Clark Peterson

887 posts

Clark Peterson

@optionology

Academy Award-winning Film & TV producer. Dad and husband. Photographer. Investor. @TheAcademy member. @Stanford alum.

Los Angeles, CA Katılım Kasım 2013

2.5K Takip Edilen849 Takipçiler

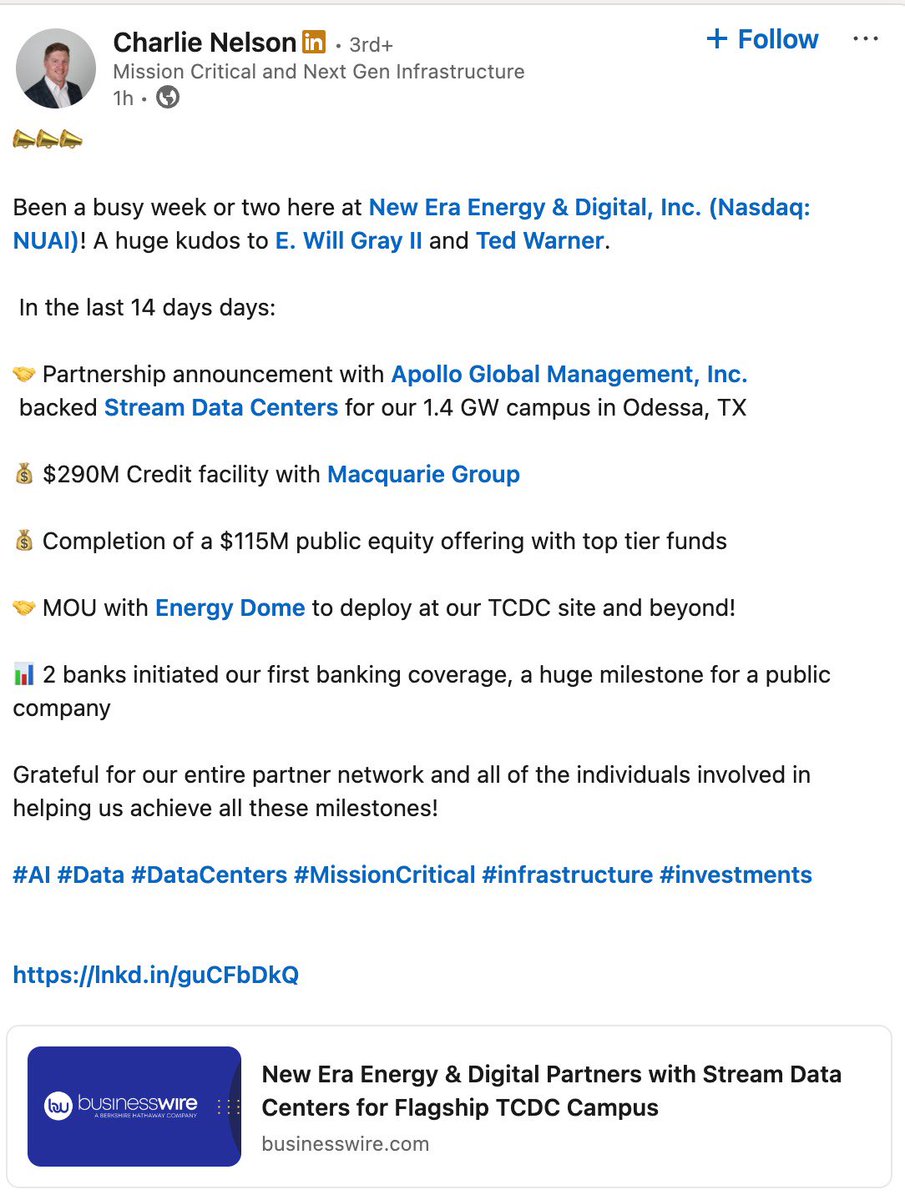

$NUAI 1,4GW and much more 🛻🏗️ According to Charlie Nelson, COO of NUAI, 🔥

English

This is huge and I confirmed it with Claude as well: I read the full 101-page Macquarie Term Loan Agreement filed as an exhibit to the 8-K. I don’t think people have fully digested what’s in this document.

The hyperscaler isn’t speculation. It’s in the binding legal definitions of a $290M credit facility drafted by Vinson & Elkins and Latham & Watkins.

