Sabitlenmiş Tweet

NResearch

422 posts

NResearch

@nresearchcorp

finance and long-term investing

Berlin, Deutschland Katılım Aralık 2024

57 Takip Edilen40 Takipçiler

@TradeNerdDE Kurzfristig fand ich $NVO als Trade attraktiv. Langfristig sind mir zu viele Unsicherheiten drin:

Politischer Druck auf Preispolitik

+

Wettbewerbsdruck

Sollten hier Preise von der Politik drastisch reguliert werden, dann sorgt das für eine Neubewertung.

Deutsch

Mittlerweile kann man bei $NVO von einer guten Erholung vom low sprechen.

Heute +7%🟢

Auf den Monat gesehen ist Novo Nordisk um 30 % gestiegen🤯

Deutsch

Ich werde nie verstehen, warum Menschen nicht selbst denken wollen und die Verantwortung lieber abgeben. 😅

Maxim Röder@MaximInvestiert

Geduld wird an der Börse belohnt. Wer fundamental starke Unternehmen kauft, wird in der Zukunft belohnt.💎 2024 & 2025 machten sich viele über AMD lustig und fundamentale Daten waren "auf einmal wertlos" 😂 Plötzlich im Jahr 2026 sieht das Bild ganz anders aus📈 Wer hätte das gedacht? 😂Eigentlich jeder, der Zahlen und Daten rational auswertet und nicht sofort emotional wird, wenn der Chart mal korrigiert. PS: Heute um 14:00 Uhr kommt auf YouTube eine Analyse zu AMD.

Deutsch

@MooreDividends Trade hat sich hier ausgezahlt mit 17% Performance. Da hat sich die schlaflose Nacht gelohnt. 😅

Deutsch

Novo Nordisk hat heute Morgen die Ergebnisse für das erste Quartal vorgelegt und ich kann es kaum glauben aber die Jahresprognose wurde angehoben! 🇩🇰

Ein kurzer Überblick:

• Gemeldeter Umsatz: Steigerung um 32 % auf 96,8 Mrd. DKK.

• Sondereffekt: Das starke Plus beim gemeldeten Umsatz und beim operativen Gewinn (+65 %) wurde massiv durch eine Rückstellungsauflösung in den USA beeinflusst (im Zusammenhang mit dem 340B-Arzneimittelpreisprogramm).

• Bereinigte Zahlen: Ohne diesen Sondereffekt sank der bereinigte Umsatz um 4 %

• Wegovy-Pille: Die im Januar 2026 in den USA eingeführte Tablettenform von Wegovy verzeichnete einen Rekordstart mit bereits über 2 Millionen Verschreibungen seit Markteinführung und einem Quartalsumsatz von 2,3 Mrd. DKK. (Das kann sich sehen lassen wie ich finde)

• Wegovy HD: Im April wurde zudem Wegovy HD (höhere Dosierung) in den USA eingeführt, das in Studien einen Gewichtsverlust von fast 21 % ermöglichte.

• Adipositas-Sparte: Der bereinigte Umsatz mit Adipositas-Medikamenten stieg währungsbereinigt um 22 %. Leider werden die Adipositas Raten weiter steigen und davon wird Novo schlussendlich stark profitieren.

Aufgrund der starken Nachfrage nach GLP-1-Therapien blickt das Management optimistischer auf das Gesamtjahr und hebt die Jahresprognose tatsächlich an. Mal schauen was wir Anfang 2027 auf dem Tisch liegen haben. Ich werde dann auf diesen Beitrag zurückkommen.

Bei aller Euphorie die ich gerade habe ist es so, dass Novo Nordisk trotz der Prognoseanhebung weiterhin vor Herausforderungen steht:

• Preisdruck: In den USA belasten Verhandlungen mit Versicherern und staatliche Preisvorgaben (wie unter der Trump-Administration vereinbart) die Margen erheblich.

• Wettbewerb: Der Konkurrenzkampf mit Eli Lilly (Foundayo) und günstigeren Kopien von Abnehmspritzen intensiviert sich.

