SOTD

14.8K posts

SOTD

@sotdsotd

Est Jan 2016 #sotd. Views imo imo imo. Statistician and bcfc fan.

Katılım Şubat 2016

1.4K Takip Edilen8.5K Takipçiler

@BCFC @UNDEFEATEDinc Thought we took Doyle off after 60 mins to rest him…

Plus should play 433 in this game

English

𝙏𝙀𝘼𝙈 𝙉𝙀𝙒𝙎 ⚪️

Five changes from Tuesday.

JB starts in goal. Starts for Leonard and Dykes too.

English

@moving_charlie Absolute nonsense.

Rent needs taken into account, which would drastically increase with inflation but your mortgage payments would stay the same.

Plus need to consider what are the other options to negate your money being eaten from inflation?

English

Buying a £300k home with a 50k deposit and a 30yr 5% mortgage for the balance means you need to sell it for £965,000 at the end, just to break even.

Your £300k home with a £250k 5% mortgage over 30 years will actually cost you £513,000 including interest, excluding maintenance.

So you won’t make any “profit” on it until its value exceeds £513,000, AND THEN you need to adjust for inflation.

30 years of inflation even at just 2% means it will need to sell at £965,000.

TO BREAK EVEN.

See why renting and investing might be a faster way to ownership?

To determine the future value of the home needed in 30 years to break even on all costs, including the mortgage interest and accounting for 2% annual inflation, we need to calculate the total cost of the mortgage (principal plus interest), adjust it for inflation, and ensure the home’s value covers this amount plus the initial deposit, also adjusted for inflation.

Step 1: Total Mortgage Costs

From the previous calculation, for a £250,000 mortgage with a 5% interest rate over 30 years:

•Total interest paid = £233,059

•Principal = £250,000

•Total mortgage cost = £250,000 + £233,059 = £483,059

Step 2: Adjust Total Mortgage Cost for Inflation

Inflation at 2% per year over 30 years increases the future value of money. We use the future value formula for inflation:

[ FV = PV \cdot (1 + i)^n ]

Where:

•( PV ) = present value = £483,059

•( i ) = annual inflation rate = 2% = 0.02

•( n ) = 30 years

Calculate:

[ (1 + 0.02)^{30} = 1.02^{30} \approx 1.811361 ]

[ FV = 483,059 \cdot 1.811361 \approx 875,054 ]

The inflation-adjusted total mortgage cost in 30 years is approximately £875,054.

Step 3: Adjust the Initial Deposit for Inflation

The initial deposit is £50,000. Adjust this for 2% inflation over 30 years:

[ FV = 50,000 \cdot 1.811361 \approx 90,568 ]

The inflation-adjusted value of the deposit is approximately £90,568.

Step 4: Total Future Value Needed to Break Even

To break even, the home’s future value must cover:

•The inflation-adjusted mortgage cost (£875,054)

•The inflation-adjusted deposit (£90,568)

[ \text{Total future value} = 875,054 + 90,568 = 965,622 ]

Step 5: Final Answer

The home’s future value in 30 years needs to be approximately £965,622 to break even on all costs, including the mortgage interest and accounting for 2% annual inflation.

English

SOTD retweetledi

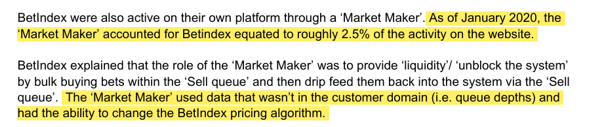

Day 1 of publicly revealing evidence regarding #footballindex that should have been discussed in private with @fionatwycross and @dcms - the market maker. An unregulated MM who was designed to provide liquidity but didn't. Insider trading would be a better description

English

@EalingHour Greetings #EalingHour! Well, I managed to not only find out about, but, but also make it to the In-N-Out Burger pop up in Park Royal today… I was so keen, I was first in the queue.

English

It’s 8pm on the first Tuesday of the month of February - and time for our #EalingHour community chat

For the next 60 minutes we’ll be talking about goings-on in the London borough of Ealing

Anything to share that’s Ealing related? Remember to include the #EalingHour hashtag

GIF

English

First pint after a game on a Sunday morning

The Screen Rot Podcast@screenrotpod

Your fella sampling the Carling at the local after doing Dry January

English

🍳 Rate my English Breakfast out of 10 boys?

£15.95 all in for this magnificent feast.

You've got to be impressed, haven't you?

English

@Cal_Lewis_7 @joshpearson180 Gt3 are £14 (top right) on Amazon now. I used them for a year or so, decent.

