ql

295 posts

UNI still performing flat / outperforming broader altcoin / defi universe (+25% last 30d) despite this arguably pretty bearish development coming from the last-ditch attempt to boost revenues by expanding fee switch to base and other L2s

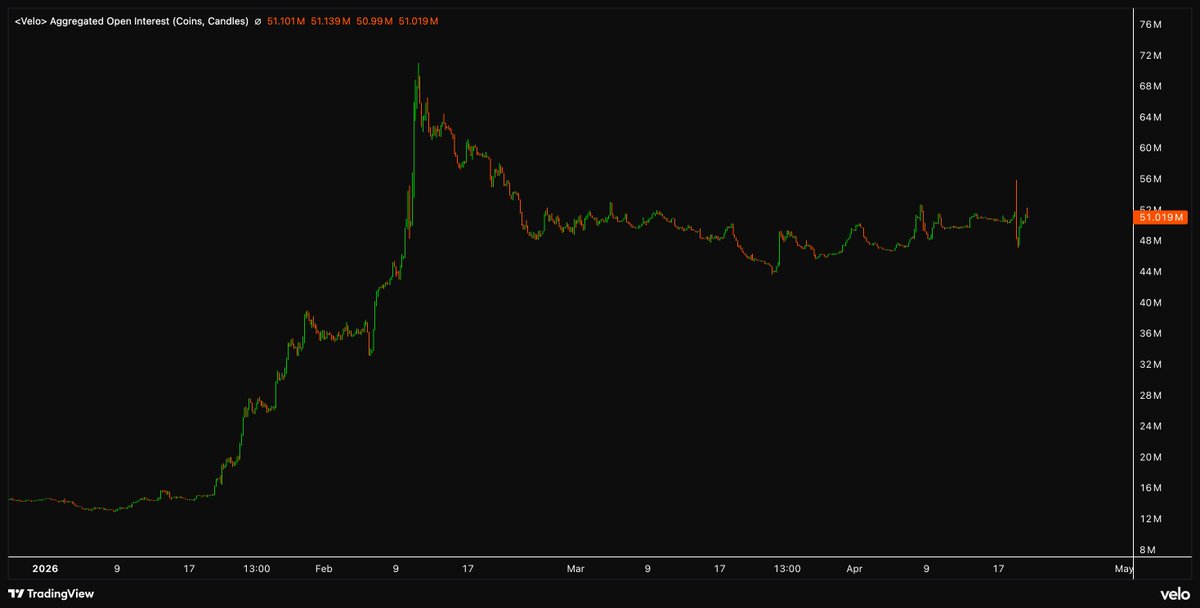

coin-denominated OI spiked around the same time this news broke indicating some positioning build up which hasn't yet been fully unwound

wondering whether we are due some UNI underperformance if the drop of in LP TVL and lack of impact on revenues continues, at least until OI is back to pre-announcement levels (driven by residual perp positioning unwind)

there's still about 2.2M UNI ($8.8M) more OI / positioning than before the announcement which has the potential to be gradually unwound now - also maybe worth comparing this OI delta vs wider market OI and normalising for that to ensure the residual OI is specific to UNI and not general altcoin / defi token OI buildup

UNI/BTC still 5% above where it was before the news but in fairness has retraced a decent amount since immediately after so the juice probably wouldn't be worth the squeeze for any sizable short position but I do expect it to unwind at least the remaining 5% of outperformance vs BTC if not more

one more point to add on this is that there is a notable lack of future catalysts in the pipeline for UNI, as a token in structural decline with the proliferation of more specialised prop AMMs and the compression of fee capture on stable / high-volume pairs (which are uniswap's bread and butter)

the one tail risk here is the blackrock investment, which I feel may have been slightly overlooked, but the sheer volume of institutional partnership headline announcements these days massively dilutes the likely impact of this on price anyway

this analysis is from a few days ago so forgive the charts being slightly stale - UNI/BTC is down 8% since then but still think there is some underperformance left given OI hasn't fully reverted

jpn memelord🛡️@jpn_memelord

So the Uniswap fee switch did significantly cut Uniswap v2 volumes on Base. Before March 7: $55m - $100m volume. After March 7: $35m -> $24m volume. And still over 90% of this does not actually pay into the protocol fee because it comes from rugs.

English

ql retweetledi

hey guys this might be of surprise to you but if you pay fees for volume or liquidations on some random pre tge perp dex you're buying locked plasma and not 95% discounted cheap hyperliquid beta

English

ql retweetledi

this is some real Japanese soldiers on the island type stuff

Troy 🟪@troyharris__

Open interest across Hyperliquid and Lighter ended yesterday at the lowest its been since Oct '25 . Volume on Hyperliquid has seen a notable uptick over the last couple of weeks. Meanwhile, Lighter had its highest daily volume since its TGE.

English

remember when you were saying the same bearish spiel about future cash flows at the pico bottom 65% lower?

one of the loudest voices on here about fundamentals and archaic legacy valuation methodologies, but when a clear disconnect between fundamentals and PA presents itself you're vocally fading the bottom

in an asset class where the most predictive indicator of price direction is beta, looking at arbitrary multiples in isolation has essentially 0 ability to predict future returns

English

@Crypto_McKenna what about hyperion HYPD?

seems like they’re doing more interesting stuff with the HYPE they accumulate like allowing projects to use it to deploy HIP-3 markets and taking some of the fees etc

English

Believe Hyperliquid Strategies is going to perform exceptionally well over the next 12-18 months.

In fact I believe it's going to outperform HYPE across that timeframe. HSI is the MicroStrategy of the fastest growing revenue generating blockchain lead by exceptional asset managers.

Team are remaining incredibly diligent in their deployment of cash raised. HSI alongside the BitWise spot HYPE ETF will remain the Institutional gateway to Hyperliquid.

$PURR

English

in this case - I suppose you are correct to say that the MM fees aren't priced into the spread

but they are to some degree priced into the realised execution slippage caused by adverse selection and toxic fills from the asymmetric latency

the degree to which this is true is still yet to be seen - it's still entirely possible that the average slippage is still less than the hyperliquid fees

but I am assuming that this data uses static orderbook snapshots to estimate the slippage, which fundamentally fails to capture the temporal impact of tiered latency (which doesn't exist on hyperliquid) on realised execution slippage

English

ql retweetledi

surely including the impact of latency is the whole point though?

correct me if I’m misunderstanding here, but isn’t the heterogeneity of latency what causes worse execution for basic tier traders at a structural disposition to toxic fills / adverse selection on Lighter?

i.e on Hyperliquid in theory, your execution wouldn’t be any worse as a result of adverse selection alone, even if the latency was greater, because it’s uniform across all participants, meaning you can’t be adversely filled as a result of the counterparty having access to lower latency

English