The Pathfinder

6.2K posts

The Pathfinder

@path1finder

Private biotech investor with a lot of luck - so far. Don't think that anything that I write makes sense (no investment advice!) and do your own DD! Good luck.

Earth Katılım Şubat 2010

333 Takip Edilen1.1K Takipçiler

@Biohazard3737 He would qualify as a professional day trader

English

@Biohazard3737 the worst is that they don't even try to hide their (half)illegal or at least unethical business activities. It's blunder in front of American eyes....

English

Hear me out... What if they bring Prasad instead?

David Lim@davidalim

SCOOP: FDA Commissioner Marty Makary is resigning from the agency. Kyle Diamantas, who previously worked as the top food official at the agency, will lead the FDA in an acting capacity. w/ @Gardner_LM: subscriber.politicopro.com/article/2026/0…

English

The Pathfinder retweetledi

ANI Pharmaceuticals Reports First Quarter 2026 Financial Results and Raises 2026 Financial Guidance $ANIP crweworld.com/article/news-p…

English

$XERS raising guidance to $380-$390 million ir.xerispharma.com/news-releases/…

English

The Pathfinder retweetledi

I actually missed this from earlier. Guess at least partially explains some moves today

I'll say this. Makary is just a puppet. Back when he was assigned, he actually had a lot of support from lots of people regardless of political ideologies.

Rachael Bade@rachaelmbade

SCOOP: FDA chief Marty Makary's job is in jeopardy, as the WH considers an FDA shakeup. Two well-placed sources tell me he's likely to be axed in coming weeks — though, I'm told, nothing is final. (Worth noting: the WH's official line is still to stand by him, as I put in the story.) As WSJ reported yesterday, Makary has angered the president by slow-walking flavored vapes. But he's also upset MAHA and pro-lifers — two key parts of Trump's 2024 coalition — as well as top officials in the West Wing. The perception is that he pushes his own agenda, not the president's — and thus has gotta go. I'll be talking more about this on THE HUDDLE. Tune in at 8:30 a.m. @seanspicer @danturrentine Full post (Read & Subscribe!): rachaelbade.substack.com/p/scoop-makary…

English

The Pathfinder retweetledi

🚨 NOVO NORDISK Q1 EARNINGS

$NVO reported a Q1 results, with adjusted operating profit of DKK 32.86B, ahead of the company-compiled consensus of DKK 28.74B. More importantly, management slightly raised full-year 2026 guidance, now expecting both adjusted sales and adjusted operating profit to decline by -4% to -12% at constant exchange rates (CER), compared with the previous -5% to -13% decline range.

Reported sales rose 32% at CER and reported operating profit rose 65%, but both were heavily affected by a non-recurring 340B provision reversal in the US. Excluding that effect, adjusted sales actually declined 4% at CER, while adjusted operating profit declined 6% at CER.

The key bright spot was Wegovy.

Novo said adjusted Obesity Care sales grew 22% at CER, while the newly launched US Wegovy pill reached DKK 2.26B in Q1 sales.

The pill was launched in the US on 5 January 2026, generated around 1.3 million prescriptions in Q1, and has now exceeded 2 million prescriptions since launch. For the week ending 17 April, weekly prescriptions exceeded 200,000.

This is the good news.

Volume is clearly not the problem. Demand remains there. The bad news is that Novo’s US adjusted sales still declined 11% at CER, mainly because lower realised prices offset volume growth across the Wegovy portfolio. International Operations were better, growing 6% at CER, driven by higher volumes.

So the quarter does not particularly scream “Novo is back to the old growth story.” It shows that the market may have become too pessimistic about the durability of the obesity franchise.

The investment debate is now very simple.

Can Novo generate enough GLP-1 volume growth to offset pricing pressure, competition from $LLY, and margin compression?

That is (or should be) the whole thesis.

My take take is that this was a solid quarter relative to depressed expectations, but not a clean victory. The Wegovy pill launch looks genuinely strong, and the guidance raise matters because the market was looking for evidence that Novo was not structurally broken. But the company is still guiding for an adjusted decline in both sales and operating profit this year, which means the business remains in a transition year rather than a restored compounding phase.

As far as valuation goes and change in targeted intrinsic value, I'll post it included in a full earnings breakdown article later today.