Article I, Defined Terms:

“Acceptable Hyperscale Entity” is defined as a U.S.-based investment grade hyperscaler rated at least BBB- by S&P or equivalent Moody’s. Then: “For the avoidance of doubt, the Letter of Intent Party shall be an Acceptable Hyperscale Entity.”

“Letter of Intent” is defined as “that certain letter of intent, dated as of March 24, 2026, by and among New Era and the other parties thereto (including the ‘Letter of Intent Party’).”

The LOI Party IS the hyperscaler. Not “may become.” Macquarie’s legal team identified this entity, verified its credit rating, and built a $290M facility around it. Latham & Watkins signed off. BBB- minimum means Microsoft, Google, Amazon, or Meta. No other U.S. hyperscaler carries that rating.

The LOI was executed March 24 — eight days before the April 1 public announcement.

Now the tranche structure reveals the timeline:

A-1 ($20M) + A-2 ($30M) = $50M available pre-lease. No tenant signing required. This is SharonAI retirement and early development capital.

A-3 ($40M) + DDTL ($200M) = $240M unlocks upon execution of the Data Center Lease. Section 4.04(a) requires Macquarie to receive “a duly executed Data Center Lease” before A-3 funds. DDTL requires A-3 first. So $240M of $290M sits behind one event: the hyperscaler converting the LOI to a definitive lease.

Amortization Trigger (Section 2.03(d)): If by ~October 8 the lease isn’t signed or less than $50M has been drawn, Macquarie can demand full repayment. This is Macquarie’s internal deadline — they expect the lease well before then.

Monthly equity contributions (Section 6.20): NUAI must contribute $5M/month to the Borrower until the lease is signed. Macquarie is requiring skin in the game every month until the tenant commits.

SharonAI cap confirmed (Section 7.06): Restricted payments capped at $20M from A-1 proceeds. $20M Macquarie + $30M+ offering = full $50M note retired in cash, exactly as Prudent Whale analyzed.

$50M minimum offering (Section 4.02(d)): A-1 couldn’t fund until NUAI closed an underwritten offering of at least $50M. The $100M offering doubled this threshold.

The Data Center Lease is defined as an agreement “to be entered into after the Closing Date” — it hasn’t been signed yet. That remains THE catalyst. But the counterparty is already identified, already investment-grade verified, and already contractually embedded in a facility reviewed by two of the most prestigious infrastructure law firms in the world.

The JV Term Sheet was attached to the LOI and was a closing condition. Macquarie reviewed the full JV economics before committing a dollar.

This document transforms the analysis. We’re not waiting to find out IF there’s a hyperscaler. We’re waiting for a named, investment-grade, Big-Four hyperscaler — already party to a March 24 LOI that Macquarie and Latham & Watkins underwrote — to execute the definitive lease. That’s the only remaining catalyst.

English

Based on the below, I believe NUAI has signed a (non binding) LOI with a Hyperscaler, and this happened on 24 March 2026.

The below 3 points come from the Macquarie Term Loan document here: sec.gov/Archives/edgar… (1/5)

English

This is huge and I confirmed it with Claude as well: I read the full 101-page Macquarie Term Loan Agreement filed as an exhibit to the 8-K. I don’t think people have fully digested what’s in this document.

The hyperscaler isn’t speculation. It’s in the binding legal definitions of a $290M credit facility drafted by Vinson & Elkins and Latham & Watkins.

Article I, Defined Terms:

“Acceptable Hyperscale Entity” is defined as a U.S.-based investment grade hyperscaler rated at least BBB- by S&P or equivalent Moody’s. Then: “For the avoidance of doubt, the Letter of Intent Party shall be an Acceptable Hyperscale Entity.”

“Letter of Intent” is defined as “that certain letter of intent, dated as of March 24, 2026, by and among New Era and the other parties thereto (including the ‘Letter of Intent Party’).”

The LOI Party IS the hyperscaler. Not “may become.” Macquarie’s legal team identified this entity, verified its credit rating, and built a $290M facility around it. Latham & Watkins signed off. BBB- minimum means Microsoft, Google, Amazon, or Meta. No other U.S. hyperscaler carries that rating.

The LOI was executed March 24 — eight days before the April 1 public announcement.

Now the tranche structure reveals the timeline:

A-1 ($20M) + A-2 ($30M) = $50M available pre-lease. No tenant signing required. This is SharonAI retirement and early development capital.

