Kate Kitty Wong

3K posts

Kate Kitty Wong

@pingthepingping

DeCeFi over CeDeFi | 🐧 | 🇭🇰 dyslexic lawyah turned liquidity plumber | 🇨🇦 王老吉 | 🐹 connecting dots & ppl | 🍮 ai can't replace my pudding | nfa

New York, USA Katılım Kasım 2013

4.9K Takip Edilen10.3K Takipçiler

@cyrilXBT Why write all of this and not share the GitHub, just curious! Have a great day!! Maybe this one: github.com/anthropics/fin…

English

ANTHROPIC JUST OPEN SOURCED THE ENTIRE WALL STREET WORKFLOW AND FIRMS ARE NOT GOING TO BE HAPPY ABOUT IT.

DCF models. LBO models. Equity research reports. Merger analysis. KYC checks.

All of it. Free. On GitHub.

Here is what just became available to anyone with a laptop.

Direct connections to Bloomberg, FactSet, S&P Global, Morningstar, and PitchBook.

Real Excel models with live formulas and sensitivity tables built automatically.

CIMs, IC memos, earnings reports, and buyer lists drafted on demand.

PE due diligence, GL reconciliation, and NAV tie-outs running as production agents.

This is not a chatbot wrapper that summarizes financial news.

These are production agents that own entire financial workflows end to end.

The kind that investment banks and private equity firms pay $50,000 to $500,000 per year in software licenses to run.

Now it is a one-line Claude Code plugin install.

19,800 GitHub stars.

Apache 2.0 license.

100% open source.

Think about what this actually means.

A junior analyst at a bulge bracket bank spends 80% of their 100-hour week running models, drafting memos, and compiling data across Bloomberg and FactSet.

That entire workflow just became a Claude Code agent.

The banks charging clients $500 an hour for analysis that this system produces in minutes are not going to tell you this exists.

The boutique advisory firms charging $50,000 retainers for due diligence work that these agents handle autonomously are not going to promote this repo.

But it is already live.

19,800 people have already starred it.

The window where knowing this gives you an edge over every analyst, associate, and advisor still doing this manually is open right now.

Star it. Fork it. Deploy it this weekend.

Bookmark this before your next financial model.

Follow @cyrilXBT for every open source release that disrupts an overpriced industry the moment it drops.

English

@0xNairolf I thought it's local Stablecoins solving real world problems mbmb

English

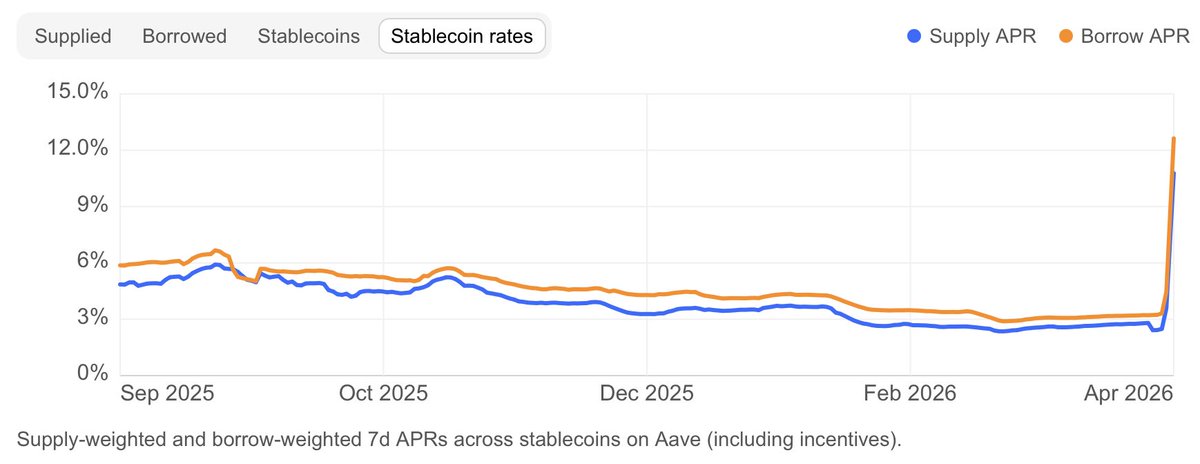

Aave's stablecoin lending pools are at 100% utilization for ~3 days. Billions withdrawn. LPs can't exit. Borrow won't budge.