So, in other words, Novo passed this quarter of the semester, but the final grade still depends on pricing, volume, margins, and the Lilly head-to-head battle.

Still, it's nice to see a result / reaction other than being down double digits.

What are your thoughts?

English

The Pathfinder retweetledi

$CYTK Here we go! Myqorzo ACACIA study results in nHCM --> BOTH co-primary endpoints hit with statistical significance.

There may be debate about magnitude of improvements for Myqorzo via KCCQ-CSS and peak V02. But, if you were dreaming for a double stat sig win, you got it.

Details in my story:

statnews.com/2026/05/05/cyt…

English

The Pathfinder retweetledi

$MIRM Primary Endpoint Met in VISTAS Study of Volixibat in Patients with Primary Sclerosing Cholangitis

- Statistically significant and clinically meaningful 2.72 point reduction from baseline and 1.64 point placebo-adjusted (p=<0.0001) reduction in primary endpoint of cholestatic pruritus

English

The Pathfinder retweetledi

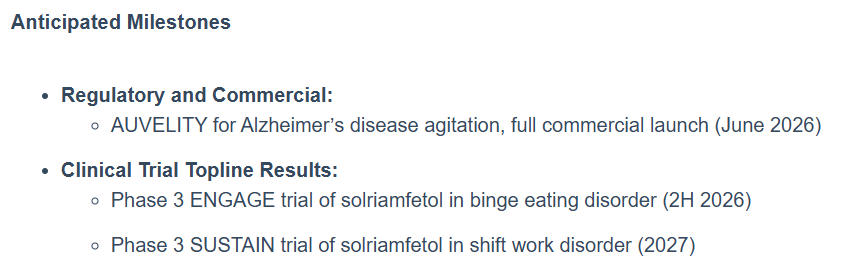

$AXSM total 1Q'26 net product revenue of $191.2M, ↑ 57% YoY.

AUVELITY net product sales $153.2M, ↑ 59% YoY.