Moore Dividends@MooreDividends

Klingt wahrscheinlich komisch, aber ich bin echt aufgeregt bzgl. der Novo Nordisk Quartalszahlen morgen. Der Befreiungsschlag kommt hoffentlich.

Deutsch

NResearch retweetledi

$WOLF - Wolfspeed has massive potential as the clear global leader in silicon carbide (SiC) semiconductors, the technology that makes power electronics far more efficient than traditional silicon.

SiC is exploding in demand for electric vehicles, renewable energy, industrial systems, and especially AI data centers that need reliable, high-voltage power.

The company just hit major tech milestones with commercial 200mm SiC wafers and the industry’s first 300mm breakthrough, unlocking lower costs, higher yields, and massive scale.

Backed by CHIPS Act funding, a $6+ billion expansion plan, and fresh refinancing that cleaned up the balance sheet, Wolfspeed is now positioned to ramp production fast while riding the electrification megatrend.

Opened a small position today, high risk...

KaizenInvestor@Kaizen_Investor

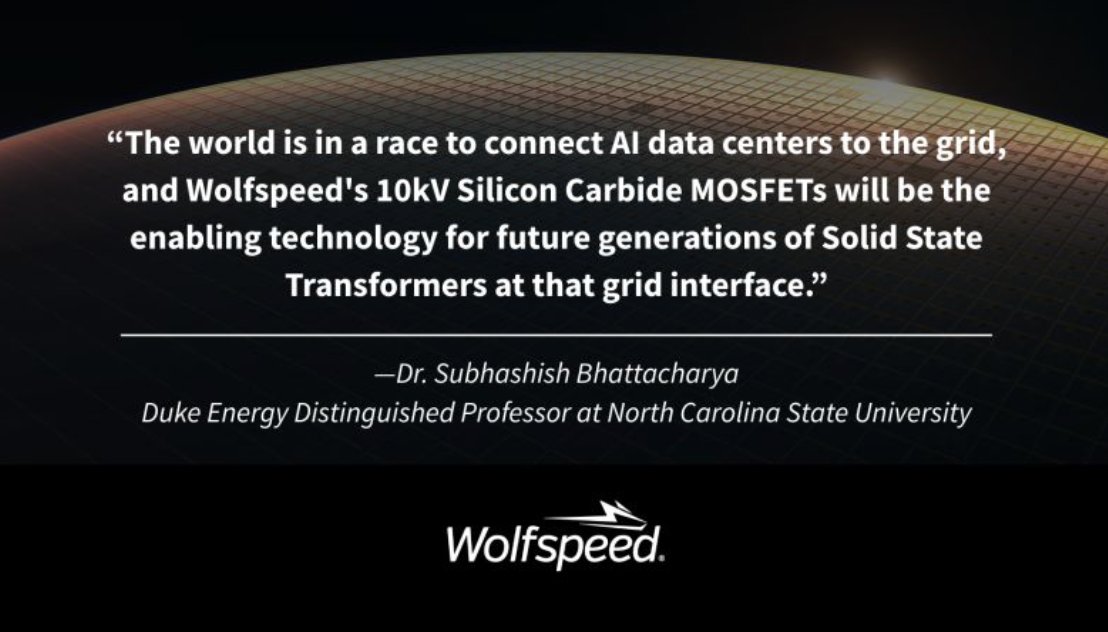

I initiated a position in $WOLF yesterday. I bought the stock at $36. I discovered Wolfspeed as they are an indirect supplier of Filtronic. The space communication tech is rapidly developing. Filtronic is buidling GaN on SiC E-band and V-band amps. I predict that this market will grow rapidly in the upcoming years. Filtronic is buying the GaN on SiC amps from $MTSI. MACOM bought this division form Wolfspeed. $WOLF sold this division in order to make sure they can be entirely focused on their SiC division. They still have a sales agreement with MACOM and are selling their 200mm SiC wafers to MACOM. While most competitors are still refining the 150mm SiC wafers, Wolfspeed is already developing 300mm SiC wafers. 300mm SiC wafers are a game changer for datacenters and for space. 300mm SiC wafers provide 4x the surface area of 150 mm SiC wafers. This geometry yields vastly more chips per wafer and reduces edge waste, drastically lowering the manufacturing cost per device through economies of scale. $WOLF is currently valued at ~$1.7B with an EV of ~$2.6B and ~$800m debt. The market is giving zero premium for future growth or IP. Being the main innovator in the SiC space, I think the market will soon start to give a premium again. Their main sales market now is the EV market. Which is unreliable and often cyclical. I understand the market does not want to give a premium for this. But with the change to 200mm SiC wafers and 300mm SiC wafers, they enter the datacenter and space market. Wolfspeed is not without risk. The company basically went bankrupt in June 2025. They needed protection from chapter 11. They have negative free cash flow with ~$800m debt. They need to invest heavily in R&D for the 300mm SiC wafers and got some competition. They needed government funding under the chips and science act, securing a first $750m with the possibility on another $1B. I’m willing to take this risk as I believe 300mm SiC wafers will be a real game changer. Even with the 200mm SiC wafers, they were able to grow the datacenter segment with 50%. This segment will become more and more important for them. The market is not pricing this in at all. Please note that they report earnings tonight after the bell, which is not ideal. They are still dependent on the EV market (75% of the revenues). So, it can be that they miss earnings tonight but still confirm my thesis. If you don’t feel confident in the thesis, please wait until after the earnings tonight before possibly initiating a position. It’s possible that the stock drops 25% due to the EV market but confirming the datacenter thesis. Please note that this is not financial advice. I just map my own financial journey. If you want to initiate a possition, make sure you do your own research.

English

Also Cloudflare ist echt eine interessante Aktie 😂

Jedes Mal wenn ich sie kaufe und mir dann noch günstigere Kurse wünsche, zieht das Ding einfach davon. lul 😅

Dass das Unternehmen & Management unfassbar gut ist, wissen wir ja schon seit 2024 😎

Maxim Röder@MaximInvestiert

Ich hatte zu Cloudflare schon einige kostenlose bullische Analysen erstellt. Die Aktie hat sich echt gut entwickelt, herzlichen Glückwunsch an alle die hier drin sind 😊 Ich weiß die Aktie ist echt volatil und manchmal gibt es hier starke Abverkäufe, aber langfristig gab es noch keine Red Flags. Ganz im Gegenteil das Unternehmen bewegt sich Schritt für Schritt Richtung Profitabilität und diese wird Cloudflare auch erreichen 😊

Deutsch

@MooreDividends Tracker der Oralen GLP1 Pillen wurde gestern aktualisiert.

Die Grafik widerlegt mein Optimismus.

Deutsch

@nresearchcorp Bin echt gespannt auf die morgigen Zahlen

Deutsch

Novo Nordisk macht zu Beginn der neuen Börsenwoche da weiter, wo sie letzte Woche aufgehört hat.

Wieder ein ordentliches Plus und die 40 € Marke ist wieder greifbar.

Let’s go! 🇩🇰

Moore Dividends@MooreDividends

Die Aktie von Novo Nordisk verzeichnet heute erneut einen sehr starken Tag. Rund 6,5 % stehen heute auf dem Menu. Haben wir ENDLICH die Befreiung vor uns?

Deutsch

Ich frag mich wirklich was Mr. Market, diesem verrückten Spinner, jetzt schon wieder nicht passt…

Hat $PLTR etwa auch zu wenig in AI-Infrastruktur investiert?😂

Klar lieber Markt, ich verkaufe auch immer Aktie von Unternehmen, die ein Wachstum jenseits von gut und böse gezeigt haben. Macht Sinn.

Nicht😅

Deutsch

@TradeNerdDE Gutes Momentum kurzfristig. Spekuliere auf ein Beat im Mittwoch. Bin seit letzte Woche als Trade positioniert.

Deutsch

Das freut mich als $NVO Investor

Endlich etwas Erholung

Haltet ihr $NVO ?

Deutsch

@LazaroInvestor I'm invested myself, but I'm much more pessimistic. The high price of oil and the resulting gasoline prices could put pressure on the earnings.

Promising in the long term, but there could be sell-offs in the short term.

