Ramana retweetledi

You started a SIP in 2005. By 2007, you felt like a genius.

Your ₹10,000 monthly SIP in SBI Large & MidCap Fund was up 66% in just two years.

"This is easy," you thought. "Why doesn't everyone do this?"

Then 2008 happened.

Yr 3: Everything changed.

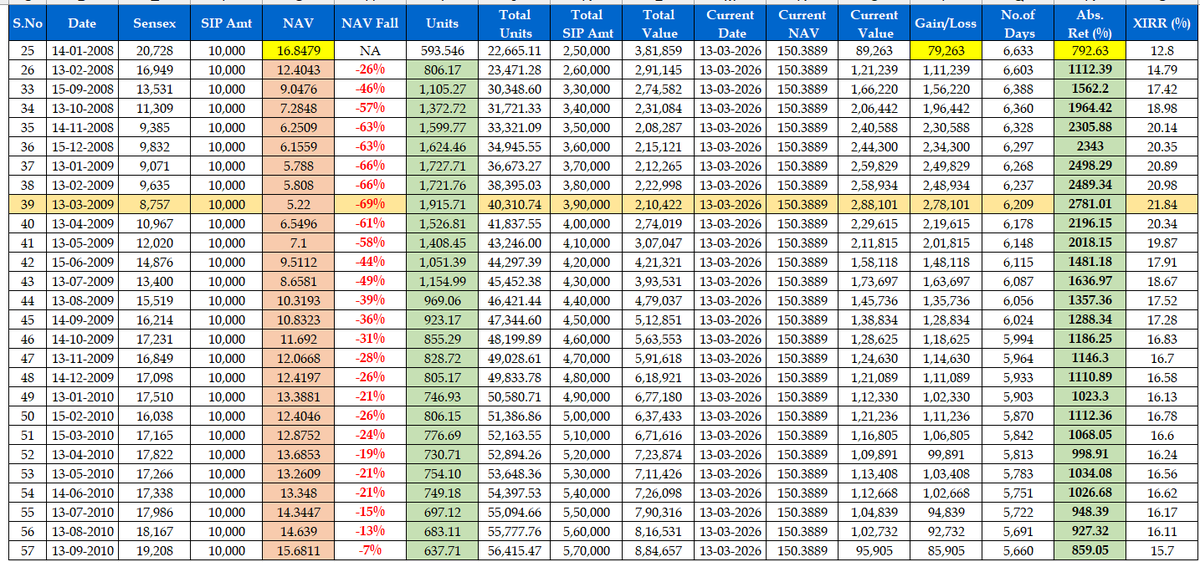

The same fund that gave you 66% returns now showed -22%.

Your ₹3.6 lakhs invested dropped to ₹2.55 lakhs.

All the profits from the first two years? Wiped out.

Doubt creeps in:

"Should I stop my SIP?"

"Did I make a mistake?"

"What if it falls further?"

But here's what actually happened next.

If you had stopped in 2008, you would have locked in your losses. Permanently.

But if you continued?

2009: Markets recovered. Your portfolio bounced back to ₹6.74 lakhs.

2010: It grew further to ₹9.57 lakhs.

By the end of Yr 5, your ₹6 lakhs investment was worth ₹9.57 lakhs.

The same portfolio that showed a loss in Yr 3 was now up by over 50%.

Not because you timed the market. Because you stayed invested when stopping felt easier.

Yrs 6–8: Nothing happened.

From 2011 to 2013, markets moved sideways. No big gains. No excitement.

Your returns were stuck between 6–10%.

Another test:

"FD gives 8% with no risk. Why stay in equity?"

If you had stopped during these boring years, you would have missed what came next.

Yrs 9–10: The patience paid off.

2014: Your corpus crossed ₹23 lakhs.

2015: It reached ₹26 lakhs.

The 6–10% yrs weren't failures. They were accumulation phases. You were gathering units while markets were quiet.

Yrs 11–20: The explosion.

At Yr 10, you had ₹26 lakhs.

By Yr 15 ₹50 lakhs.

By Yr 20 ₹1.38 crores.

It took 10 yrs to build ₹26 lakhs.

The next ₹1.12 crores were added in just 10 yrs.

That's not linear growth. That's compounding.

What if you had stopped?

Stopped in 2008? You'd have booked losses.

Stopped in 2011? You'd have missed the 2014 rally.

Stopped in 2018? You'd have missed the post-COVID surge.

Stopped anytime? You'd have broken the compounding chain.

RUPEE COST AVERAGING AT WORK

Every fall, 2008, 2011, 2018, 2020 — your SIP kept buying.

Lower prices meant more units.

Those units became the fuel for the wealth created later.

Unwanted volatility isn't your enemy. It's your silent accumulator.

What This 20-Yr Journey Teaches Us

Yrs 1–5: Markets test you. Don't stop.

Yrs 6–10: Markets bore you. Don't quit.

Yrs 11–20: Markets reward you. Don't disturb.

Why did this fund work? Because it had structure, not just luck.

When we evaluate a fund, we check:

Rolling returns: Did it beat the benchmark consistently?

Consistency: How often did it outperform? (>70% is our filter)

Risk-adjusted returns: Was the volatility worth it?

This fund passed. But not every fund will.

Selection + Patience = Wealth.

A ₹10,000 SIP doesn't build wealth in 5 yrs. Or even 10.

It builds wealth when you stay through the falls, survive the boredom, and let compounding do its job.

Not through timing. Not through luck.

Through the process.

English