This isn't the rsETH hack spreading. It's a governance-set rate ceiling like price control, a market failure coded in Solidity. 🧵

1/

English

@gordonliao How come they don't withdraw and borrow somewhere else that's cheaper 👀

English

Why the market fails?

Some borrowers have locked up wETH and go for exit with stablecoin borrows. Marginal borrower still runs leveraged strategies with returns at 25-40%+. 14% cost of funds, still in the money

Supplier sees insufficient compensation for 0 liquidity, leaves

4/

English

Tokenized bank deposit reminds me of DeFi bridges ... So u can double count ur TVL 👀👀👀

English

So ... Which curators on @Morpho is licensed ... Bitwise?

Cointelegraph@Cointelegraph

🇺🇸 JUST IN: SEC says certain crypto interfaces, including DeFi front-ends, wallet extensions, and apps, may operate without broker-dealer registration under conditions: • No custody of user funds (self-custodial only) • No investment advice or recommendations • No order routing or execution • Fixed, neutral fee structures only • No discretion over transactions or market activity

English

Everyone debates: @cz_binance

👉 “When will quantum break crypto?”

Wrong question.

The real risk is already happening:

👉 Harvest Now → Decrypt Later

Meaning:

• Encrypted blockchain data today = permanently stored

• Once quantum is viable = old signatures can be broken

• Funds from old wallets = exposed retroactively

This includes:

👉 Early BTC wallets

👉 Dormant ETH wallets

👉 Any reused public keys

So even if quantum arrives in 5–10 years…

The attack surface already exists TODAY.

English

@bryan_johnson thanks for making everyone DM me about this tweet =)

English

. @Visa launches Intelligent Commerce Connect — a unified on-ramp for AI agents to make purchases using tokenized credentials. 100+ partners building, Santander Bank already live with it in 5 LatAm markets. What's the actual infra stack?

> Visa published an MCP server on GitHub bridging LLMs directly to payment APIs

> AWS integrated via their Bedrock AgentCore with retail + B2B agents

> Stripe now supports Visa's Shared Payment Tokens alongside Mastercard Agent Pay — first provider doing both networks for agents

> McInerney (Visa CEO) calls it "the convergence of AI, tokenization, digital identity, stablecoins"

> Visa also launched Trusted Agent Protocol (Oct 2025) to distinguish legit agents from bots

> likely >> Visa is positioning as the universal trust layer for agentic commerce — not owning agents, but owning the credential/risk infrastructure agent depends on. The MCP server move means any LLM can plug in natively. Stripe as middleware, Visa as rails.

x.com/pymnts/status/…

English

Rezolve (processed $1B in USDT through Brazilian retail) expanding into AI agents check out infra targeting North America and Europe @RezolveAi ... what agentic rails are they running on?

> CPO David Ingram says protocol-agnostic

> website claim to be built around their own commerce-native AI layer

> but Rezolve acquired Subsquid (and Smartpay)

> earlier blog post mentioned x402 × SQD × Rezolve Ai alignment

> likely >> x402 handles per-request agent payments, Subsquid providing on-chain data for inference, and Rezolve provides the enterprise commerce/checkout layer

English

@cryptoxiao docs.morph.network/docs/morph-rai…

You are missing these skills 👀👀

English

宣布一件大事,我们把 6551 的X + 全网新闻源MCP + SKILL 开源了!