English

$GRAB Earnings Today 👀

$GRAB been crushing it with mobility, deliveries, and financial services across SEA, this could be another strong beat.

Been loading up on the dip and holding long term. Southeast Asia’s growth story is unstoppable, and $GRAB is right at the center of it.

Let’s see some solid revenue growth, margin expansion, and upbeat guidance!

English

@SBetschinger Für Parteien, die etwas gegen eine freie Meinung haben, ist X auch nichts.

Deutsch

Mein Eindruck ist eher, dass auf X die Desinfomationskampagnen von Grünen und Linken mit harten Fakten entlarvt werden. Das mögen diese Leute nicht.

Franziska Brantner@fbrantner

X ist in den letzten Jahren im Chaos versunken. Politische Debatten leben vom Austausch, der Menschen erreicht & informiert. X hingegen fördert zunehmend Desinformation. Deswegen bespiele ich diesen Account nicht mehr. #WirVerlassenX (1/2)

Deutsch

$GRAB is releasing its Q1 2026 earnings tonight.

Given the uncertainty surrounding oil prices, I’m taking a very cautious approach here and expect the results to be disappointing. However, the underlying story remains intact in my view, and I’m extremely bullish on $GRAB.

English

@MaximInvestiert Das bringt mich evt. in Teufelsküche aber ich sage vor den Zahlen $NVO.

Ich bin hier optimistisch für eine Überraschung in den Zahlen am Mittwoch. Bin hier erstmal nur als Trade positioniert.

Deutsch

Welche Aktien/ Unternehmen findet ihr gerade am spannendsten?

Was wird euer Meinung nach (auf 3-5 Jahre gesehen) stark performen und warum? 😊

GIF

Deutsch

@aktien_max Ganz deiner Meinung! Ein negativer Gewinn und ein negativer Free Cashflow zeigen, dass in der Aktie aktuell nur Hype steckt.

Deutsch

$INTC ist wieder bei $100.

Börsenwert von $500 Mrd.

Aus meiner Sicht muss Intel jetzt erstmal starke operative Ergebnisse zeigen, um diese Kursentwicklung zu rechtfertigen.

Wie siehst du das?

Elfi@stockmum

$INTC ist crazy‼️ Kursverdopplung in 1 Monat $44 zu $99 Grund: #Trump will Intel - Chips - Herstellung in USA 🇺🇸 . (1) Bist du in Intel investiert ? (2) Wird Intel weiter steigen ? (3) Ist Intel aktuell zu teuer, um noch einzusteigen ? ‼️ Alles Intel oder was ‼️

Deutsch

@nresearchcorp Ich habe andere Zahlen. Umsatz stieg. Seltsam was für Daten du hast. intc.com/news-events/pr…

Deutsch

Die Intel-Aktie ist weiter auf dem Weg nach oben. Schon wieder 12% rauf. EIN Hoch nach dem nächsten. Manchmal lohnt es sich Weltkonzerne in Krisen einzusammeln. #intel

Deutsch

NResearch retweetledi

Moments after opening the markets, @BillAckman describes celebrating the combined IPO of Pershing Square USA and @PershingSquare Inc.

$PSUS | $PS

English

NResearch retweetledi

BREAKING $GRAB & Robotic Expansion 🚨🤖

A*Star, JTC, Grab enter partnerships with robotics firm Sharpa to build Singapore’s physical AI sector

[SINGAPORE] Artificial intelligence robotics company Sharpa will hire various AI scientists, mechatronics specialists and solutions engineers in Singapore over the next three years.

This is as it aims to deepen its research and development (R&D) efforts in the region, it said on Tuesday (Apr 28).

Headquartered in Singapore, Sharpa plans to grow its headcount to around 150 employees in the city-state, with more than 50 per cent of them in “high-value” R&D roles.

It will also enter strategic partnerships with ride-hailing giant Grab and government agencies JTC and the Agency for Science, Technology and Research (A*Star), Sharpa announced at an event at the National Gallery.

These pacts aim to “develop the physical AI industry in Singapore”, Sharpa said. Physical AI refers to the ability of robotic systems to engage with, and act autonomously in, the real world.

