Sabitlenmiş Tweet

Juan M

41 posts

Juan M

@siroexmon

building internet-native capital markets @fence_finance prev. core contrib. at yearn

Madrid / New York Katılım Şubat 2022

189 Takip Edilen41 Takipçiler

@bridge__harris we are building the infra for that to be possible at @fence_finance

English

@sytaylor @stripe The industry is waking up to the potential of stablecoins.

Soon they will realise how powerful stablecoin finance is and how solutions like @fence_finance leverage stablecoins to build better debt capital markets infrastructure.

English

Confirmed: @stripe's biggest-ever acquisition is of the Stablecoin platform Bridge.

Bridge provides software that helps businesses accept Stablecoin payments and simplifies the infrastructure (a bit like Stripe does for TradFi).

🧠 This will go down as an Instagram-like all-time great acquisition.

It solves a huge long-term pain point for Stripe. Accessing a 24/7, instant, global, dollar-based rail means they can provide new value to customers.

Sell from anywhere and get paid instantly in dollars without dealing with crypto complexity.

🧠 This is the largest acquisition in Crypto history

It marks a narrative shift from Crypto being about price, to it being about business value.

🧠 Stablecoins are 24/7, global and instant.

There's no other way to move dollars as instantly and cheaply. If you're still doubting them, take another look, they've come a long way since 2021.

🧠 Today Stablecoins infrastructure is complex.

If you want to move Stablecoins in a way that's cheap, instant and compliant that's hard. You have networks like Ethereum and Solana, Wallets, and different coins like USDC or PYUSD (PayPal).

🧠 Bridge simplifies it.

Bridge makes all of that go away. Bridge makes Stablecoins work like someone who's never used Stablecoins think they should.

Which is exactly what Stripe does for traditional rails.

🧠 Strategically, this solves a big pain point for Stripe.

Stripe is not the same company outside of the US and Europe. The long tail of Asian, LATAM and global south markets are very expensive and slow to integrate with. Stablecoins fix this.

🧠 Stablecoins are increasingly infrastructure not a consumer experience.

Stripe can now offer US dollar liquidity, 24/7, instantly to sellers anywhere in the world. That seller can then choose to "off ramp" into their local currency or rail at their convenience.

PS. We did an hour long conversation with Bridge founder @zcabrams on the Tokenized podcast (find it wherever you get your podcasts)

Michael Arrington 🏴☠️@arrington

This deal is done. $1.1b techcrunch.com/2024/10/17/str…

English

@jeff_weinstein we @fence_finance are reducing latency in debt capital markets, reducing the time of funding of every single receivable and eliminating negative carry

English

what are the most “latency reducing” focused companies, at any layer of the stack?

English

Juan M retweetledi

Very excited to be partnering with @MorphoLabs for our liquidity management module

Fence's MetaVault will be a crucial part of our plan to remove cash drag from private credit without adding unwanted risks thanks to isolation of markets

Morpho 🦋@Morpho

1/ A new EURe vault curated by @fence_finance is live on Morpho Blue. The vault will generate yield on @monerium's EURe by lending against stable and liquid RWAs starting with wbC3M from @BackedFi.

English

@santiagoroel spot on.

That's our thesis @fence_finance as well.

We are bringing to live our mission : build internet-native debt capital markets

English

Thing about crypto is that it’s the first capital market that has global capital formation with speed and increasing scale.

Money moves much faster in crypto rails than traditional rails as it allows practically anyone with access to internet to tap into these networks. On-ramps being the biggest bottleneck. That’s not the case for localized and fragmented capital markets (Wall St, London, Dubai, HK, Shanghai etc).

Capital has been constrained by antiquated networks (think transfer networks like SWIFT) and artificial restrictions to limit capital flight.

Crypto removes that constraint and is unlocking a sea of capital that wants to move more freely. The result is what you’re seeing in crypto. Capital formation at the speed of light ⚡️

English

@CarrascosaCris_ muy interesante! Gracias Cristina.

