Sameer Jaferani retweetledi

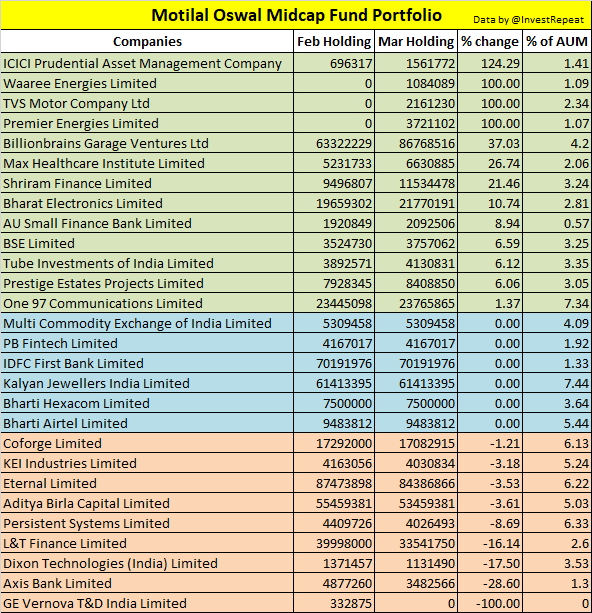

Motilal Oswal Midcap Fund's March Portfolio is out.

🟢 3 fresh buys - Waaree Energies, TVS & Premier Energies

🔴 1 Full Exit - GE Vernova

📈 Currently holding 27 stocks in portfolio. AUM stands at ₹31,000 Cr.

📊 Cash holding (including arbitrage): 13.43% (Jan) to 7.24% (Feb) to 4% (Mar)

English