Sabitlenmiş Tweet

The next Warren Buffett, if there will ever be another, will not be found at the Berkshire annual meeting.

English

Peter Sterky🇺🇦

632 posts

@psterky

Trift Capital. xCFO Spotify. Actively hiring outstanding forward-leaning curious analysts - positions open.

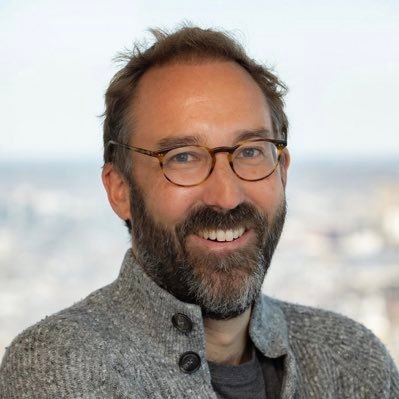

Ended the year around 35% reinsurance rate. On track to 20%. Gemini said bigger insurers are <15%. I expect Lemonade to be around 5% in the next 5 years due to better underwriting and bigger balance sheet. Something I think worth tracking.

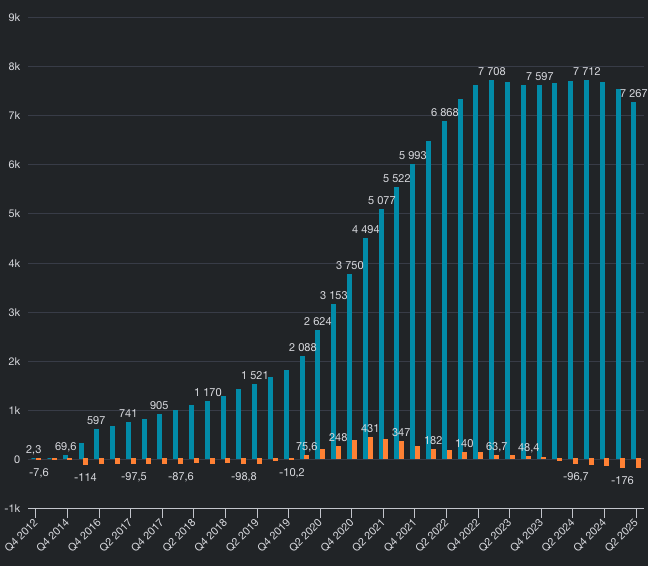

Holy shit The $SoFi CEO just bought $1 million of SoFi shares