Cash and cash equivalents $305M

English

The Pathfinder retweetledi

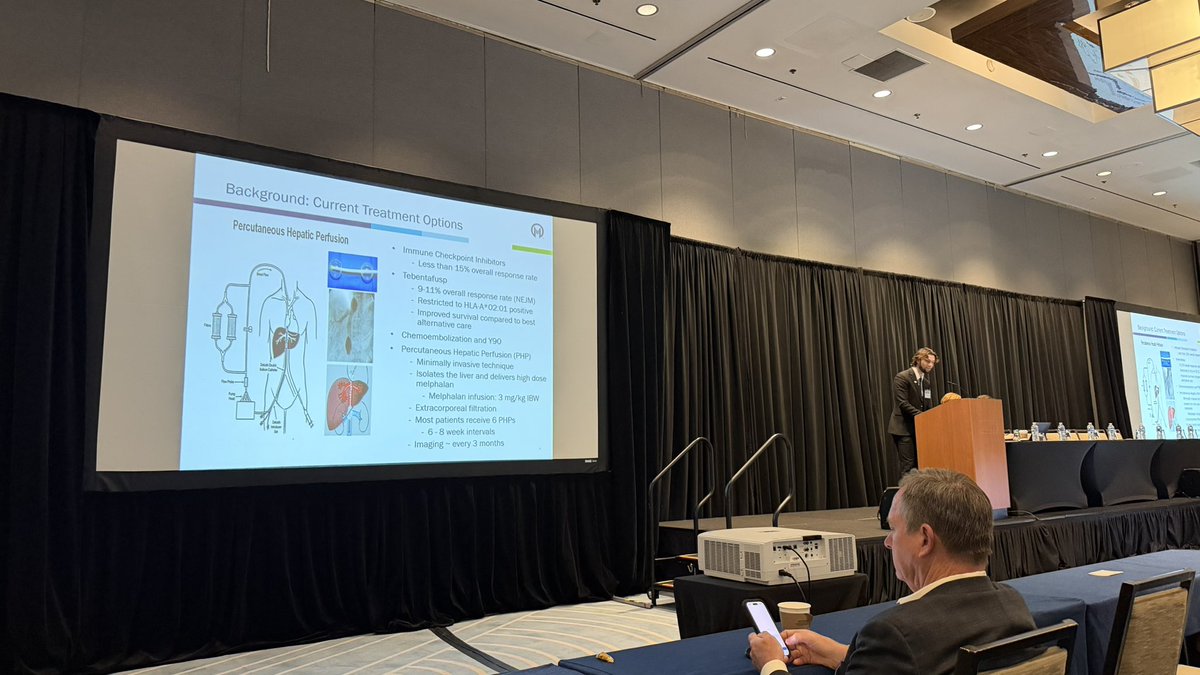

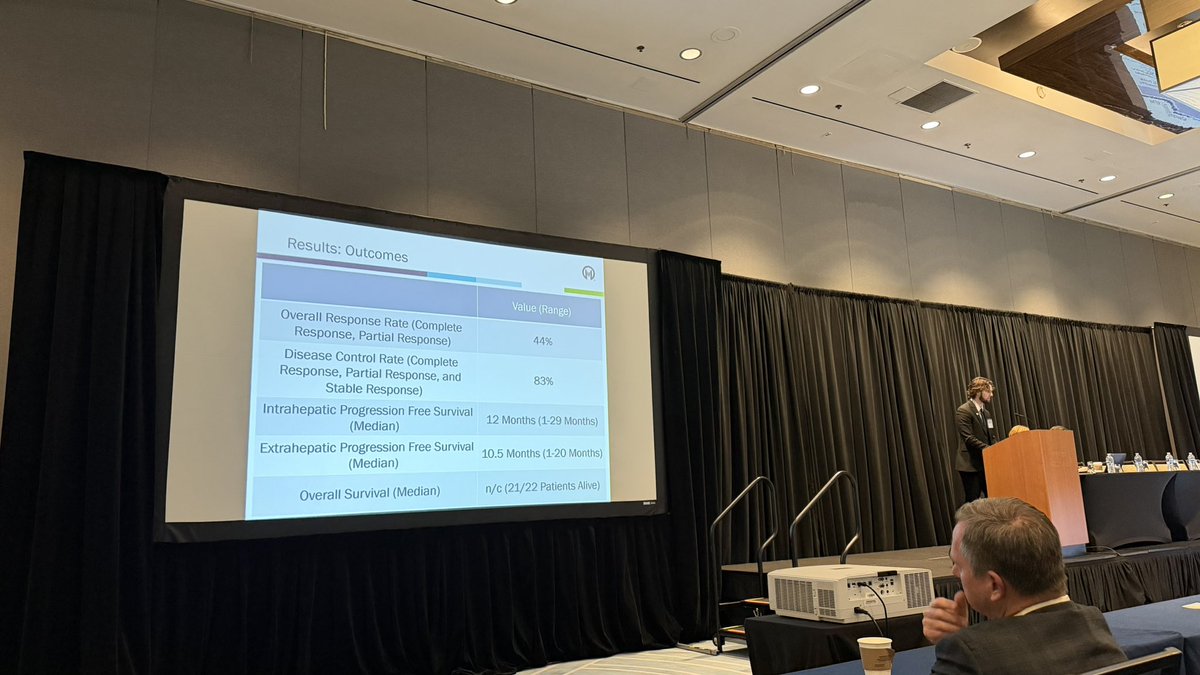

Parker Olive USFMCOM MS2 presenting @MoffittNews PHP data post FDA approval. Excellent job Parker. Even better results than the phase III trial. @USFHealthMed #ACT2026

English

@Sanctuary_Bio @Biotenic @murphycpr @Vulpescap "For You" is completely useless, never using it. getting trapped by this algo isn't a good thing

English

@Biotenic @murphycpr @path1finder @Vulpescap I dunno. The algos for me just seem way off. Following tab works...that is straightforward. For you tab is just a mess and clearly geared towards pure engagement. All that + complianced accounts and it's just...way quieter than pre-Elon taking over.

English

I'll just say

I had fun today. BioX will never reach the where it was in the good ol' days. I've accepted in my heart that is over

But as a remote worker, I don't know what I'd do without this community. A+. Fun f'ing times

Have a good night and hoping for good hockey games!