A-3 ($40M) + DDTL ($200M) = $240M unlocks upon execution of the Data Center Lease. Section 4.04(a) requires Macquarie to receive “a duly executed Data Center Lease” before A-3 funds. DDTL requires A-3 first. So $240M of $290M sits behind one event: the hyperscaler converting the LOI to a definitive lease.

Amortization Trigger (Section 2.03(d)): If by ~October 8 the lease isn’t signed or less than $50M has been drawn, Macquarie can demand full repayment. This is Macquarie’s internal deadline — they expect the lease well before then.

Monthly equity contributions (Section 6.20): NUAI must contribute $5M/month to the Borrower until the lease is signed. Macquarie is requiring skin in the game every month until the tenant commits.

SharonAI cap confirmed (Section 7.06): Restricted payments capped at $20M from A-1 proceeds. $20M Macquarie + $30M+ offering = full $50M note retired in cash, exactly as Prudent Whale analyzed.

$50M minimum offering (Section 4.02(d)): A-1 couldn’t fund until NUAI closed an underwritten offering of at least $50M. The $100M offering doubled this threshold.

The Data Center Lease is defined as an agreement “to be entered into after the Closing Date” — it hasn’t been signed yet. That remains THE catalyst. But the counterparty is already identified, already investment-grade verified, and already contractually embedded in a facility reviewed by two of the most prestigious infrastructure law firms in the world.

The JV Term Sheet was attached to the LOI and was a closing condition. Macquarie reviewed the full JV economics before committing a dollar.

This document transforms the analysis. We’re not waiting to find out IF there’s a hyperscaler. We’re waiting for a named, investment-grade, Big-Four hyperscaler — already party to a March 24 LOI that Macquarie and Latham & Watkins underwrote — to execute the definitive lease. That’s the only remaining catalyst. $NUAI

English

In Summary. either 1 of these is true: Either there were 2 LOIs signed 24 March: 1 between NUAI and Stream and a separate 1 between NUAI and an “Acceptable Hyperscale Entity” or

There was 1 LOI signed 24 Mar and NUAI, Stream and an “Acceptable HS” are all parties to this (end)

English

@ThePrudentWhale Great piece! Possibly your best one yet on $NUAI.

English

Latest deep dive on $NUAI is out now:

open.substack.com/pub/prudentwha…

English

@YeshuaNasi @YeshuaNasi follow me back. I want to add you to an nuai chat

English

@fataibrown Closed!

Dilutracker@dilutracker

Dilution Alert: $NUAI (MC: $244M) - Underwritten public offering closed April 10, 2026, implying substantial new equity issuance. - 1.52M shares issued on April 10, 2026, for debt conversion; 2.09M shares issued on March 31, 2026, for acquisition consideration. - $50M convertible note issued to SharonAI (part of acquisition); up to 20% can convert to shares by April 17, 2026.

English

The speaker is Tom Manskey, Director of Economic Development for the Odessa Chamber / Odessa Development Corporation (ODC). He regularly gives updates on major projects like this at Ector County / ODC meetings.

Project Blizzard King = codename for New Era Energy & Digital’s ($NUAI) flagship hyperscale AI/HPC data center campus in Ector County (near Odessa) in the Permian Basin. They’ve been working on it for over a year — land closed, power deals advancing, targeting GW-scale capacity. Solid local confirmation it’s moving forward.

English

@Dragobbbb Great thread. @grok Who is the official saying all this? $NUAI

English

🚨 Do you understand what OpenAI just did?

They killed Sora because it was burning $15 million per day in compute costs.

The entire product made $2.1 million in its lifetime.

> Cantor Fitzgerald analyst Deepak Mathivanan broke down the math. One 10-second video required 4 GPUs running for 40 minutes at $1.30 per clip. At scale, that's $5.4 billion annualized.

> Active users collapsed from 1 million to under 500,000. Downloads fell 66% from the November 2025 peak.

> Disney had committed a $1 billion investment and character licensing deal. They found out Sora was dead less than one hour before the public announcement.

> OpenAI lost $13.5 billion in the first half of 2025 alone. Despite pulling in $4.3 billion in revenue.

> The freed-up GPUs went to an internal project codenamed "Spud" — a coding tool built specifically to compete with Anthropic's Claude.

This wasn't a product failure. It was a $5.4 billion annual burn rate threatening the entire company's IPO at a $730 billion valuation.

Sora didn't die because the tech was bad. It died because the economics of AI video generation are fundamentally broken. And I think every other AI video company — Runway, Pika, Kling — is running on the same impossible math right now.

