Investor

65 posts

Investor

@pricing_power__

Analyst turning over rocks [email protected] https://t.co/9TabDExgoV

Katılım Aralık 2017

705 Takip Edilen1.8K Takipçiler

Gaurav Kapadia showing us all how it’s done

TBU@TBU12345678

the one thing I like about the OG Tiger Cub guys is that they really live/lived "the life". PJs, Augusta memberships, the best wine, epic houses in the Hamptons. for whatever reason the pod guys never picked up high class tastes, even with the big share shift of $

English

@WaterworldCapi1 @tangentstyle Think cprt a short here? Rba saying they want to get to 50% share from 40% aka 30% headwind to cprt volumes. Cprt not super cheap in absolute terms in that context.

English

Much ink was spilled over IGSB’s track record a few years ago. Few people know how software will unfolds but igsb is staking a claim that software and services will be increasingly commingled. What this means for legacy saas? Idk. Excited as a bystander to see how this unfolds

English

Is it a coincidence that both initiatives are in services, wealth and property management?

Id put money on there being a plan to infuse both of these business models with tech. They've already started sharing what this vision may look like in wealth and their Riviera product

English

Investor retweetledi

few $FIG / design workflow thoughts

wont get into most recent quarter - but you should be asking about whether there were any one-time tailwinds from (1) starter -> pro upgrades (MCP tool call limits + daily Make credit limits on starter that don't exist on Pro/Org/Ent) and (2) seat increases from "ghost" seats as cheaper to buy an extra pro seat than buy AI credit add-on. and (3) note the risk factor changes re Make margins

the big shift that will drive stock / longer term demand is how well FIG adopts to the new world = coded design components > visual components

– at its core, Figma is a translation tool to bridge what designers want to build and what developers actual build. the end goal is to generate the right code

– FIG was crucial in the design flow bc it was multiple times faster / easier to adjust UI using drag & drop on their canvas, vs do this in code

– AI tools have made it just as fast to design with code, and make edits with a single prompt. code is native to LLMs

there's a reason why design workflows start with prototyping right now. skips the tedious sketching out of screens and enables teams to get to the end "vision" quicker

– teams are now going backwards into Figma to build out the design file due to org inertia and process

– this process is broken - you built a working thing, then documented it in a static mockup tool, so then it could be handed to developers to rebuild it

– the middle step is redundant and gets solved if either (1) org inertia breaks down and processes emerge around the prototype vs Figma file, (2) the prototype can be created with high fidelity referencing a coded design system and with code that is high quality enough to be directly pulled into a MR/PR and moved into CD dev process, or (3) better yet if the prototype is built on existing code base

code is the end goal, and appears to be the new source of truth in design. as roles converge (PM, designer, engineer), this could become the natural path

English

Investor retweetledi

Remitly may blow away street projections for 2028. In lower opex growth scenarios - consistent with current trends & the new CEO's comments about AI & maintaining a flat headcount over the next few years - there’s tremendous room for upside vs guidance. $RELY (1/x)

