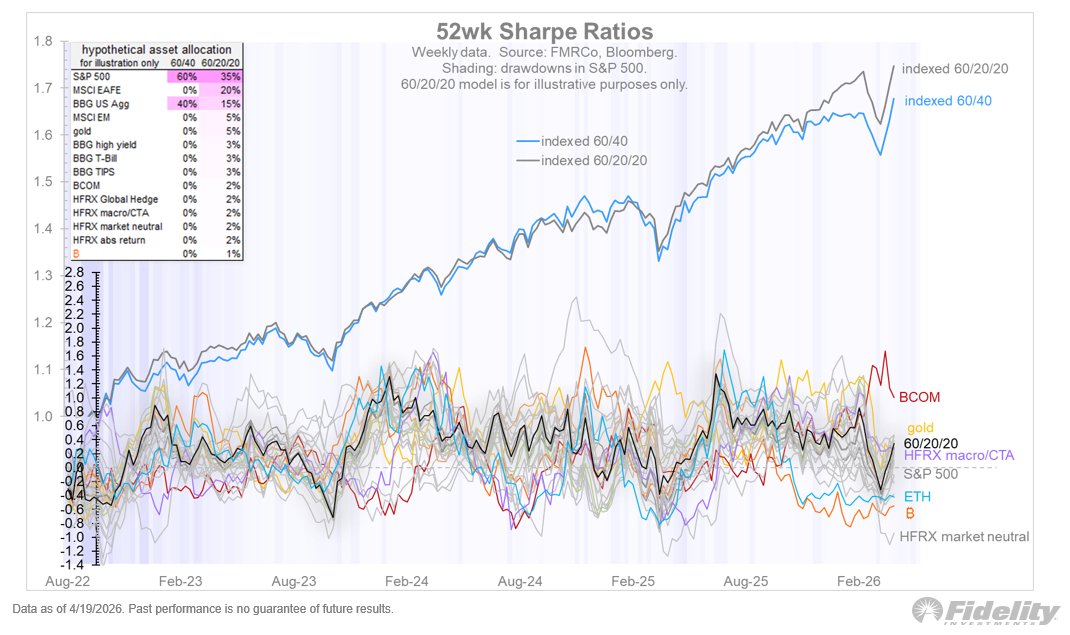

@TimmerFidelity I like using Bitcoin to get equity exposure in a more capital efficient way and redirecting that capital to diversifying strategies

open.substack.com/pub/andrewsieg…

English

Andrew Siegler

54 posts

@sieglerandrew

Another ex-Bridgewater on https://t.co/EFEFVCyXV4 https://t.co/IsPiiypHBK

"you can't adequately teach your kid in 3 hours a day!" "So the school can do it in 8?" "No, you have to do it after they get home from school, it takes about 3 hours"

no one is talking about this…

NEW: The Trump-Vance White House has falsely accused an ally of Pope Leo — Sister Norma Pimentel — of illegal activity tied to migrant aid, and cut off all federal funding to Catholic Charities in south Texas. Church leaders say it’s a targeted, political reprisal against Pope Leo and the Catholic Church. thelettersfromleo.com/p/trump-vance-…

Snap