Steven shaw

2.5K posts

@rynokinsight If you look at trucking, for example, mile rates rose faster than diesel prices. Why won't something similar happen to metals demand with all the rebuilding that needs to happen and the data center buildout?

English

@WilfredFrost @DanielTNiles Who is the investment banker for NVTS

English

HOLD MORE CASH - says legendary tech investor

@DanielTNiles in this week’s episode of The Master Investor Podcast, just six weeks after he correctly called for a more aggressive risk-on approach at the end of March, since when Nasdaq has surged 25%.

SEMIS: “So in the short term, are semis at the most overbought they've been since 2000 or 1995 before they had horrific corrections? Absolutely.”

IRAN WAR: “If it going to take a lot longer for this situation at the Strait of Hormuz to get sorted out, then you're going to see stock prices collapse to catch up with where bond yields & oil prices are. I don't think that's the case. But, I'm viewing things as you should be sitting with a lot of cash.”

MEGA CAP WINNER: “It's obviously Google. They have the full stack & they're the ones you should bet on...they've got everything & they've got the massive cashflow to fund it.”

However, the shift to Agentic AI should sustain earnings upgrades this year, making today more like 1998 than 99/00, but be prepared for 30-50% AI trade pull-back in early 2027.

We also discussed what the shift to Agentic AI means for $NVDA (not ideal), Intel $INTC (great) and $AMD (good); why concerns over $META are NOT overdone; why $AAPL fortunes should improve; why $AMZN & $MSFT are struggling short term, & why $GOOGL shines bright.

Timestamps:

00:00 Intro

02:39 Why today feels like 1998, NOT 1999/2000

05:25 Agentic AI suggests more upside to bull market

07:52 But Iran War could derail things

11:18 Agentic AI means CPU’s over GPU’s

13:35 Semis are overbought

17:51 Is shift to CPUs bad for Nvidia?

19:13 Google the standout performer

21:15 Apple leadership transition

23:45 Meta concerns not overdone

25:37 Google best placed

27:36 30-50% AI crash by early 2027

30:01 Concerns about OpenAI

34:27 Upcoming IPOs, oil, bonds signal problems

36:16 Hold more cash

37:48 Kevin Warsh a positive, but watch bonds

45:44 Conclusion: 1998 or 1999?

English

Man I hope this $KYIV trade works out…

*Walter Bloomberg@DeItaone

TRUMP: RUSSIA-UKRAINE WAR IS GOING TO END VERY SOON

English

When my wife asks how we are going to afford our trip

English

$PCG is reminding me a lot of $LYV when I was “screaming into the void” at $120…

The financials are beyond easy to model (it’s literally a regulated utility). But there’s this scary legal/regulatory overhang compressing the multiple…

If the California legislature does anything even slightly constructive this summer, the stock probably rerates hard as the market starts pricing out the left tail…

