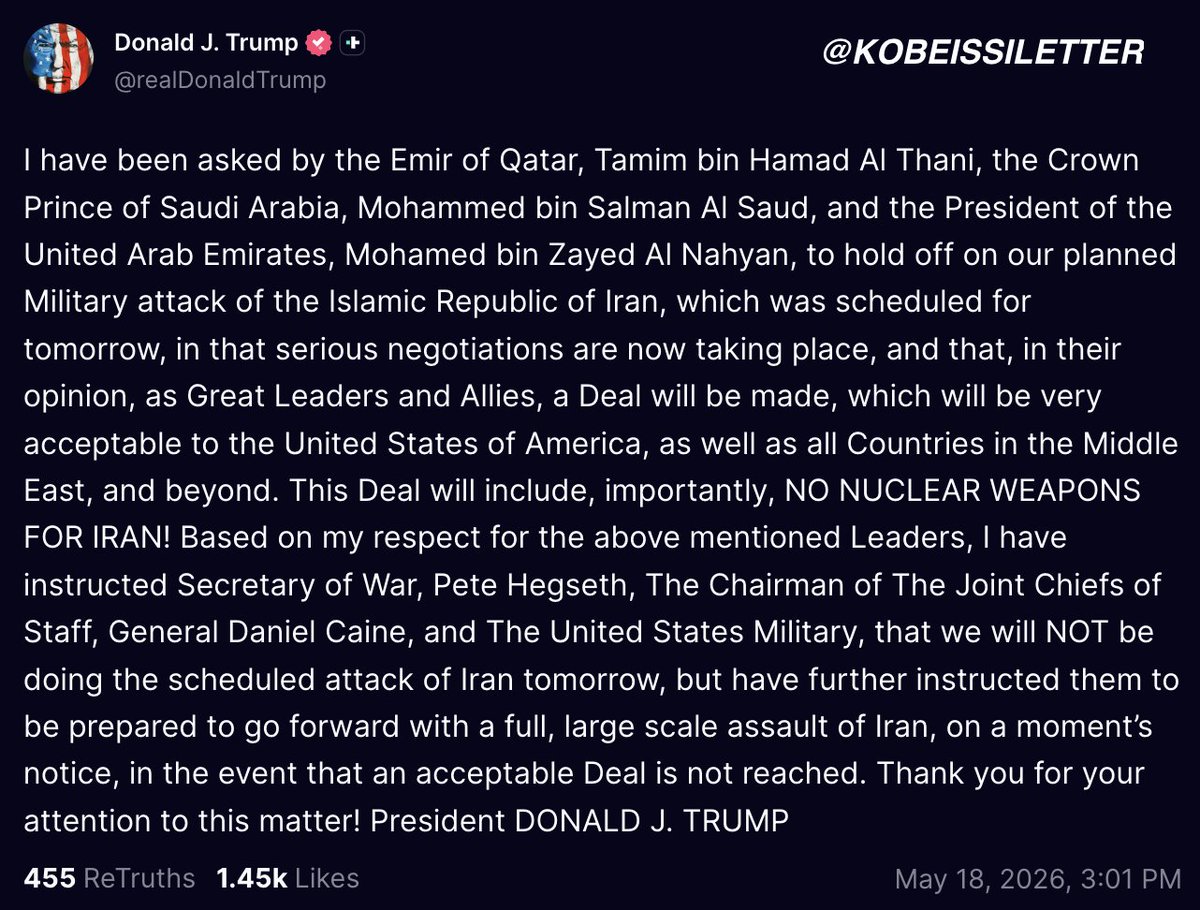

This is classic great power diplomacy in action.

Trump's statement shows the Gulf states (Qatar, Saudi Arabia, UAE) are not just bystanders they're active mediators leveraging their economic weight and relationships with both Washington and Tehran. They called to "hold off" because a major strike tomorrow risked.

• Retaliatory Iranian attacks on Gulf energy infrastructure (they've already hit some)

• Oil prices spiking even higher amid an already volatile 2026 war environment

By pausing the scheduled operation while keeping forces on "moments notice" for full-scale assault, the U.S. maintains maximum leverage.

This is textbook "peace through strength" serious negotiations are happening, a deal is being pushed that includes no nuclear weapons for Iran, and Gulf leaders are helping broker it because their own stability and export economies are on the line.

The timing with broader regional dynamics matters this isn't random. It's pressure + diplomacy to force a durable outcome rather than endless escalation.

Markets will love the de-escalation signal short-term, but the "be prepared" part keeps the hawkish edge alive. History shows these pauses often precede breakthroughs… or bigger moves.

English

BREAKING: President Trump says he has called off a US "Military attack" on Iran which was scheduled for tomorrow after leaders of Qatar, Saudi Arabia, and the UAE called him and asked him to "hold off."

Trump has instructed the US Military to "be prepared to go forward with a full, large scale assault of Iran."

English