@Gubloinvestor I cannot agree you more, Canada worker being tax so much, they treat hard workers as slave.

English

robert chen

26 posts

别因为短期暴跌痛苦, 你的肉体没有受到任何伤害, 坚持到3.18美光,坚持到4月底存储集体发q1财报。

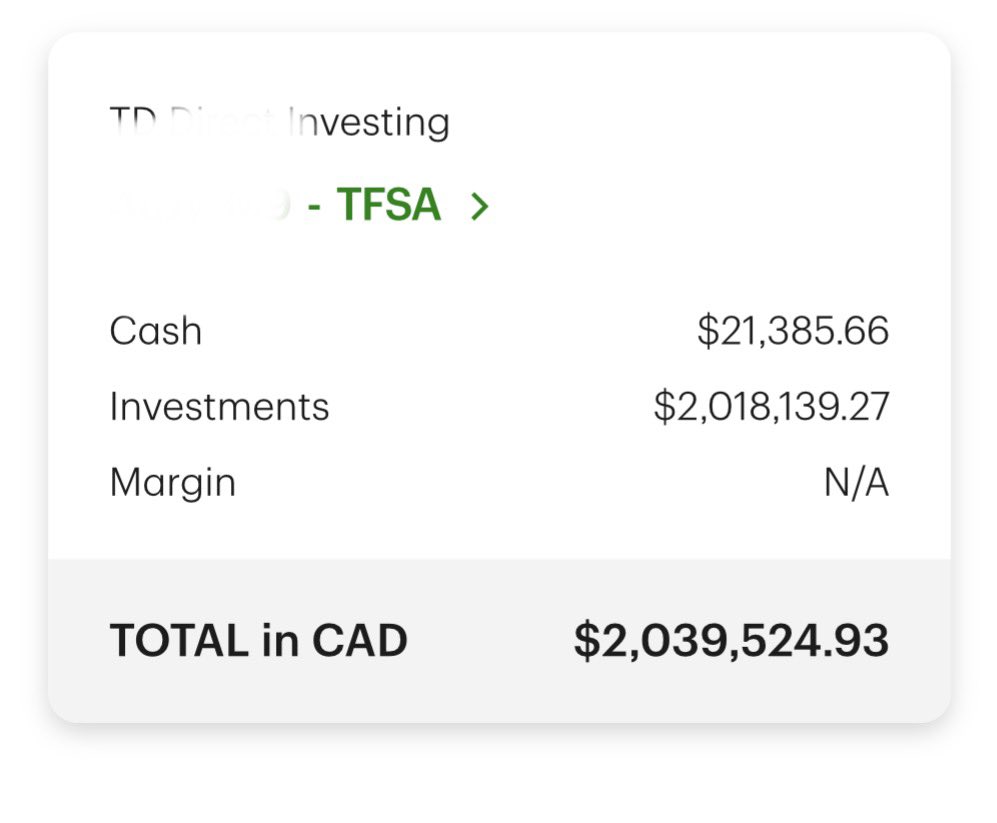

Big milestone reached - over $1,000,000 in my TFSA account It’s a Canadian tax free account, the cumulative maximum contribution is $102,000 and all gains are tax free. The Canadian Tax Agency monitors accounts and out of 17.8M accounts about 350 have balances over $1M That puts me in the top 0.002% of TFSA investors!

