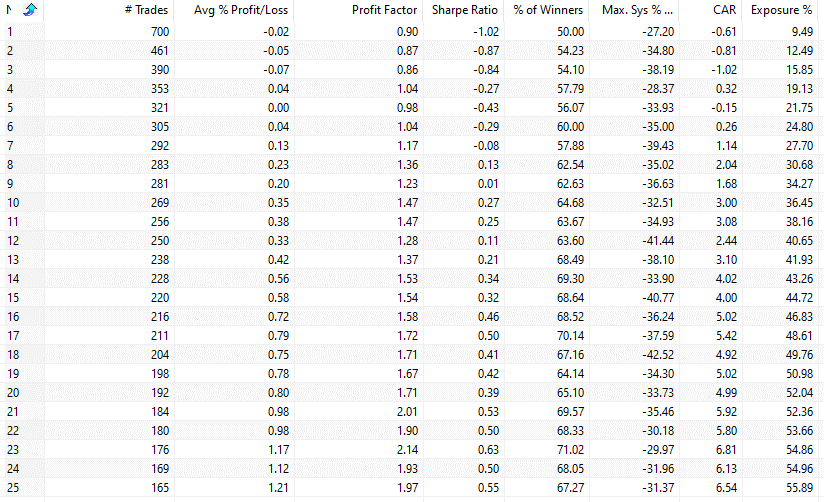

Samuelsson

13.2K posts

Samuelsson

@samuelsson

Entrepreneur, investor, trader, and lifelong learner. 🇸🇪 🇺🇸

Sweden Katılım Mayıs 2008

173 Takip Edilen2.3K Takipçiler

Overnight Trading Strategy: The 3-Day Down Setup.

A classic "Mean Reversion" strategy that exploits the "Overnight Effect," where the majority of S&P 500 returns historically occur between the close and the next day's open.

One simple rule.

The Strategy: 3-Days Down

✅Asset: $SPY

(S&P 500)

✅Trigger: Market closes lower 3 days in a row.

✅Entry: Buy at the 3rd day's close.

✅Exit: Sell at the next day's open.

Results (Since 1993):

✅ 643 Trades

✅ 65% Win Rate

✅ 8% Max Drawdown

The "Greed" Twist: If you hold until the next day's CLOSE instead of the open:

✅Average gain jumps to 0.24% per trade.

✅But... win rate drops and drawdown increases significantly.

Optimization:

By refining the entry/exit, our version hits ~0.35% per trade with lower volatility.

English

What Happens When A Stock Is Overbought?

Most traders think “overbought = sell.”

The data says something more subtle.

A backtest shows that when stocks become overbought (2-day RSI > 95), returns over the next few days are significantly weaker than average, but long-term returns revert back to normal.

Overbought predicts short-term softness, not crashes.

Below are the results for #spy after N-days when RSI(2)>95:

English

NR7 trading strategy for swing trading (with rules, logic, and backtest)

Most traders look for movement. NR7 teaches you to look for contraction.

The NR7 pattern, introduced by Tony Crabel in 1990, is based on a simple but powerful observation:

👉 Big moves often start when volatility contracts first.

An NR7 day occurs when today’s trading range (high − low) is the smallest of the last 7 trading days.

That’s it.

No complicated indicators. Just price behavior.

However, a lesser-known fact is that Crabel designed NR7 for volatility expansion forecasting, not as an entry.

Why does this work?

Markets move in cycles:

Expansion → contraction → expansion

When ranges shrink, energy builds beneath the surface.

It’s the classic “calm before the storm”?

Low volatility frequently precedes sharp directional moves - which is exactly what NR7 tries to capture.

We backtested NR7 (trading rules):

- The range, or volatility, is the difference between the High and the Low (each day).

- If today has the lowest range of the previous last 6 trading days, then we go long at the close.

- We exit at the close when today’s close is higher than yesterday’s high.

We’re not predicting direction.

Unlike many short-term strategies, it is NOT necessarily buying weakness (mean reversion).