English

@joshpearson180 Link to that red dragon set? Kind find them anywhere

English

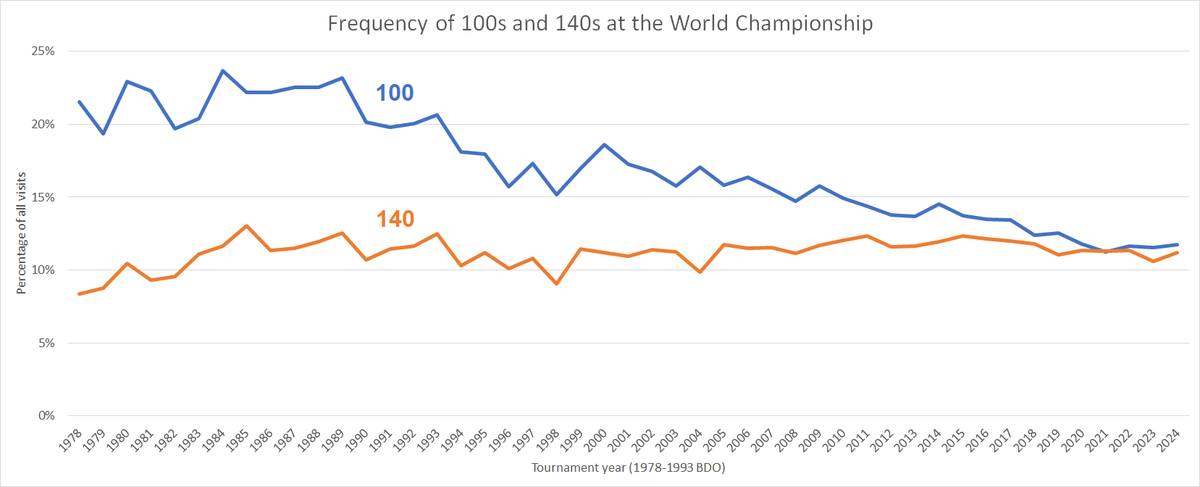

It's more of a long-term trend, beginning around 1990 (possibly sparked by Phil Taylor). The eclipsing of 100 has already happened in the Premier League and is happening now in the World Championship:

Dan Dawson@DanDartsDawson

@ochepedia That is quite the stat. Has the gap between 100 and 140 decreased significantly in recent years?

English

SOTD retweetledi

🚨 DARTS GIVEAWAY 🚨

🎯 We've got ONE pair of tickets to give away for the AFTERNOON session at the Paddy Power World Darts Championship on Monday 1⃣6⃣th December.

For a chance to win those tix, simply REPOST this post 👇

Only enter if you're sure you can attend. T&Cs below.

English

SOTD retweetledi

@chriswisey No “foreign” manager has ever won an international tournament.

Small sample size at top clubs and top nations.

English

No Englishman has won a domestic trophy in England since Harry Redknapp lifted the FA Cup with #Pompey in 2008.

Worth keeping that in mind if you’re questioning the reasons behind the FA choosing Thomas Tuchel.

English

SOTD retweetledi

The following thread relates the connection between Betindex #footballindex and Index Labs the 100% owner. This is in response to the Liquidators Report published yesterday. This is not from Begbies but BDO the Liquidators of Index Labs.

English

If this is done and Roberts gone, Stansfield must be done, right, right? #bcfc

Fabrizio Romano@FabrizioRomano

🚨⚪️⚫️ Reiss Nelson to Fulham, agreement done after Ipswich Town deal off! Documents being prepared to get it done in time.

English

@moving_charlie How can you include inflation as a negative to buying when one day you will you be comparing rent payments in 5 and 10 years time a mortgage payment similar to today.

English

Owning v Renting: "My mortgage would cost less than my rent."

Often the case. But to work out the true cost of buying with a mortgage you need to do the following sums:

Mortgage Repayment +

Mortgage Interest +

Maintenance Costs +

Inflation +

Stamp Duty.

Mortgage Repayment = Actual purchase price - deposit.

Mortgage Interest = Total amount paid to lender - amount borrowed.

Maintenance Costs = Everything your landlord has to pay for plus any improvements, decor or upgrades

Inflation = Even at 2% per annum, that's how much your home is devaluing by every year. So, over 25 years thats a 50% devaluation against your initial purchase price, in real terms.

Stamp Duty = Purchase Tax where applicable (doesn't affect most First Time buyers currently, but will hit more in April 2025 when the threshold lowers again).

All of this has to be deducted from any nominal increase in price before you have actually made any kind of financial return on your 'investment'.

Renting includes NONE of these costs and gives you flexibility and options, but currently has the risk of being asked to leave against your wishes.

Choose wisely - it's different for everyone!

GIF

English