That's a wrap.

P.S. I made a free toolkit breaking down 100+ mental models used by history's greatest thinkers — the same frameworks that help you see patterns like this before everyone else.

5,000+ downloads. 113 five-star reviews.

Comment "MODELS" and I'll send it to you.

If you're new here, @GeniusGTX is a gallery for the greatest minds in economics, psychology, and history. Follow along for more similar content.

Cheddar@cheddar

Last week, OpenAI announced that it is shutting down Sora — its AI video generation app — just six months after launching. The app will go dark on April 26, with the API following on September 24. The reason OpenAI gave was straightforward: Sora was burning through roughly $1 million per day in computing costs while user numbers had collapsed from a peak of one million to fewer than 500,000. OpenAI says it needs to redirect those resources toward coding tools and enterprise products ahead of its expected IPO. The shutdown also killed a $1 billion deal with Disney, which had signed on to license its characters for the platform — and found out Sora was closing less than an hour before the public announcement. OpenAI framed the decision as a strategic refocus, saying the Sora research team will now shift toward world simulation research to advance robotics. Users are being urged to download their content before the shutdown deadlines. #ai #sora #openai

English

This is not NLP. Not sentiment. It is executive cognition measured through language, built on 40 years of management science (Upper Echelons Theory, Hambrick and Mason 1984).

I did my PhD on this at Columbia.

TonalityIQ is the quantified version at scale.

Run MSFT yourself: eventhorizoniq.com/tiq/MSFT

English

I analyzed 84 Microsoft earnings calls from Ballmer through Nadella. My system detected something the Street is missing. Satya's language is ahead of his numbers for the first time in a decade. Here is what the data shows:

English

@TJTheWheelDeal I’ve learned this lesson early on: she doesn’t want a solution, she wants you to listen, agree the price is crazy, a question about her day, and finally a compliment. Feel free to steal this formula.

English

Wife calls me all paranoid saying it was $101 to fill up her Porsche. IT’S NORMALLY $80 DOLLARS AND NOW ITS OVER $100 AND I DID’T EVEN FILL IT UP ALL THE WAY!

Me: I’m like Buy a Tesla.

Her: They are ugly.

Me: So is the gas bill.

Me: Pick your ugly lol

Yeah…I’m on the couch for sure tonight or guest bedroom lol

English

One of the most moving reads of my life. The kind of blessing that will never leave; the kind of story that shapes simply by being read. I'm grateful and moved forever.

Mule Boy by Andrew Krivak.

English

@litigious_dulce How is this still under $6? Ppl clearly son’t get hoe big $NUAI is going to be. What a phenomal find.

English

$NUAI recently appointed Ted Warner as CFO. (newerainfra.ai/news/new-era-e…)

Warner was previously Managing Director and Head of Energy & Power Infrastructure at Northland Capital Markets — the investment bank behind many of the largest financings in the digital infrastructure space. This is a significant hire worth understanding in detail.

Warner's track record in data center financing is unusually deep. According to Northland’s own materials, his group originated and executed nearly $7 billion in lead managed financings since he rejoined the firm in 2020, with a heavy focus on digital infrastructure and HPC data center development across the capital stack.

The best way to understand what Warner does is to look at his work with Applied Digital ($APLD) — arguably the clearest case study of a single banker helping transform a small-cap power and mining company into a legitimate institutional-grade AI data center platform.

When Applied Digital needed $50M in April 2024 to advance its HPC data center in Ellendale, North Dakota, Northland served as sole placement agent on a convertible debenture. (globenewswire.com/news-release/2…)

Four months later in August 2024, Northland placed another $53.2M in convertible preferred stock to keep the Ellendale buildout on track. (globenewswire.com/news-release/2…)

Then came the deal that changed the company’s trajectory entirely. In January 2025, Northland served as sole placement agent on a $5 billion perpetual preferred equity financing facility with Macquarie Asset Management — one of the world’s largest infrastructure investors managing approximately $634 billion in assets. The deal provided up to $900M for the Ellendale HPC campus and gave Macquarie a right to invest up to an additional $4.1 billion across Applied Digital's future HPC pipeline, supporting over 2 GW of data center development. Goldman Sachs served as senior financial advisor. Citizens JMP, TD Securities, and Needham also provided advisory services. But Northland — Warner's team — was the sole placement agent. (globenewswire.com/news-release/2…)