En el post dices que las stablecoins no son consideradas dinero. algunas preguntas al respecto:

es el e-money dinero?

Lo serán/ son los EMT? o también son simple medio de cambio?

Español

@santiagoroel when you know how to deal with known logic attacks, it is a lot more scary to use new languages/ new compilers/ new ... that have more unknown unknowns

English

I get it. For a long time Solidity was the only game in town but now we have better alternative programming languages to deploy smart contracts compatible with Ethereum. I may be missing something (note: not technical) but it makes me wonder why it makes sense to use Solidity at this point…🤔

English

Most if not all of finance will eventually migrate to DeFi rails

It's when not if

English

@AlexH_Johnson great post! I believe you will like what we are building at @fence_finance , internet-native debt capital markets

English

At SpaceX, Elon Musk created an “idiot index” to locate areas in rocket construction where laziness and out-of-date assumptions were keeping costs unreasonably high.

A similar exercise is needed in small business lending in order to unlock the access to capital that entrepreneurs need.

I dove deep into this topic in today’s special @FintechTakes deep dive, sponsored by @ntropy_dev.

workweek.com/2023/11/01/a-f…

English

@austincampbell I agree with most of your points. Working in building the infrastructure to solve them.

would love to chat, DMd

English

As someone who works in crypto, but has a background in both reinsurance and tradfi, I have some views here. To give a little background, I've been involved in the tokenization of assets at scale, I've traded all kinds of fixed income, and I've managed one of the largest ILS portfolios in the world. I'm not speaking as a casual here.

Some thoughts:

1 - You do not get to magically say blockchain lowers risk and wave your hand at it, then move on. In many cases, tokenizing assets and putting them on a blockchain is adding a layer of risk (you've added another ledger and a 24/7 system with different behavior on top of your already existing ledger, often on a different timescale), not removing it. Yes, there are theoretical benefits to using a blockchain, such as transparency of the token, tracking, and so on... but many of the alleged benefits (such as eliminating counterparty credit risk) have not even been competently built on-chain yet for abstracted or generalized use cases, much less in a way that also would eliminate it in the underlying market. In short, the majority of tokenized real assets probably add risk, not reduce it, in the current environment.

2 - One of the reasons I am so deeply skeptical of the tokenization of assets by crypto natives is that to understand how to tokenize an asset, especially off-the-run assets that already have not gained significant real-world adoption, you need to have a deep understanding of the asset itself. Raising parametric insurance contracts as an example here with absolutely zero discussion of the core problems with the parametric insurance contract market (namely basis risk and measurement disputes) that have nothing to do with a blockchain is just absolutely wild. This is like saying the core problem with horse adoption is lack of awareness or distribution of horses and completely ignoring the existence of the automobile. I want to be clear as someone who has worked in these markets: parametric insurance and private debt markets are deep expert markets with real-world structure problems that blockchains do not solve. Tokenizing and distributing markets that are complex and explode like live grenades in the hands of even sophisticated investors, but doing it retail? That is nothing more than a deeply cynical and morally repugnant cash-grab. Again, throwing these out casually is precisely the problem; this is classic hype merchant behavior of dispensing magic keywords without any understanding of the underlying structure, and indicative of the sort of thing that should cause you to throw out an entire pitch from someone when you see it.

3 - You do not disintermediate many of the things referenced (IBs, trustees, servicers, lawyers, auditors, etc.) by tokenizing assets. Unless the asset is a natively crypto asset, which is demonstrably not the case if we are tokenizing real assets, you still need all those things back out in the real world. Yes, for purely crypto applications or clever designs for some specific real-world use cases, it's possible to have some degree of "code is law" type implementation, though man, I really do not think people understand both the implications of that or how to do that in an effective manner. @lex_node writes about this often and far more effectively than I could, so let me just shill his handle here as someone who has opinions so informed on this topic it's probably unhealthy.