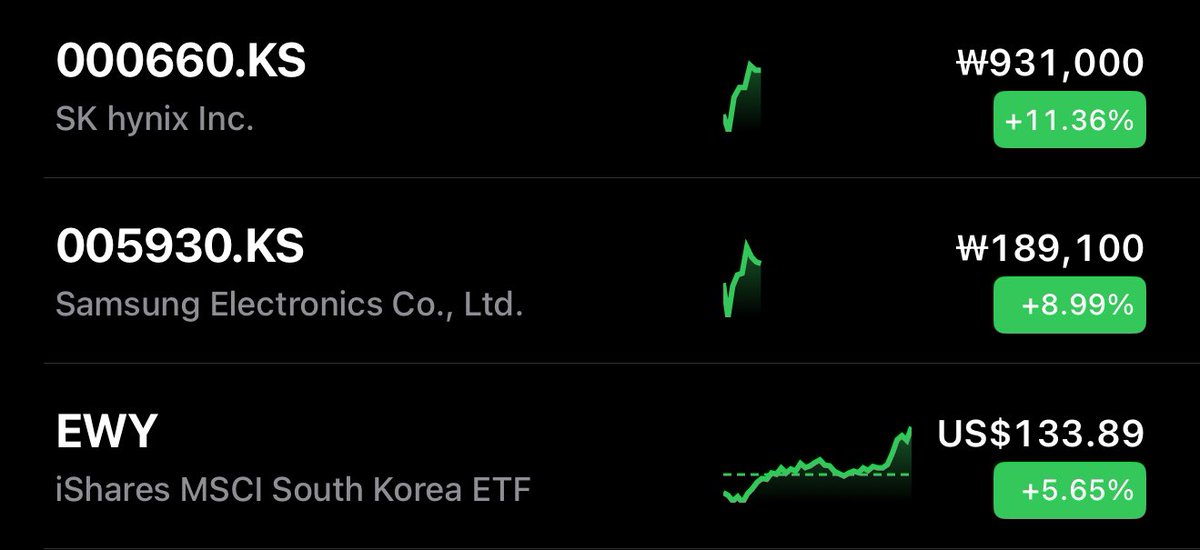

The sentiment around KOSPI | $EWY (SK Hynix / Samsung) on Crude Oil / LNG / Helium either: Disrupting Supply or Compressing Margins are overblown. The supply chain disruption and energy cost threats to SK Hynix, Samsung are sensationalized noise. Here's why: 1. Crude Oil: The a likely scenario if oil prices increase 31% and oil floats to $120/bbl: In this case, the effect on oil has almost no material impact on SK Hynix and South Korean memory equities. There are increased energy costs via oil-pegged LNG/JKM prices on Korean equities, mainly for companies surviving on razor-thin 5% to 10% margins. However, a KEPCO 70% rate hike has little material affect on Samsung/SK Hynix, given memory prices have soared with Samsung doubling NAND prices Q2. From disclosed financial from, their SK Hynix's annual electricity bill exceeds ₩1 trillion per DIGITIMES (~$750M). Which against FY2025 revenue of ₩97.15 trillion represents roughly 1–2% of revenue. SK Hynix posted a 58% operating margin in Q4 2025. Against this backdrop, the energy cost shock is small: If we model a 50% increase in energy costs: - Hit to SK Hynix quarterly OP (₩19.17T): ~₩134 billion-~₩146 billion (0.76%) - Hit to Samsung DS quarterly OP (₩16.4T): ~₩407 billion (2.4%) Every 50% energy cost spike would shave roughly .7% off SK Hynix margins and 2.4% off Samsung operating margins. Analysts project SK Hynix margins could reach 70%+ on conventional DRAM in 2026. Energy costs do not meaningfully threaten Korean semiconductor operating margins, even if they were to increase by 100%. However, this is material to companies with low operating margins of 5-10% The Losers: Traditional heavy manufacturing (steel, basic chemicals, standard flat glass). The Winners: Samsung/SK Hynix. The main risk is second-order effects on supply chains such as increased material costs. This is very hard to model, but in an example where: an industrial company forces 30% price hikes on raw materials (chemicals, specialty gases), it barely dents the fabs. Materials are roughly 15-20% of semiconductor COGS, so mathematically, a 30% spike in material costs only shaves an additional ~2% off SK Hynix's operating margins. A combined 3-4% direct (utilities) and indirect (materials) energy headwind is easily absorbed by an oligopoly printing 70% margins (and increasing prices). In majority of cases, the costs likely get passed down to hyperscalers through NAND/DRAM price hikes. In the very worst case scenario of oil prices increasing 3x or 5x. The main affect on oil increasing hundreds of percent are two factors: - Global macroeconomic shock, causing global inflation (affecting every single company, from $GOOGL to $COST). - KRW (South korean Won) USD/KRW exchange rate blowout. KRW depreciation from sustained high oil is a real second order risk, but historically Korean memory exporters benefit from won weakness on the revenue side. The majority of Samsung/SK Hynix sales are dollar denominated wheras costs are won denominated. So a weaker KRW is actually margin accretive for exporters, which partially offsets the