English

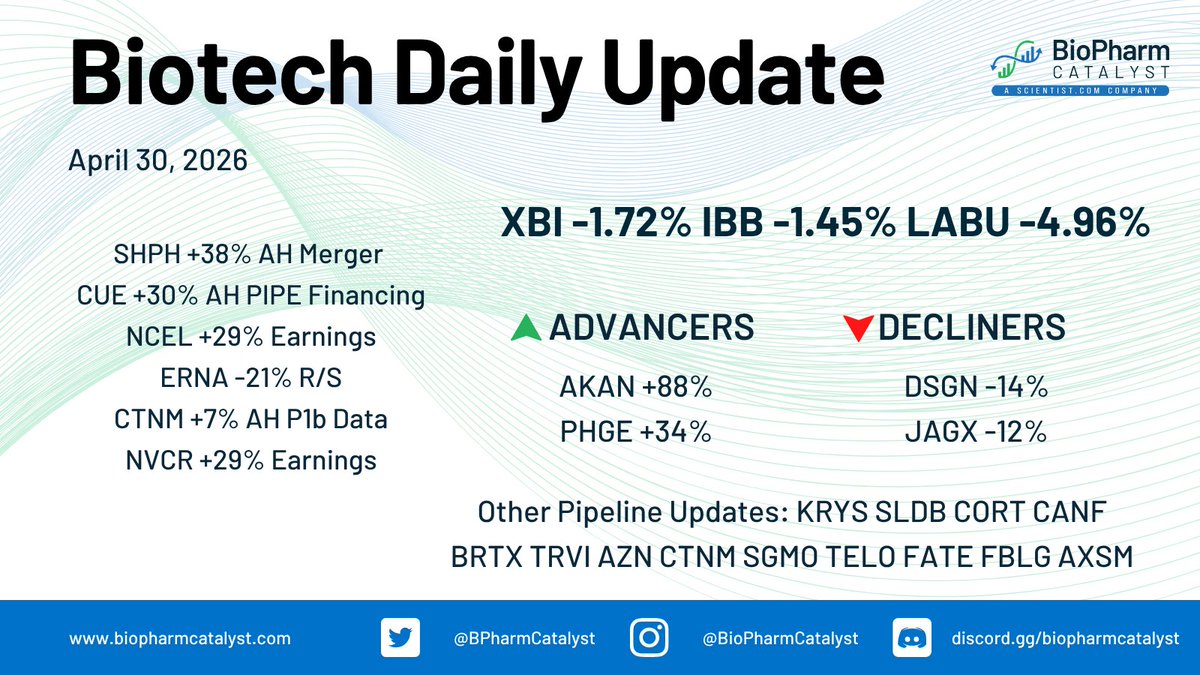

$CUE entered into a $30M PIPE financing selling pre-funded warrants for up to 2,727,272 shares and accompanying warrants for up to 1,363,636 shares at an effective price of $11.00, with proceeds to support its clinical pipeline including the recently licensed Phase 2 anti-IgE antibody Ascendant-221 (upfront $15M, up to $676.5M in milestones, plus royalties), positioning the company to initiate a global Phase 2b food allergy trial following Phase 2 CSU data in 2H 2026.

$XTLB $SGMO $KALV $LEXX $SNGX $TEVA $AKAN $SCLX $PBM $PHGE

See More Biotech Updates👇

biopharmcatalyst.com/news/2026/newc…

English

@Sanctuary_Bio @Vulpescap and more people that contributed valuable information/insights

English

@Vulpescap no premium accounts so people didn't spam feed for beer money. Search was usable. you could see what other people liked. No bots. Compliance was far less restrictive so you had quite a few inst traders sharing their thoughts much more freely

English

"but it's just cough syrup" 😆

Andre-ACGT@Andre_AGTC

Here is the press release Axsome Therapeutics Announces FDA Approval of AUVELITY® (dextromethorphan HBr and bupropion HCl) for the Treatment of Agitation Associated with Dementia due to Alzheimer’s Disease | Axsome Therapeutics, Inc. share.google/4W4DmjsHfZ4EBb…

English

The Pathfinder retweetledi

$AXSM announced that the FDA has approved AUVELITY (dextromethorphan HBr and bupropion HCl) for the treatment of agitation associated with dementia due to #Alzheimer's Disease.

biopharmcatalyst.com/company/AXSM/n…

English

The Pathfinder retweetledi

$IDYA to Initiate NDA Submission from the Darovasertib OptimUM-02 Trial under the Oncology Center of Excellence Real-time Oncology Review (RTOR) Program.

Completion Expected in 2H'26

English