很多人说,6551 的新闻源、推特面板很好用就是消息太多看不完。

还有很多朋友跟我说 X API 太难接,Skill 学不会,折腾半天龙虾就是跑不起来。

今天直接解决,我们把我们积累了1年的数据基础架构全部打包成 MCP + SKILL,任何人都可以几分钟部署,24h帮你看新闻。

🦞 你的龙虾现在可以:

• 直接连上 X 数据 + 全网50+实时新闻+链上数据,不用配 API 密钥。

• 24h 监控、分析、触发tg提醒。

照着 GitHub README 部署,几分钟就能装好。

欢迎大家安装试用和分享体验,有问题及时反馈及时迭代。

也欢迎👏🏻有热情的 dev 参加我们的生态

MCP

github.com/6551Team/openn…

github.com/6551Team/opent…

SKILL

clawhub.ai/infra403/openn…

clawhub.ai/infra403/opent…

中文

No analysis is going to work when Trump can destroy the chart and setup with a single speech.

English

@jony_levin Your judgement is clouded by the lessons learned; cmd a delete; now go and pick an ai stonk with ur gut feeling

English

For the longest time I couldnt understand why would any merchant need a POS machine to accept crypto payments and why products like wallet connect pay even exists ...

>> 1. encoding the amount, asset, destination address, and compliance metadata so the customer just scans and confirms

>> 2. Don't need to care about which chain or download a new wallet. The POS SDK supports EVM, Solana, and Tron from day one and is compatible with 700+ wallets.

>> 3. standardized payment states like PaymentCreated, PaymentRequested, PaymentProcessing, PaymentSuccess, PaymentError, for customer handling and proper accounting.

>> 4. No new hardware required. The integration works on existing Ingenico Android-based POS terminals, which have over 40 million devices deployed across 120+ countries it's just another payment method alongside cards.

>> 5. Fiat settlement option.

"Pick a simple problem and solve it so well that no one else can" hmmmmm 🤔

WalletConnect@WalletConnect

WalletConnect Pay just got a lot BIGGER. WalletConnect Pay is now supported across a range of wallets. Just announced live at WalletCon Cannes 2026. Here's who's in. ↓

English

Everyone is focusing on the “6 red months”…

But that’s not the real signal.

The real question is:

👉 What kind of market produces 6 consecutive red monthly closes?

Because historically, that doesn’t happen in random conditions.

It happens when:

• liquidity is tightening

• sentiment is completely washed out

• weak hands are fully exhausted

In other words — late-stage compression, not early-stage weakness.

In 2018, that exact setup marked the end of distribution* and the start of re-accumulation.

Not because “history repeats”…

But because markets move in cycles:

👉 pain → apathy → positioning → expansion

And 6 red months?

That’s deep into apathy phase.

Now look at today:

• Institutions are already inside

• ETFs changed the demand structure

• Supply is more illiquid than ever

• Retail is… mostly gone

So even if the *pattern* looks similar…

The underlying structure is completely different.

That’s why blindly expecting “+300% in 5 months” is the wrong takeaway.

The smarter read is:

👉 The longer the compression

👉 The more violent the expansion

Most people will wait for confirmation.

But by the time it’s obvious…

The move is already halfway done.

History doesn’t repeat.

But liquidity cycles do.

And right now, we’re closer to the end of pain…

than the beginning of it.

#Bitcoin #Crypto $BTC

English

@minchoi Does it work on nother screen if I keep scrolling down 👀👀👀

English

KOL trip Day 2 with @Binance_TH_ 🍷

Yesterday: risk management on ropes

Today: risk management on wine 😏

Now at PB Valley, Khao Yai 🇹🇭

wine tasting + lunch with the squad

Who knew crypto trips come with this kind of lifestyle?

#TouchGrasswithBinanceTH 🌿

#BinanceTH

English

KOL trip kickoff with @Binance_TH_ 🚀

This morning we assembled at CRC Tower, All Seasons Place — ready to head to Khao Yai 🇹🇭

Black & yellow everywhere 🟡⚫️

Builders, creators, and community all in one place

Day 1: Adventure + After Hours

Day 2: Keep building

Not just a trip…

this is how #BinanceTH connects IRL 🔥

#TouchGrasswithBinanceTH

English