🚨 Successful claims stories

A follower approached us,

His wife was diagnosed with dengue and its complications,

He lodged a claim with the top insurer,

The insurer rejected his claim, stating that diabetes was a pre-existing medical condition not disclosed.

He reached out to us at 8:30 PM in the evening,

We got our teams rolling ...and assessed his case,

He had indeed disclosed diabetes in his policy ,and he was entitled to this claim.

Our claims team reached to the teams within the insurer,

We began to work with the insurer to clear the misunderstanding,

After sharing the relevant document,

The pre-authorisation was accepted at 11:30 PM in the night.

The follower was really really happy that we were able to help him get the claim!

Night or day, the intent is to help customers/followewrs with claims,😄😄😄

Now onto the next claim!🫡🫡🫡

Hi! Yes. Even after the 5-year moratorium period, an insurer can still reject a claim if they’re able to prove fraud. The moratorium period protects you from past honest mistakes, but it’s not an automatic free pass. If the insurer thinks something was deliberately hidden, they can investigate and deny, and then it comes down to whether they can prove intent or you can show it was an honest miss. So, the safest thumb-rule is: disclose everything to the best of your knowledge and keep your medical records handy. If you ever face an unfair denial, escalate it to the insurer’s GRO first, then to IRDAI’s Grievance Redressal Cell, and finally the Insurance Ombudsman.

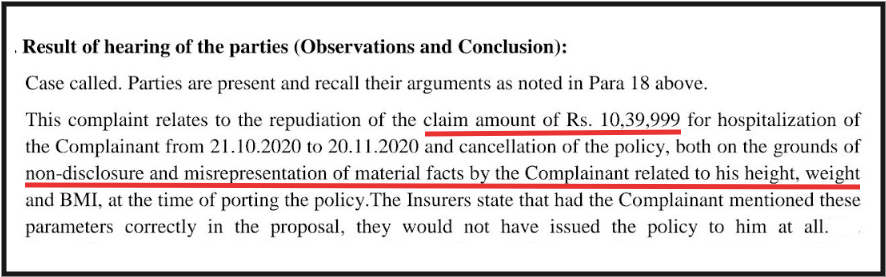

10L claim rejected over incorrect weight

Worse: Insurer cancelled the entire policy

What happened?

How can you ensure this doesn't happen with you?

Find out 👇

🚨Niva Bupa rolls back premium hike on Aspire

To pass on the full GST benefit to customers,

Niva Bupa has now rolled back the premium hike on its policy for young people, "Aspire"

Niva will revert to old premiums effective immediately!

My brother, he didn't have to wait. He could leave or drop me and i would be charged. But no he didn't. It was 2+ 2 mins. I would be charged for the 2 overhead mins and I think rapido charges 3 rupees a min. He wanted more. He wanted 10 rupees per min . He fought with me for North of 10 mins. It's not about the money or wait time it's about getting his way which he did.

.@rapidobikeapp

who runs your mafia business? Because this driver just harassed me for waiting for 3 mins and he has the audacity to say "dekhta hoon kaise jaate ho".

I booked an auto. I ask him to wait for 2 mins because I was finding the keys. I come down. This certain gentleman starts threatening and shouting at me.

I paid him 20 rupees because he was threatening to harm me.

This is right infront of my house.

Rapido calls people late night after a ride is over. It has always been so funny to me cause the customers are at risk before starting the ride.

To hell with this city and its people who can just walk away threatening you like this and the only vestige of hope you have is by tweeting about it ?

I

🚨What happens if you hide/forget to disclose a disease while buying a health insurance policy?

Just talked to a follower,

His claim for his father was rejected by a top insurer.

He did not disclose diabetes for his father while buying his policy 5 years ago,

His father was admitted to the hospital for chronic kidney disease and is now on dialysis.

During the investigation,

The insurer found that the father had diabetes while buying the policy, and this was not disclosed.

The customer told us his father forgot to disclose the disease as he was unaware he needed to disclose.

The insurer not only rejected the claim

But terminated the policy there by losing 5 year of premiums and continuity benefits,

On top of this,

His father will never get a new policy due to the kidney problems,

Always disclose all pre-existing medical conditions at the time of buying the policy,

Even if this leads to rejection of the policy

If you forget to disclose all pre-existing diseases at the time of buying the policy,

The insurer will not only reject your claim but also terminate ur policy,

@NIKHILLJHA@nikhil89nick Can you please give more clarification on this scenario? I don't think this is a case of fraud, this is more of a misrepresentation. Would moratorium have saved the customer in this case 5 years would have been completed?

💖 Relief Delivered: ₹92.66L Cashless Claim Approved After Personal Intervention🙏@Niva_Bupa

✨ A Life-Changing Win: ₹92.66 Lakhs Cashless Approved with Heart & Hustle

Mr. Jain’s claim was initially approved for ₹25 Lakhs. Understanding the need for more support, I personally stepped in to coordinate with the hospital and Niva Bupa.

Through prompt communication and diligent follow-up, all queries were resolved smoothly.

On 23rd Sept 2025, the final-cashless approval was successfully revised to ₹92,66,049 — a huge relief for the family.

Grateful to Niva Bupa for their cooperation and proud of my role in making this possible.

“True success is standing by people when it matters most.”

Excepts Consumables almost everything got paid.

#InsuranceWin#ClaimSuccess#NivaBupa#CashlessClaim#PatientFirst#InsuranceSupport#RealStory#HealthcareHeroes#InsuranceAdvisor#SuccessMatters#CustomerSupport#CashlessApproved

@stepbystep888 Another reason

let say in an unfortunate even the policyholder get demised during the policy period, in regular he would have paid only for that number of years and could have saved the remaining years premium but if he would have paid all in advance.. it won't be returned back

Why regular pay is better in term insurance than limited pay.

live example:

Bajaj Life, 2 Crore premium, female, non-smoker, current age = 34 years

Reason 1: Present value of future cash flows is cheaper in regular pay vs. limited pay.

99% policies sold by Holistic Wealth is regular pay.

Reason 2:

Why pay in advance?

Is there any other service for which you have considered paying 16 years in advance?

Are you paying the school fees of your kids quarter by quarter or you have paid 12 years of the fees in one go?

Reason 3:

The option to lapse the policy. Let's say this person by the time she turn 50 has accumulated 15 Crore, why does she need the term insurance anymore. She can simple stop paying the premiums and lapse the policy.

🚨Deductibles in Health insurance-A great way to lower premiums

Deductible is a fixed amount that u will pay once,

before the insurer starts to pay the claim.

Deductible can drop ur health insurance premium by 18-50%🤯🤯

A thread🧵on what is deductibles & how to effectively use deductibles?👇

One of my very close friend yeasterday done with his surgery and got discharged not a single rupees has been deducted… when he got hospitalised on 15th sept , hospital ask to pay some amount for non deductible items as most companies dont pay that , so pay upfront a sum of around 50k … we talk to their TPA desk .. and asked them to put all claim if something deducted will pay at that time after so many back and forth they agreed..

And yeasterday not a single penny has deducted and he went home without paying anything from his pocket…

Praying for his speedy recovery ❤️

6/n

Currently insured person usually clarify from customer care about an eligibility of procedure and sometime they get clarity but it is not binding on insurer and sometime they just ask us to file for a claim and then see but insurer never give anything in written beforehand.