For instance, Sharpa and the A*Star Institute for Infocomm Research will co-handle the development of AI-enabled robotic functions for container handling at ports.

Speaking at the event, Minister of State for National Development as well as Trade and Industry Alvin Tan noted: “This (will) give us a glimpse of what the productivity of tomorrow… might look like, where ports are integrated with robotic systems that can perform complex tasks.”

Such tasks include twist-lock coning and deconing, which refer to container-securing processes at terminals.

Tan also said that the agreements reflect the importance of public-private sector collaboration in turning “research into application”.

Sharpa develops general-purpose, autonomous AI robots capable of “human-like dexterity”, aimed to assist consumers and businesses with repetitive, labour-intensive or high-risk tasks.

Deployment in Punggol Digital District

Under JTC and Sharpa’s partnership, the AI robotics company will deploy a fleet of its flagship North robots within the Punggol Digital District (PDD) across various settings – such as retail and food and beverage (F&B) – and use cases.

Sharpa debuted its autonomous North robot in January.

Spanning 50 hectares, PDD is a new-generation business park for tech sectors including robotics, AI and cybersecurity. It is expected to be fully completed in 2026.

Besides deploying robots, Sharpa will establish an innovation lab in the district. In turn, JTC will grant the firm the use of certain facilities, including the Open Digital Platform, which offers businesses and students access to real-time district data.

Sharpa co-founder David Li said that leveraging PDD’s infrastructure will allow the company to refine its autonomous robots in a real-world setting.

With Grab, it will also explore the use of robotics in F&B operations and logistics at PDD.

Talent development in Singapore

One focus of Budget 2026 was how Singapore will build capabilities in embodied AI, via investments in R&D.

This is mainly to address complex problems in the sectors of advanced manufacturing, maritime and aviation, noted Tan. However, he stressed that it is just as important to develop and invest in the “right (human) talent” for a sustainable future.

He said: “Through existing schemes such as (the Economic Development Board’s) Industrial Postgraduate Programme, we will continue to support more companies and talents to build a steady pool of people that are ready to ride this technological wave.”

The jobs for which companies like Sharpa are hiring – such as AI engineers – are “exactly the type of high-quality jobs” that Singapore wants to create here, he added.

Sharpa was founded in 2024 and also has manufacturing and R&D operations in Shanghai, as well as business operations in Mountain View, the United States.