energy cost headwind. But in an extreme case of oil prices hiking 5x, the only longs in that apocalyptic world are crude oil itself, defense contractors like $LMT / $NOC, domestic US energy producers, and the US Dollar. This is unlikely to happen. The financial media and algorithms will likely panic, but , if crude oil goes from $91 to $120 and KEPCO increases energy costs: The data shows there's little affect on Samsung / SK Hynix in specific, and the main impact are on players with razer-thin operating margins. 2. LNG: If the Hormuz closed, the majority of South Korea’s LNG imports would be unaffected. The media has been quoting Hormuz + LNG flows going to China, INdia, SK, and Japan. But if we look at the trade data from South Korea, that’s just a fraction of their total imports. Majority of imports arrive via Hormuz free routes, eg. Australia (24.6%), US (12.2%), Malaysia, Indonesia (~20%), and Russia/Sakhalin (~4.6%). Then the rest filled in with minor sources from Nigeria, Peru, Brunei, PNG, etc. The 82% of 2024 important were long term contracts that were oil-indexed, and as we've modeled above, increasing energy costs would hurt opex by 1-2% per 50% increase, but given DRAM/NAND price hikes and operating margins hitting 70%+, this would make a very little dent. Even if they did, costs would be passed onto hyperscalers. South Korea learned their lesson from 2022 and diversified sources, and there's little impact on LNG supply disruption. The main concern is oil impacting hiking of LNG. 3. Helium: SK Hynix statement: “Long secured diverse supply chains and sufficient inventory" of helium. "Therefore there is almost no chance that the company will be affected [by helium]. The reality is larger players like $TSM to SK Hynix have diversified their supply chains against foreign events. Helium is critical to semiconductor supply chains, but the media narrative is sensational. Especially when the largest memory company puts out an assertive statement that there’s no chance the company [SK Hynix] will be affected. _ But to South Korean equities in Samsung/SK Hynix, fears around Oil/LNG/Helium look disconnected from reality: The algorithms selling off SK Hynix because of helium and KEPCO rate hikes are acting on bad math. It is fundamentally a supply chain non-issue. The main threat is oil and energy costs on global macroeconomic shock affecting everything from consumer goods to inflation. March 3 "Black Tuesday" crash dropped KOSPI dropped 7.2% and SK Hynix fell 11.5% in a single session on exactly these energy security fears as the main catalyst. Of course, forced liquidations from leverage added fuel to the fire. However, the disconnect between fundamentals and price action is the trade. If margins were actually threatened, the selloff would be justified. But, the sell-off destroyed more value in one day than DECADES of hiked energy cost increases could have. The fact that the math doesn't support the fear is precisely why it's Korea is a buy, as markets are selling off on emotion rather than looking at the structural expanding profitability despite increasing oil/energy costs.