English

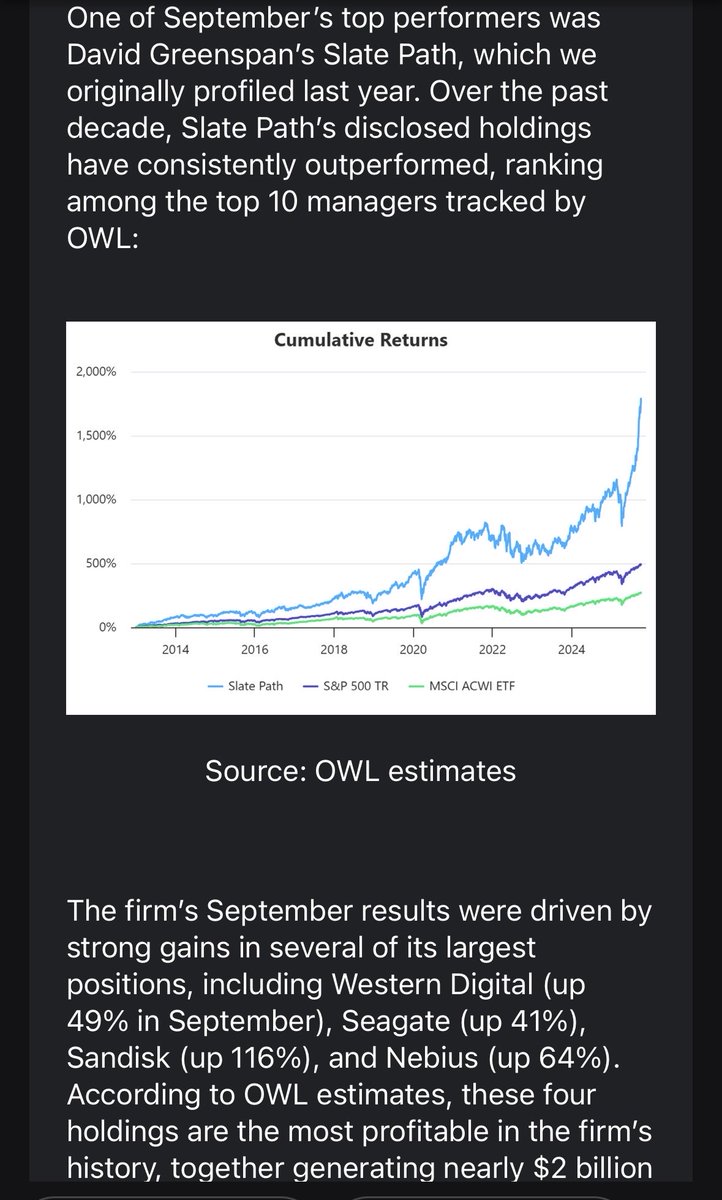

@west4thstreet Huge in WDC, SNDK, MU, WBD. Actually insane. AUM has prob 2-3x’d on returns alone

English

Slate Path returns the last couple years have to be incredible

English

@TechFundies Ya I agree & been thinking about this given alphasense token ramp and spgi lseg all discussing mcp growth

Pushback would be ease of replicating this data and declining switching costs so even if consumption revenue is a short term uplift, does it rerate

Investor@pricing_power__

threads im interested in exploring: market data consumption

English

Random thoughts after connecting $FDS to Claude Chat / Cowork.

My thinking is I want to approach AI as a typical user for investment advancement and use the learnings as a proxy for SaaS (as opposed to judging the impact of AI on FIG which I have never used before). Investment management likely downplays the importance of collaboration functionality in enterprise SaaS since most investment ideas are run from start to finish by a single person w/ just the end product being shared with a committee.

1. Connectors take Claude to a whole new level. By adding $FDS, I now get reliable data which takes my trust and application of AI much further.

2. Trying to replicate old, working things is frustrating. I tried to have Claude replicate my Excel quicksheet which is built with $FDS excel codes. It sort of worked but then I realized it was just very buggy and hard to get working as reliably as my spreadsheet. And then I asked myself why I was spending money and time working on rebuilding something that already works well. Same applies for $MSFT apps – can just connect to them and work on spreadsheets, emails, etc.

3. Building new stuff is easier and cool. I quickly prompted it to build an artifact that pulls the tech universe and helps me parse which businesses are accelerating. I then quickly prompted it to run the same analysis but by subsector. I think the data is likely correct and could quickly visualize the market’s enthusiasm for semis and avoidance of application software (see image). The new stuff is what I think everyone should be excited about. It’s new functionality, analysis, insights that can allow me or a business to advance and outperform competition.

4. The fastest, most efficient way to get to new functionality is via incumbent data / sw providers. I can pay more for $FDS MCP and am good to go. No change to existing processes or loss of procedure. Just ready to work on new things. I could purchase MCP from a smaller vendor but most of their data is incomplete right now. I could switch to CapIQ or Bloomberg but A) they are just as if not more expensive, B) Bloomberg doesn’t have an MCP yet, C) I would have to switch all the old stuff too / recontract which is just a waste of calories.

5. $FDS hasn’t had anything new to sell me ever. Now they do and it’s hot. Now maybe the flipside is the MCP can be swapped out for a competitor more easily which commoditizes the offering – particularly if all the old stuff moves entirely over to Claude over time but that seems very unlikely just given how people work (evidence: Bloomberg is the most legacy tech out there and has very low churn bc of habit).

6. Should I be paying more to access $FDS data via an MCP? Arguably not since it’s just another way to expose the same data and my usage of the terminal will likely lose share of time spent. But, whatever, the spend is a very low percentage of the business and not having it just seems stupid. Can you imagine meeting an investor and responding that you don’t have clean financial data in Claude because you’re too cheap (not to mention most funds expense this to the investor anyways!)? My point just being I think people are ultimately going to spend more to get more, and will be fine with it bc of the value add. I think the same thought process applies if I were starting a new firm – why would I want anything other than the most comprehensive data set to power my AI? Jeopardizing ROI to save a bit of money makes no business sense.