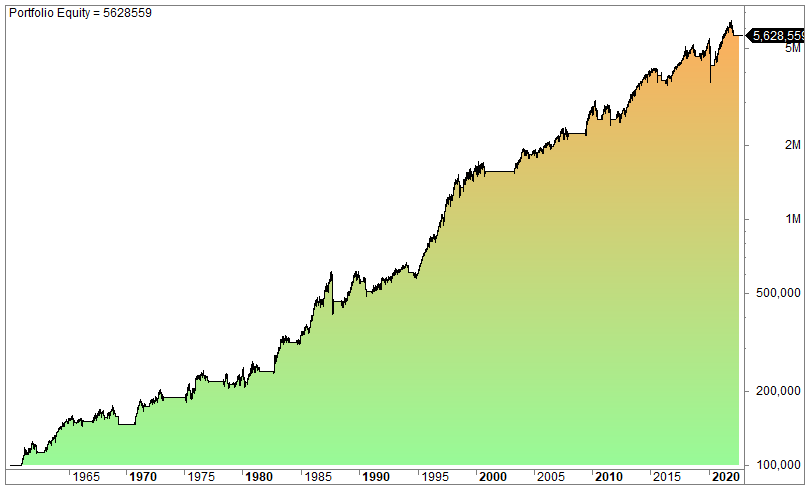

This is the equity curve for SPY since inception:

You are entering during quiet markets - often during stable or bullish environments - which makes it a strong complement to mean-reversion systems.

This diversification aspect is underrated.

Many portfolios are overloaded with the same type of edge.

NR7 behaves differently.

Backtests show something important:

✅ Reasonable long-term performance

✅ Moderate exposure time

✅ Many small gains instead of rare big wins

But also:

⚠️ Average trade can be small

⚠️ Needs exits and filters to improve robustness

In other words:

NR7 is more of a framework than a finished strategy.

However, edges don’t always come from complexity.

English

Absolutely. High win rates alone mean very little. Robustness and realistic assumptions matter more. We published this strategy many years ago, and the backtest itself covers roughly 15–20 years of market data. As always, verify everything yourself and see if you get similar results.

English

@samuelsson High win-rate backtests usually omit the exact conditions that produced them and the slippage plus costs that appear live. Did the 91% survive a regime shift or strict OOS with realistic execution?

English

The best trading strategies are often surprisingly simple.

We tested a Triple RSI strategy that achieved a 91.03% win rate in our backtest.

In the video, we break down the entry and exit rules, the performance, and why testing ideas beats relying on opinions.

English

Samuelsson retweetledi

What just happened?

Last night, news emerged of a "trade deal" that has never happened before.

Nvidia and AMD agreed with Trump to provide the US with 15% of REVENUE from chip sales in China to remove export controls.

Corporations are panicking. Here's why.

(a thread)

English

Samuelsson retweetledi

"While the world fixates on Donald Trump’s populist cocktail of reciprocal tariffs and big, beautiful deficits, @JMilei is delivering a man-made miracle that should gladden the heart of every classical economist and quicken the pulse of all political libertarians." 1/5

English

Varför glöms detta lätt bort eller är det något jag missar?

Jimmy Corsetti@BrightInsight6

“Unprecedented”? Why y’all omitting the ‘Roman Warm Period’ and the ‘Medieval Warming Period’? Is it because it was millennia before the Industrial Revolution and doesn’t fit the fabricated climate narrative? 🧐

Svenska

Samuelsson retweetledi

Javier Milei har sänkt Argentinas månatliga inflation från 26 % till bara 1,5 %.

Ekonomin växte med 7,6 % under Q2 mot året innan.

Han har vänt en 100-år i fel riktning trend.

Men detta kommer ni aldrig få höra något om i mainstream media.

De kallar honom en farlig "högerextrem" galning som förstör sitt land.

Svenska

Samuelsson retweetledi

Just dropped a new newsletter.

One of the backtests this week asks: Can a coin toss actually beat Wall Street’s top investors? 🤔

Plus, we dive into RSI signals, earnings seasons, and more. If you’re into data-driven trading, don’t miss it!

📬 tradingstrategiesdaily.com/p/5-new-market…

English

Samuelsson retweetledi

Developed by Perry Kaufman, the Efficiency Ratio (ER) ranges from 0.0 (no trend) to 1.0 (strong trend).

It’s a practical way to filter market noise and enhance your trading strategy.