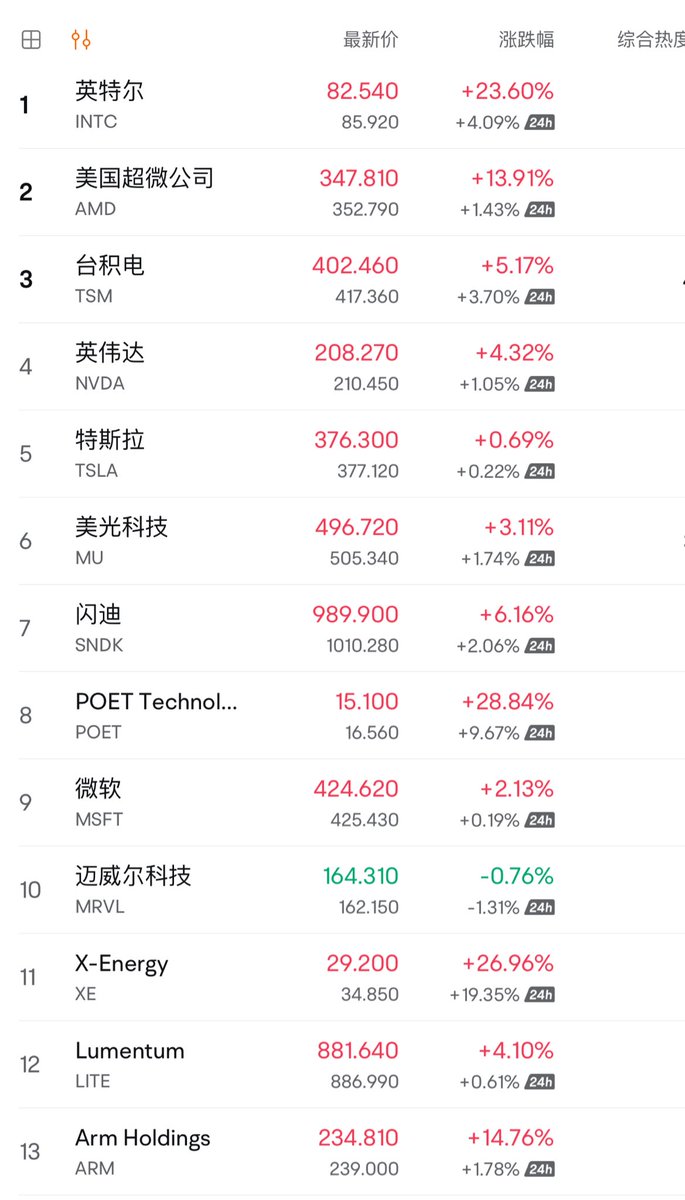

It’s honestly impressive Bloomberg titles have managed to crash the Semi Market for a second day in a row. $LITE down 14.4% $NVDA down 3.5% $TSM down 4.4%. On the news that Oracle and OpenAI are not expanding a part of their Stargate project. This looks more legitimate than yesterday’s report as the OpenAI contagion is spreading. At the very bottom, they left added: $META, to step in and consider leasing the planned expansion site in Abilene, Texas, from developer Crusoe. This looks like a buying opportunity for specific names, as the AI trade has expanded far beyond OpenAI now and is now funded by profitable hyperscalers from $GOOGL to $META.