That deal essentially took Applied Digital from a company scrambling to fund a single campus to one with multi-billion-dollar institutional backing to build a national HPC data center platform. The structure — perpetual preferred equity with a 12.75% dividend, 15% common equity interest, and a 1.80x liquidation preference — allowed APLD to retain 85% ownership of its HPC business while recovering over $300M of its existing equity investment. (macquarie.com/us/en/about/ne…)

Warner's group didn't stop there. In April 2025, Northland placed a $150M convertible preferred equity facility for continued Ellendale campus development. (globenewswire.com/news-release/2…)

By late 2025, they were drawing an additional $787.5M from the Macquarie facility to fund both Polaris Forge 1 in Ellendale and the new Polaris Forge 2 campus in Harwood, North Dakota. (constructionreviewonline.com/applied-digita…)

In December 2025, Northland placed yet another facility — a development loan from Macquarie to fund pre-lease development costs for new AI factory campuses, with an initial $100M in draws while Applied Digital negotiated with another investment-grade hyperscaler for multiple additional sites. (ir.applieddigital.com/news-events/pr…)

From a $50M convertible to a $5B institutional partnership to a multi-campus national buildout — all with the same placement agent quarterbacking the capital formation. That's the Applied Digital story, and Warner was at the center of it.

His group’s reach extended well beyond APLD:

Riot Platforms ($RIOT) — In February 2025, Riot announced it had engaged Evercore as financial advisor and Northland Capital Markets to support the evaluation of AI/HPC uses for its Corsicana Facility power assets in Texas. (sec.gov/Archives/edgar…)

Bitfarms ($BITF) — Northland acted as sole placement agent on Bitfarms’ conversion of its Macquarie debt facility to $300M in project-specific financing for the Panther Creek 350 MW HPC/AI campus in Pennsylvania. (globenewswire.com/news-release/2…)

Bitdeer ($BTDR) — In its March 2025 production update, Bitdeer disclosed it had formalized an engagement with Northland Capital Markets as financial advisor for its HPC/AI data center development strategy. (sec.gov/Archives/edgar…)

TeraWulf ($WULF) — Warner personally signed the amendment adding Northland as an agent under TeraWulf’s sales agreement in August 2023, positioning the firm on TeraWulf’s capital markets platform. (sec.gov/Archives/edgar…)

Super Micro Computer ($SMCI) — Northland served as co-manager on Supermicro’s follow-on offering of common stock in late 2023, alongside J.P. Morgan, BofA Securities, and Goldman Sachs. (northlandsecurities.com/ncm-co-manager…)

Prior to this run, Warner spent 8 years as a founding member of Northland’s energy banking practice, participating in 150+ transactions totaling over $10 billion. He also served as CFO of Fountain Quail Energy Services, a PE-backed oilfield services company. (northlandsecurities.com/team_member/te…)

For context on where $NUAI stands today: the company, formerly New Era Helium, pivoted to AI and digital infrastructure in August 2025. Its flagship project is the Texas Critical Data Centers (TCDC), a campus in Ector County, Texas, planned to scale to over 1 gigawatt of capacity on a 490+ acre site. The parallel to Applied Digital’s starting position is hard to ignore. As recently as 2024, APLD was a small-cap company with power assets, a data center thesis, and a need for institutional capital to scale. Warner’s group provided the financing pathway that took them from that starting point to a $5B Macquarie partnership and a multi-gigawatt development pipeline. NUAI today has power assets from its legacy as an energy company, a massive data center project, and a similar need to access institutional-scale capital to fund the next phase.

Thus, it’s meaningful that Ted Warner, the banker who had a seat at nearly every significant transaction in the power-to-compute pipeline, is now the CFO of NUAI. Warner had broad visibility into deal flow across the digital infrastructure landscape — he saw the pitches, the power positions, the hyperscaler LOIs. He had a strong sense of which projects were real and which weren't. With all of that context, he chose NUAI. That decision is informative for a few reasons.

First, it suggests he sees a valuation disconnect. Warner knows what these assets trade for. If NUAI were fairly priced, there would be less incentive to leave banking for an operating role. His move implies he sees a gap between where NUAI trades and where its assets sit — and he's willing to stake his career on that gap closing. That carries more weight than a price target.

Second, it raises the probability of a hyperscaler partnership. Warner has seen these deals from the inside. He understands what a company needs to look like before a hyperscaler signs. If he didn't believe NUAI was credibly on that path, the move would carry significant career risk. The timing and NUAI's current trajectory are consistent with the kind of catalyst convergence that has driven other companies in the space — like APLD's Macquarie partnership — from relative obscurity to institutional relevance.