Check out this video for a clear breakdown of how it works.

youtube.com/watch?v=oCbFVy…

#Finance #TrendAnalysis

YouTube

English

Samuelsson retweetledi

📉📊 LARRY CONNORS’ %B STRATEGY (BOLLINGER BAND) | TRADING STRATEGIES EXPLAINED 🧠📈🔍📘💹

Larry Connors’ %b strategy is a mean reversion strategy and all such strategies have performed very well over the last 25 years. The strategy has produced some good results, but it remains to be seen how the strategy performs combined with the other strategies of Mr. Connors.

The strategy has the following trading rules:

➨ The close must be above the 200-day moving average.

➨ The %b must be below 0.2 for the last three (consecutive) days.

➨ If 1 and 2 are true, buy on the close.

➨ Exit when the %b closes above 0.8.

We were not able to replicate the results of Connors because we lack his parameters. However, the results are very good in QQQ and SPY, but very few fills. This is the equity curve (Shown below) for QQQ.

Can the strategy be improved or made different? If you have any suggestions, please comment 👇

#tradingstrategies

QuantifiedStrategies.com@QuantifiedStrat

📊 CHANDE MOMENTUM OSCILLATOR TRADING STRATEGY – SETUP, RULES AND BACKTEST 📈 The Chande momentum oscillator is a technical indicator that measures momentum through the daily value change in the security. But the question arises: Can a profitable strategy be developed using it? We backtest a trading strategy using the Chande momentum oscillator for a 9-day period (this is the most used timeframe). ➨ We buy when the Chande momentum oscillator is under -50 ➨ We sell either when the oscillator crosses above 50 or 5 days after the buy signal was triggered We backtested the trading strategy using the SPY ETF. The data is adjusted for dividends. Below is the equity curve for our Python backtest. Can the strategy be improved or made different? If you have any suggestions, please comment 👇 #tradingstrategies

English

Samuelsson retweetledi

🌟 GOLDEN CROSS TRADING STRATEGY (BACKTEST ANALYSIS) 📈📊

A Golden Cross happens when the short moving average crosses above the long moving average. As a trading signal, it works reasonably well. It keeps you invested in bullish markets and keeps you out of trouble when we get a bear market.

The trading rules are simple:

➨ When the 50-day moving average crosses above the 200-day moving average, it signals a bullish breakout, and you buy.

➨ Alternately, when the 50-day moving average crosses below the 200-day moving average, it signals a bearish breakout, and you sell your position.

We backtested the strategy on the S&P 500 since 1960. We used the same trading rules as described above.

Below is the equity curve from our trade since 1960.

Can the strategy be improved or made different? If you have any suggestions, please comment 👇

#tradingstrategies

QuantifiedStrategies.com@QuantifiedStrat

📉 WILLIAMSVIXFIX TRADING STRATEGIES – DOES IT WORK? 🤔 In this post, we explain what the WilliamsVixFix indicator is, how you can use it, and whether is a good trading tool or not. We test one WilliamsVixFix trading strategy. The indicator works. We backtest the following trading rules: ➨ Find the highest close over the last 22 days and subtract the low of today (or the current bar). ➨ Divide by the highest close of the past 22 days. ➨ The result is multiplied by 100 to "normalize" the indicator. CM WilliamsVixFix is a synthetic VIX. How does it compare to the original VIX? Below is the chart of the S&P 500, Williams Vix Fix, and the VIX. Can the strategy be improved or made different? If you have any suggestions, please comment 👇 #TradingStrategies

English

Samuelsson retweetledi

Tariffs force countries back to free trade.

Very simple concept but misunderstood by most people.

Palmer Luckey@PalmerLuckey

"Unprecedented embrace of protectionism", they say. No, reciprocal tariffs are the opposite. The whole point is to encourage free trade rather than lopsided "free trade" we currently have with so many countries. "It's very simple. If they charge us, we charge them."

English

Samuelsson retweetledi

Tariffs are working and most people just haven't realized it yet.

English

Samuelsson retweetledi

Saying that there are many competing "schools" of Economics is like saying there are many schools of Mathematics.

"1+1=2" doesn't care, nor does "human action is purposeful behavior."

Economics, like mathematics, is a precise a-priori science with crystal clear boundaries.

English