Mike@MikeLongTerm

BREAKING $GRAB| MOODY's Upgrade to BA2🚀 Moody's upgrades Grab's CFR to Ba2 with stable outlook April 27 2026 Moody’s Ratings has upgraded the corporate family rating (CFR) of Grab Holdings Inc to Ba2 from Ba3 and changed the outlook to stable from positive. The stable outlook reflects the rating agency expectation that Grab’s earnings and cash flow will continue to grow over the next 12-18 months, supported by its leading market position and cash buffers, even as elevated oil prices weigh on mobility and deliveries margins in the near term, Moody’s said in a statement on Monday. It also expects the company to execute its growth strategy prudently, particularly with respect to acquisitions and shareholder returns, while maintaining very good liquidity. “The upgrade of Grab’s CFR to Ba2 reflects continued improvement in its credit quality, underpinned by stronger earnings and cash flow generation,” said Yu Sheng Tay, a Moody’s Ratings Assistant Vice President and Analyst. “While higher oil prices and softer consumer sentiment represent near-term headwinds, Grab’s scale, leading market position in Southeast Asia, and sizable cash buffers allow it to sustain driver support programs, giving it an advantage over smaller regional competitors,” added Tay. According to Moody’s Grab’s credit quality has improved, underpinned by stronger earnings and cash flow generation that it expects to be maintained even as elevated oil prices and softer consumer sentiment create near-term pressure on its mobility and deliveries businesses. The rating agency projected Moody’s-adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA), which includes share-based compensation and interest income, to increase to around $590 million in 2026 and $740 million in 2027, from $483 million in 2025, supported by continued gross merchandise value (GMV) growth across mobility and deliveries, narrowing losses in the financial services segment, and disciplined cost management. Although elevated oil prices arising from the Middle East conflict create near-term pressure on mobility and deliveries margins, Moody’s expects earnings to continue to grow. It is noted that Grab has responded with targeted driver support measures, including fuel rebates and vouchers, co-funded fuel discounts, and has raised fuel surcharges in certain markets. Moody’s expects Grab to have the flexibility to moderate consumer incentives, if needed, to help manage margin pressure, while leaning on affordability-focused products to sustain demand. Furthermore, elevated fuel prices affect all ride-hailing and food delivery operators. Grab’s financial resources and scale as the largest operator in Southeast Asia give it a meaningful advantage over smaller regional rivals, which may lack the financial capacity to sustain driver support programs over a prolonged period, Moody’s added. It also said Grab has stepped up investment activity over the last 12 months, including in autonomous and remote-driving technologies and digital wealth management, as well as the $600 million acquisition of a food delivery business in Taiwan, marking its first foray outside Southeast Asia. Moody’s views the increase in mergers and acquisitions (M&A) activity as broadly consistent with the company’s strategy to strengthen existing business lines, and these transactions will not materially compromise the company’s net cash position. The rating agency also projects Grab’s financial services segment to register its first full year of positive EBITDA in 2027, with breakeven EBITDA targeted by the end of 2026. This reflects continued scaling of the lending business across its digital banking and fintech platforms. Moody’s also expects the company to remain open to inorganic opportunities that enhance its capabilities and broaden its product offerings in financial services. According to Moody’s Grab has very good liquidity. It had unrestricted cash balances and short-term investments of $5 billion (excluding customer deposits of $1.6 billion), compared with $2 billion of debt as of December 2025. It noted Grab’s liquidity is further bolstered by around $1 billion of non-current time deposits and investments. Alongside cash flow generation, these sources are sufficient to fund the company’s share buybacks, proposed acquisitions and investments, capital expenditures, and debt maturities. Moody’s also highlighted that this rating action is based on a baseline scenario of a contained impact on energy markets notwithstanding ongoing disruption to oil supply and limited damage to production or infrastructure. Nevertheless, it recognized that Grab’s credit profile may be susceptible to a more adverse scenario in the conflict, reflecting its exposure to the macro financial conditions risk transmission channel, which could lead to a more consequential impact on creditworthiness. Moody’s said it would upgrade Grab’s rating if it maintains its leading market position in mobility and delivery services; continues to improve its revenue, earnings, margins and free cash flow; demonstrates a track record of profitability at its financial services segment; and maintains very good liquidity and prudent financial policies, particularly in terms of acquisitions and shareholder returns; and debt/EBITDA remains below 2.5 times. The rating, however, could be downgraded if Grab’s market position in mobility and delivery services erodes such that its revenue and earnings deteriorate; losses at its financial services segment increase further or the breakeven timeline is materially delayed; the company pursues an aggressive growth strategy or embarks on outsized shareholder returns; or if leverage, as measured by debt/EBITDA, rises above 3.5 times, particularly if accompanied by a significant reduction in the company’s cash buffer and liquidity position. Source: technode.global/2026/04/27/moo…

English

5000 € in meinem Wachstumsdepot - Einzelunternehmen

Anlässlich der Überschreitung von 5000€ in diesem Depot möchte ich das heute mit euch teilen.

In diesem Depot sind enthalten:

ServiceNow $NOW

Hims & Hers $HIMS

Amazon $AMZN

Microsoft $MSFT

Netflix $NFLX

AMD $AMD

Meta $META

Novo Nordisk $NVO

RocketLab $RKLB

Tempus AI $TEM

Lemonade $LMND

Fluence Energy $FLNC

BYD $BYD

Alphabet $GOOG

Ich habe keine Sparpläne in diesem Depot laufen, sondern kaufe da nach wo ich es für sinnvoll halte.

Im Vergleich zu anderen ist das Depot natürlich winzig.

Aber vielleicht macht es genau das für den ein oder anderen spannend mich zur finanziellen Freiheit zu begleiten.

Deutsch