4 - You also don't get to magically say all this data exists on blockchains. It's often the collection of the data itself that is the problem. Slipping in references about sensors, drones, and wearables as though we are going to live in a 24/7 complete and total surveillance state to get slightly better settlement on a blockchain is again, deeply cynical (that, or the author genuinely believes in a more authoritarian dystopia than anything which currently exists on the planet). How, precisely, are we going to have real-time data about many private credit agreements? Do we think businesses are going to publicly put every single shred of their data on-chain to be analyzed? Track their employees in real time like they are automatons and put it all on-chain? Again, this is just confounding and unprofessional stuff.

I suppose I simply find it profoundly disappointing and sad that this is the state of the pitch for real assets on chain. If an intern had handed me something like this when I ran a trading desk, I'd have sent them home for the summer and told them they weren't getting a job. This is so far below replacement level in terms of how to think about or build fundamental structures on chain that I would have to write a post 20x as long just to explain how broken some of this thinking is, and how fundamentally we have to re-work some of these assumptions to get to a place where we can truly get useful things on-chain in a way that will improve the lives of people in the real world.

Teej@Lempheter

We’ve gotten RWAs all wrong. The future of RWAs aren’t copy-paste of tradfi assets, inheriting the inefficiencies of the old system. The RWA mega-protocols of 2030 will leapfrog tired off-chain infrastructure and: A) Solve an actual, non-fugazi non-legerdemain problem for real world issuers and investors B) Give rise to new new, blockchain-native asset classes (birth assets) The reality is that most RWAs that end up on-chain otherwise wouldn’t be financed traditionally. The “problem” being solved, if any, is that risk is being underpriced. Adverse selection. During my time at Maker, we (RWA units) helped usher in the current, flourishing era of on-chain RWAs. Serving as a sovereign mega balance sheet willing to take risk on commercial real estate, US gov debt, and structured credit. We were the buyer in the market, we provided almost all the demand. This was key because every on-chain RWA marketplace easily finds asset issuers to SUPPLY assets (will look for anywhere that gives them the cheapest capital), but it has always been and will always be the DEMAND side that is elusive. The next, binary unlock for RWAs is getting traditional, institutional investors to allocate. What will drive this? Again - 1) Solving a problem for them - i.e. lowering risk 2) Providing net new asset classes, otherwise inaccessible via traditional deal flow 1) Lowering Risk Risk takes a number of forms, from credit to market to liquidity and many more. To me, fundamentally, blockchains are risk-reduction machines: counter-party risk, settlement risk, data fidelity risk, and eventually, as a function of successfully mitigating these risks, liquidity risk. 2) Net New Assets Not the same old shit. Parametric insurance contracts, hash-power derivatives, deterministic debt (on-chain borrower's revenue contracts are escrowed), and vast securitizations of assets that would've otherwise never been securitized. This is what we are doing at @EntheosNetwork with smart battery securitizations. This last point is important. Securitization is one of the most fundamentally important financial innovations in our lifetimes. Diversification drives a lower risk profile, which invites more investment, driving down the cost of capital to end borrowers, driving demand for more assets, which then get sluiced back into securitization and so on... But most assets never make into securitization execution. Why? Because the service providers necessary to make it happen in a tradfi are prohibitively expensive. Placement agents, investment banks, trustees, special servicers, master servicers, lawyers, auditors. These parties are paid massive amounts to pass paper and cash back and forth. Reporting on asset performance and remitting distributions. Blockchains are built to remit high fidelity data, distribute value without settlement, custody, and counter-party risk, be audited easily and deterministically, enforce cash waterfalls via smart contracts, and permit seamless capital formation, combination, and composability. Of course the devil lies off-chain: the oracles. I believe blockchains will combine with a new generation of higher-fidelity, tamper-proof oracles (i.e. not a servicer who collects a rent roll from landlords once a month). Asset performance will be machine-reported, real-time, and highly reliable. We'll see composability between sensors, drones, and wearables reporting on assets and DePIN networks like @helium and @Hivemapper. Ultimately what's being built is a completely fresh supply chain for infrastructure, physical (renewables, telecoms, etc.), financial (new securitization structures, reporting (IoT), and legal (smart contract logic). Incrementalism isn't going to cut it. Blockchains are an exponential technology and will seep into every aspect of the real world.