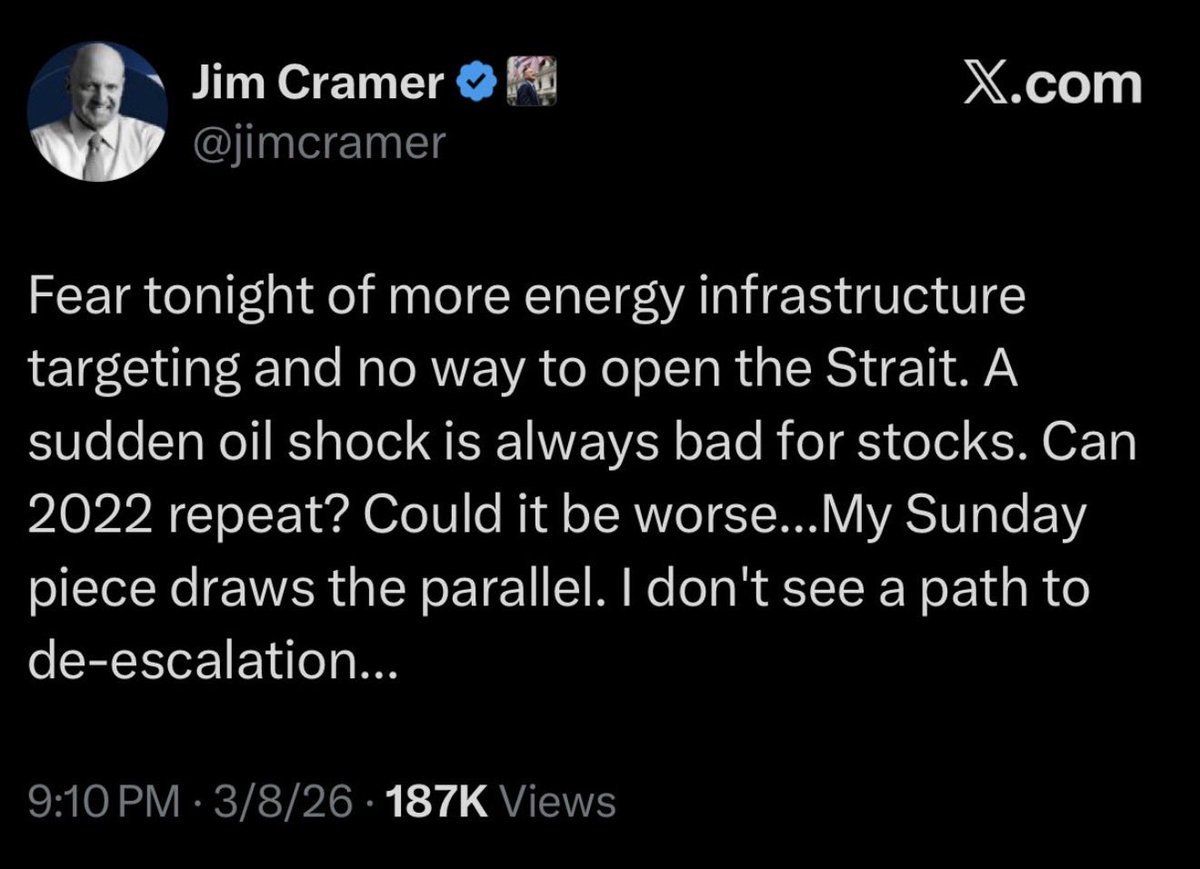

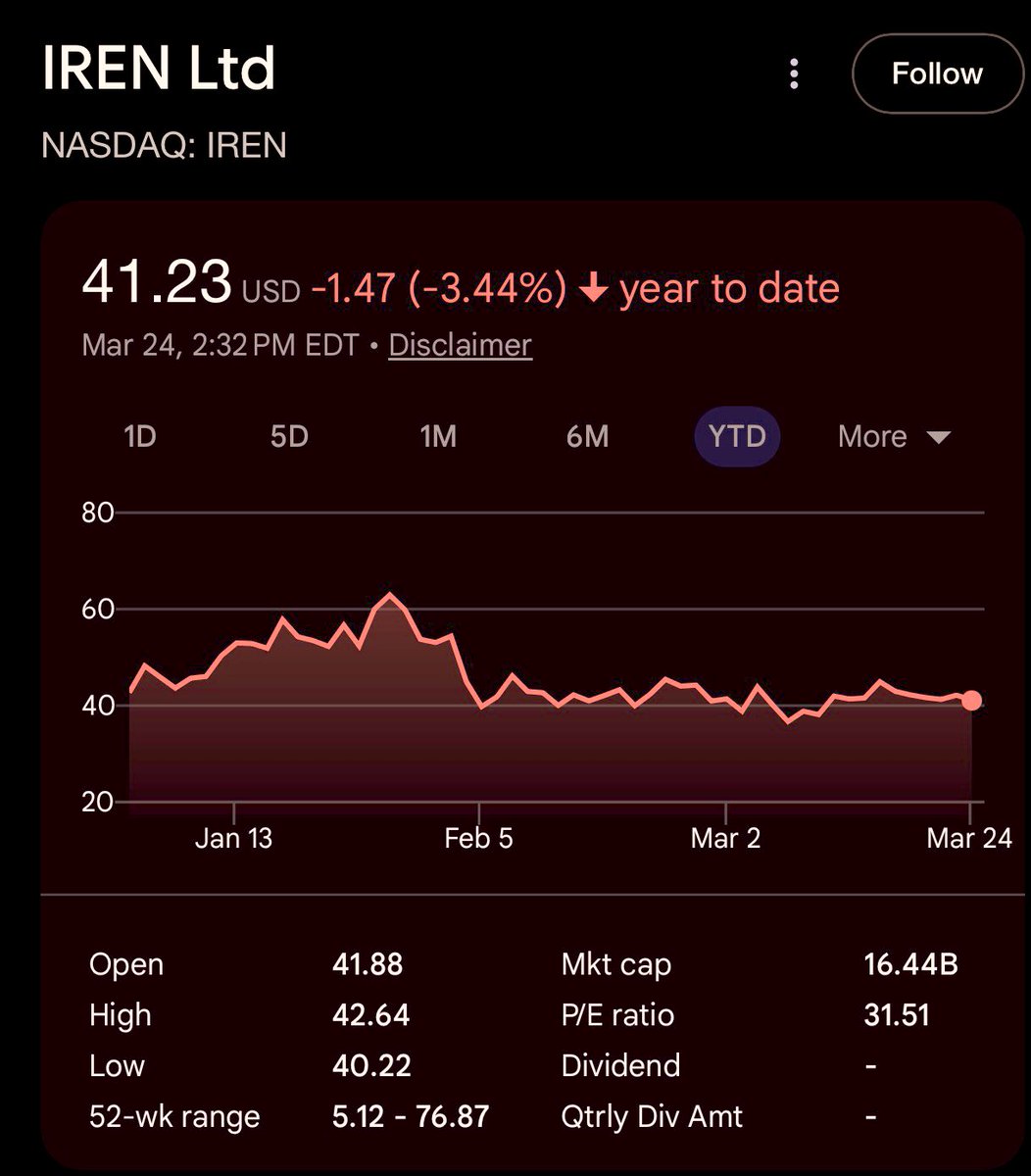

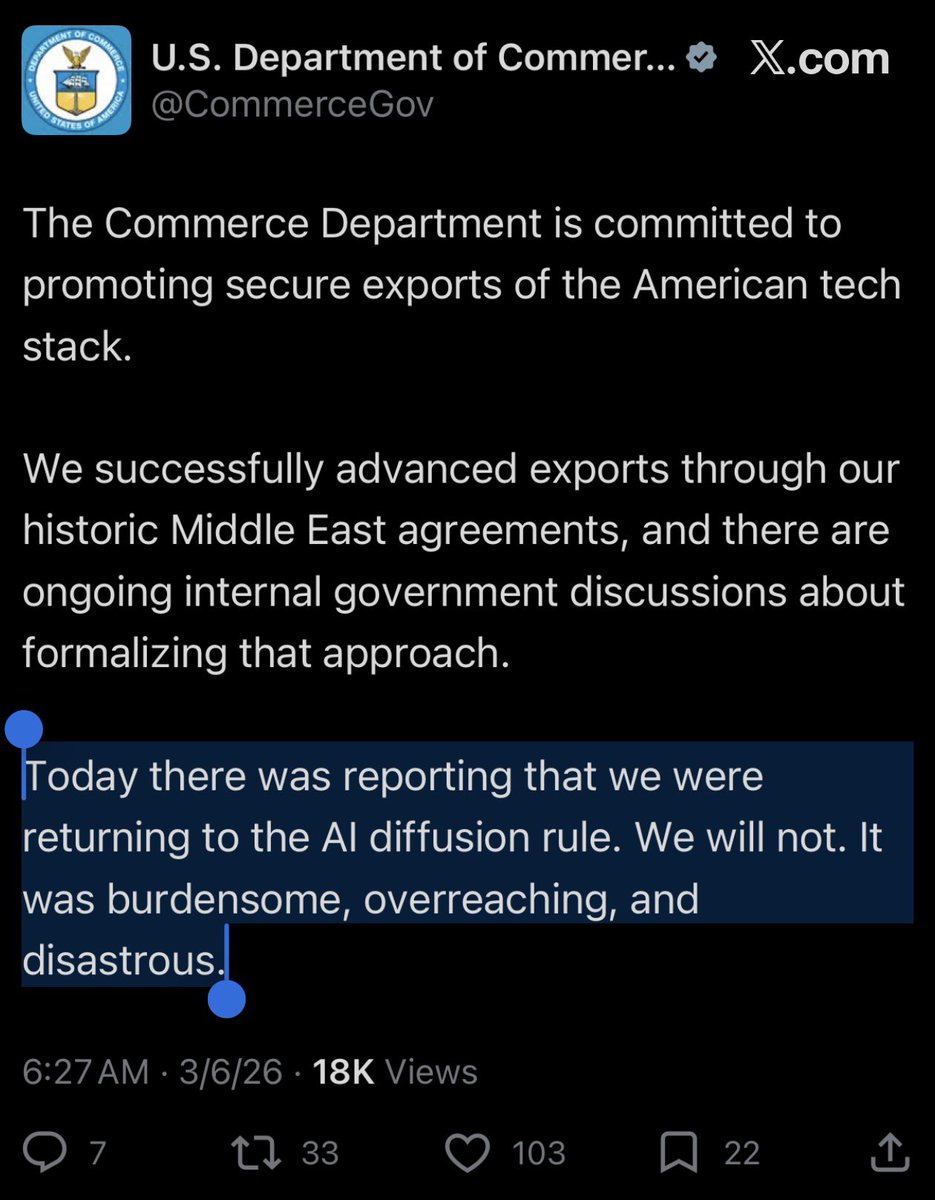

“US Mulls Requiring Permits for Global $NVDA, $AMD AI Chip Sales” Markets are reacting violently to news of the Trump administration was thinking about giving Nvidia the $AXTI export control treatment. Keyword: Proposal | Draft. There is an almost zero chance it passes as is. Tech companies are likely lobbying the administration as this gets reported. In the article: The Trump administration will propose regulations that would require American approval for AI chip shipments worldwide. The result of this bill would bottleneck the AI trade for no reason and harm Trump’s favorite metric: the US stock market. Trump was known for rescinding the Biden-era AI Diffusion Rule: “Major U.S. tech firms, including Nvidia, Microsoft, and Oracle, lobbied against the