Alpha_Ex_LLC@Alpha_Ex_LLC

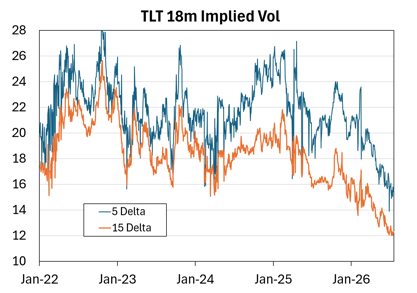

The most interesting and largest trade of yday was in the $TLT where 212k of the Jan'28 100-120 call spread were bought for 62 cents.

One of my sayings is that "equities are short the straddle on rates." Large moves, either up or down, in Treasuries mostly spell trouble for the stock market. With the correlation between stock and bond prices often positive these days, it's been higher rates that get a lot of attention as a threat.

Warts and all, Treasuries still probably rally if there's a significant enough risk-off that leaves the SPX in a large drawdown.

I like the time to expiry, the skew and, especially, the vol in this call spread. The trade has 18 months to expiration, a lifetime away in today's unprecedented pace of change in markets and the world. It collects a nice amount of skew. And you are net buying vol in an unstable asset at extremely low levels. Below the vols associated with the 100 strike (15 delta) and 120 strike (5 delta).

A solid way to part with 62 cents and protect a tail.