English

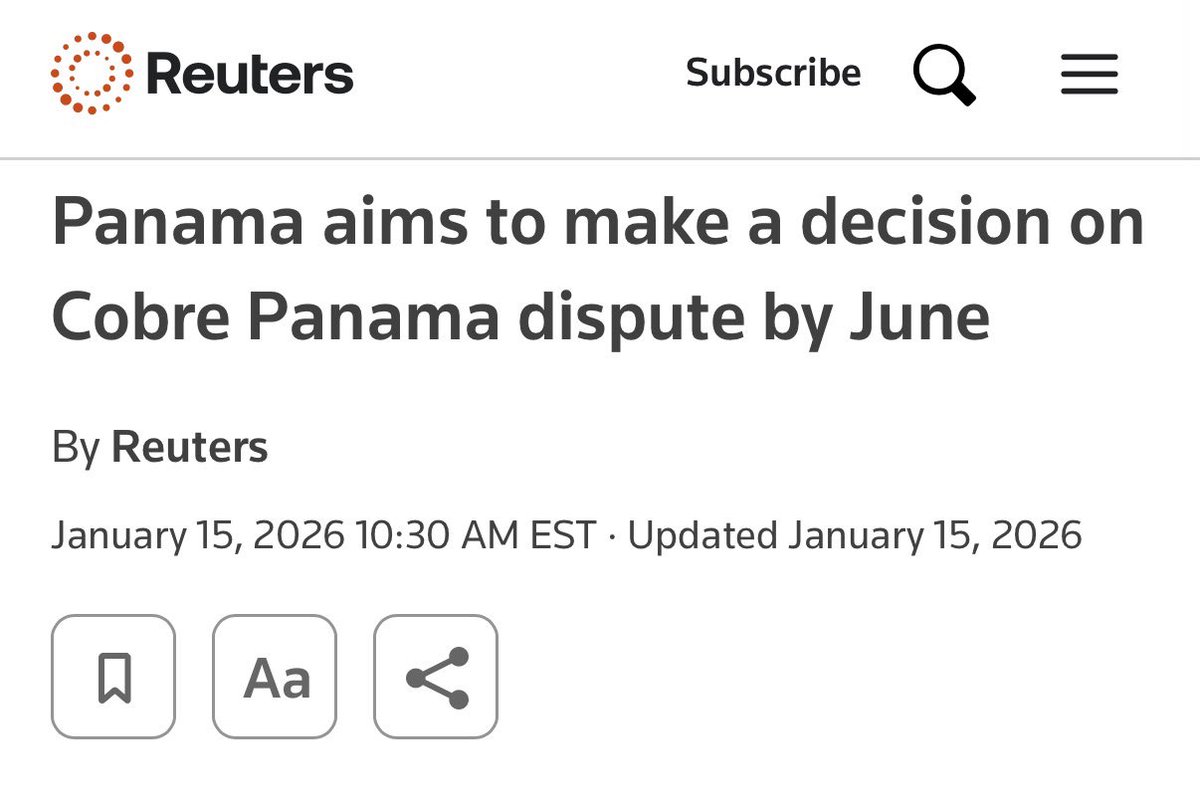

$FM.CN looks cheap into the June Cobre Panama decision.

Cobre is the massive Panama copper mine that was shut for political/legal reasons, not because the asset is broken. It’s ~35–40% of NAV and the stock still only prices in roughly half its value…

MINING.COM@mining

First Quantum loss widens on costs, output dips dlvr.it/TSHM3z

English

$BW no longer a thirteen bagger, sold off to be a ten bagger. I sold calls on 60% of the position that will now all expire worthless.

GIF

English

@SFarringtonBKC This is unlikely to shrink the deficit and I am skeptical that Warsh will support a rate cutting regime unless there is recession. Don't forget the Druck connection! How do you shrink the balance sheet and cut rates?

English

Overnight rates gonna get cut so hard, yield curve gonna steepen, deficit gonna shrink, housing market gonna unfreeze, home equity loans are going to sell like hotcakes, financials gonna boom. $OPEN, $RKT, $BLNE, $SOFI

Daniel@danielisdizzy

Kevin Warsh, the new Fed Chair, just made it clear why rates are going lower: “AI is going to make almost everything cost less. We’re at the front end of a productivity boom. Economic growth won’t be inflationary—we’re in the early innings of a structural decline in prices.” Elon Musk, Sam Altman, even Stanley Druckenmiller all expect AI to be strongly deflationary. The next few years are going to be insane.

English

$PCG is a situation: California Wildfire Legislation (a regulatory discount story).

The utility still carries scar tissue from the Camp Fire (2018), the bankruptcy (2019), and fear that California could reopen wildfire liability risk for equity holders.

The key backdrop is AB 1054 (2019) and SB 254 (2025). AB 1054 created the backbone of the current framework, including the prudency standard (utilities can recover wildfire costs if conduct was reasonable) and the 20% disallowance cap (shareholders cannot be forced to absorb more than 20% of claims in a prudency review).

SB 254 reinforced that framework through the Continuation Account (extending the wildfire fund), but it also required a broader 2026 policy review, with CEA recommendations due by 4/1/26 that now flow into a state legislative process ending 8/31/26.

The key bear thesis is that the stock has gotten ahead of itself before any meaningful change has actually occurred. That is fair. But the outcome range is still fairly clear: California can reinforce the framework and keep the prudency standard and 20% cap intact, which would narrow the regulatory discount; go further and reduce structural wildfire risk through stronger backstops or broader cost sharing, which would close even more of the discount; or create ambiguity around the durability of the cap or prudency standard, which would keep a higher cost of capital on the equity.

That’s the setup. $PCG is about whether the 2026 review ends with reinforcement, further structural de-risking, or renewed uncertainty.

Place your bets…

English

Monday will be ugly…

English

Joe Kernen was such an obvious Republican flunky, a totally unobjective idiot. It's a bit frightening to see that on financial networks.

English

The Kingdom Capital Advisors Q1-2026 letter is now available: kingdomcapitaladvisors.com/fund-letters/q…

English