7. I did some market research. CapIQ said the inbound inquiries for their MCP is “through the roof, insane, etc.” w/ per seat pricing going up by 30-50%. $FDS per seat increases are probably similar to a bit less than that.

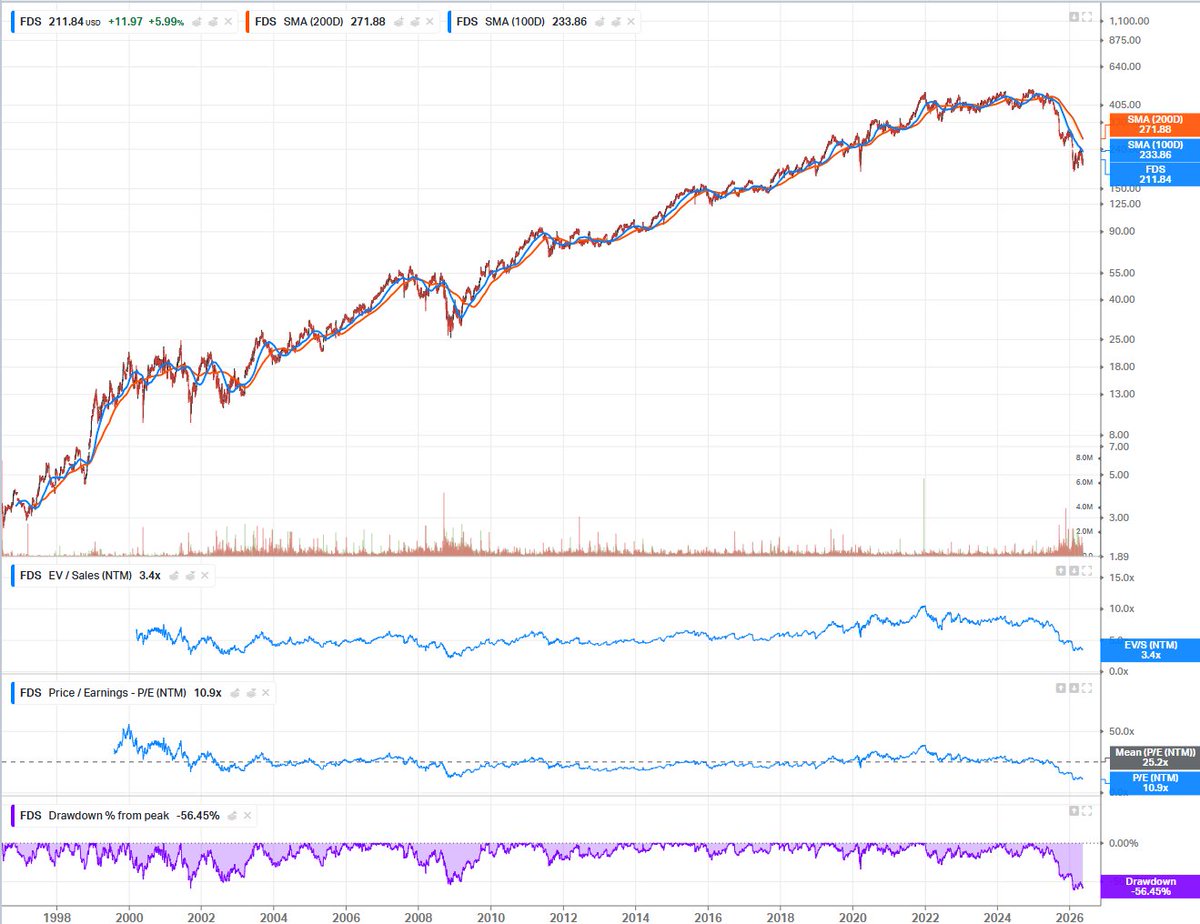

8. $FDS has been accelerating the past 3 qtrs w/ msd growth, and I would guess that continues given MCP ramp. Margins are a bit low while re-investing in product which is a sensible thing. Stock trades at 12x this year’s GAAP EPS / 12x FCF. Stock once traded down to 14x GAAP EPS in 2008 when the financial world was ending and finance professionals were being laid off. Stock has never had a worse peak-to-trough drawdown than now. And it’s never been this cheap.

Please throw rocks at this.

English