rule, arguing it could cost them billions in revenue and push partners towards Chinese technology.” So a new policy getting enacted, would be counterintuitive to his agenda. Unfortunately other articles + news on elsewhere reworded this as an imminent export control, rather than a proposal. Sensational / false headline reporting triggered a massive selloff of the entire supply chain from $TSM, $NVDA, to $MU today. However, people do have a right to be worried about the implications.

Feels like everyone is doom-posting KOSPI saying: > “Look at the chart, it can’t keep going up like this!” > Memory is a black hole for demand ( $SNDK taking 3Y preorders ) > $EWY is basically just two stocks, Samsung and SK Hynix, not a representation of the Korean economy > Like saying Taiwan Index is a bubble because the index that tracks $TSM and Mediatek goes up. > Memory demand/AI doesn’t just disappear because of a War in Iran, but it does get more expensive. > Increased energy from crude/LNG get passed down to hyperscalers, not eaten up in opex. It’s looks to be fear selling and deleveraging (3x ETFs and 10x likely got wiped out today) rather than materially operational (slight bearish headwind, but not enough for -30%). SK Hynix futures is now trading in the high $300B MC-low $400B range. If MS and updated analyst projections are even slightly right, SK Hynix’s operating profits for example would be ~$300B. They’ll be sitting on too much money by 2028 as a cushion if memory prices drops. (and not even considering demand becomes structural). Looks to be another DeepSeek-Nvidia type fear selling situation, especially as nand/dram prices get hiked again recently. More of a question of timing the bottom. It’s times like these logic matter more than irrational headline selling.