English

@high_byte Medium version

@imolfar/why-and-how-zk-snark-works-1-introduction-the-medium-of-a-proof-d946e931160" target="_blank" rel="nofollow noopener">medium.com/@imolfar/why-a…

Deutsch

casual reminder to read this if you're interested in zk math

arxiv.org/abs/1906.07221

English

@melissawasser I would love to read and provide feedback! part 1 was very useful when we started @fence_finance, and we solve quite a lot of the main pains stated there

we have learned a lot by working with banks and fintech platforms to solve them, so happy to help if still able

English

We are releasing the next debt series soon..we would like to update our market map! Comment on any changes we should make. There have been quite a few changes in 2023! a16z.com/2022/04/15/16-…

English

@JeanineSuah free last minute flight cancellation/ reschedule is a must for me

English

Perhaps you'd like to verify RISC Zero proofs on chain? Now you can!

RISC Zero@RiscZero

RISC Zero on Ethereum? It’s happening! Last week, we posted our first low-cost proof on Sepolia. We're excited to enable builders to make use of complex logic in on-chain applications — without ballooning gas costs. Check the 🧵 for the full article & all the details.

English

@samdblond Fence.finance / SaaS to manage and automate asset-backed debt facilities operations for fintechs, saving 70%+ of costs by making them programmable

ACV=€75k

Selling to banks and credit firms AND/OR startups raising €10m+ in asset backed debt

English

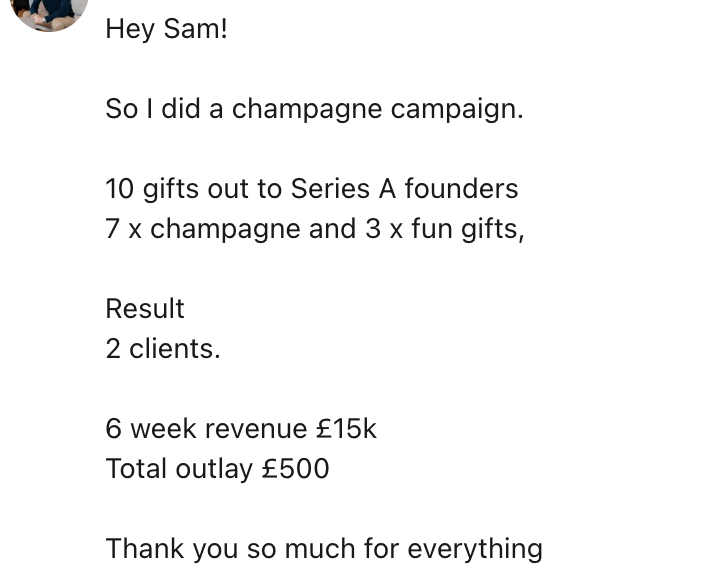

I get a message about once / day saying the outbound champagne campaign we ran at Brex, or a variation I suggest to the founder or sales leader, is the best performing demand gen campaign the company has ever tried. A couple examples attached.

Comment below with a 1 sentence description of your business, your buyer segment and persona, and your ACV, and I’ll reply with an idea for an outbound campaign for you. Example: corporate cards and expense management software, startup founders, $50k. I’ll respond to as many as I can while on this 8 hour flight.

English

@immad @mercury + fence.finance

+ startup raising $5-40m in asset-backed debt (bnpl, loans, hardware subscriptions, …) or credit funds

+ 80% lower than tradfi solution

+ SaaS platform to automate debt operations (reporting, covenant monitoring, draw down requests, cash waterfall, …)

English

@brianfakhoury good examples of it in the wild? we are building our homepage and would love to look into this

English

The future homepage of startups is (partially) a chat interface with a pre-filled conversation pitching the service/product and the ability for a visitor to continue the conversation based on what questions they have.

Already seen this a few times in the wild.

English