Third, it reflects confidence in the team. Warner has worked with dozens of management teams in this sector. Joining one full-time, with your compensation and reputation attached, is a stronger endorsement than any external rating.

From a credibility standpoint, Warner brings roughly two decades of experience structuring the exact type of financings NUAI will need to execute — along with institutional lender relationships, infrastructure fund access, and sell-side credibility that would be difficult to replicate.

Finally, we should consider the compensation structure. NUAI compensates its C-suite through stock options and RSUs with multi-year vesting, and Warner is under the same framework. That makes him not just an executive but a co-investor — dilution hurts him, poor execution hurts him, and every capital structure decision he makes is informed by his own exposure to the outcome.

None of this guarantees a specific result, but when someone who financed many of the sector's winners decides to join an operating company, the signal is worth weighing seriously.

English

$NUAI

The incentive comp structure for the new CFO says it all…don’t think a guy of this caliber would sign on unless he thought this thing had massive upside. My range for FV of 3GW nat gas data ctr power for $NUAI is $48-72/share. The other 5GW of nuclear is pure optionality at this point, but once they sign a partner investors will start to put a value on that call option. Nuclear timetable would be 2030 and beyond.

Per the PR:

“The RSUs vest ratably on a monthly basis over a four-year period conditioned on Mr. Warner’s continued employment with the Company as of each applicable vesting date. The PSUs vest based on successful achievement of the applicable performance criteria during the period beginning January 1, 2026 and ending on December 31, 2030 and are also subject to time-based vesting on a monthly basis over a four-year period conditioned on Mr. Warner’s continued employment with the Company as of each applicable vesting date. The PSUs consist of: (i) 203,476.24 PSUs that vest based on the Company entering into a binding commercial agreement with a hyperscaler with minimum production of 200 megawatts (the "Lease"); (ii) 203,476.24 PSUs that vest based on the Company achieving a final financial closing relating to the Lease at the Company’s Ector County, Texas site (the "Site"); (iii) 203,720.52 PSUs that vest based on: (A) the Company achieving commercial operation at the Site and (B) the volume-weighted average closing price of the Company’s common stock over any 90-day period during the performance period being at least $15.00; and (iv) 610,673 PSUs that vest upon the Company completing a material credit facility sufficient to support the Company’s project development with a major financial institution on or before June 30, 2026.”

English

If your Mining Mafia membership application is still pending or you want a fast-track review on a new application… reply with “review” within 4 hours… I’m actively reviewing applications.

If you’re an existing member and want to show your support comment “Few”

x.com/i/communities/…

English

@EKatzovitz @bitcoinbutcher1 Stay safe and take care of yourself.

English

@bitcoinbutcher1 Pull ercots rioo it is public information. Can't do now. Busy with other things like staying alive

English

Until $iren can substantiate their 🇨🇦 profitability via lower retrofit cap ex, absence of colocation fees and higher contract rates post $msft, it will be grouped with $crwv

Talking points will not cut it in this market. The financials do the talking.

Show and tell is coming in May

James Chanos@RealJimChanos

It’s hard to overstate how bad the $CRWV results/guidance were, but consider this: CoreWeave would still be losing money if they depreciated their GPU’s over 10 years! And at a conservative industry-standard 6-yr life, Coreweave would have zero EBIT coverage of their interest.

English

@DD_Geopolitics So what percentage of Iranian in Iran are against what happened today and what percentage are happy about what happened today?

English

🇮🇷 Iranians chant "DEATH TO AMERICA" as the sun rises on Iran the morning after the murder of Ayatollah Khamenei.

English

SHOCKING: 99% people using Claude are barely scratching the surface.

Right now, the entire internet is screaming “Claude, Claude, Claude”...

But here’s the truth: just chatting with it won’t change your life.

To unlock its real power, you need to master:

• agentic workflows

• Claude Code

• skills, automation & system-level usage

I spent 100+ hours researching and compiled the best Claude resources from across the entire internet — videos, repos, guides, books, and papers.

I’ll give it to only 4,500 people.

To get it:

1. Follow me MUST (so i can dm)

2. Comment “Claude”

3. I’ll DM you the document 📩

If you don’t follow or comment, you won’t receive it

English

@fataibrown @KashRamki Thanks for sharing. Is this message to you?

English